Daily Morning Note – 7 February 2022

Welcome to our Daily Morning Note from our Research team!

PHILLIP SUMMARY

Singapore shares tracked most regional peers to log gains on Friday (Feb 4), brushing off Wall Street’s red ink overnight. The Straits Times Index (STI) rose 0.47 per cent or 15.42 points to 3,331.41 for the day, outperforming the 30-month record high it made on Thursday. The benchmark saw 2.62 per cent in gains for the week.

Wall Street stocks finished mostly higher Friday (Feb 4) as markets weighed a surprisingly good US jobs report that raised expectations for aggressive tightening in monetary policy. The US added an unexpectedly robust 467,000 jobs in January, according to Labor Department data that also significantly raised job figures for November and December. The Dow Jones Industrial Average finished down 0.1 per cent at 35,089.74. The broad-based S&P 500 gained 0.5 per cent to 4,500.53, while the tech-rich Nasdaq Composite Index jumped 1.6 per cent to 14,098.01. All 3 indices posted gains for the week.

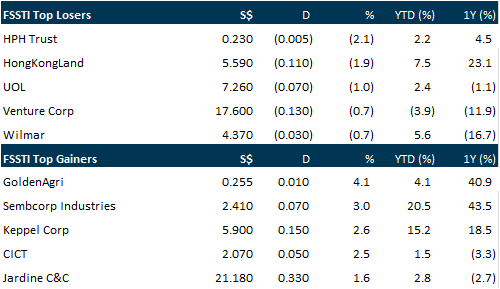

Top gainers & losers

BREAKING NEWS

SG

There were 4 primary-listed stocks conducting share buybacks over the 21/2 sessions through to Feb 3, with a total consideration of S$5.7 million. Aside from an abbreviated trading week, less share buyback activity is expected at this time of the year, as financial reporting gathers pace. Keppel Corporation led the consideration tally, buying back 977,600 shares over the 21/2 sessions at an average price of S$5.68 per share. On Jan 27, Keppel Corporation announced it had established a S$500 million share buyback programme, in accordance with the share purchase mandate granted by its shareholders at the company’s previous AGM. The group noted that shares repurchased will be held as treasury shares which will be used in part for the annual vesting of employee share plans, but also as possible currency for future merger and acquisition (M&A) activities.

After years of struggling to emerge from the shadows of regional rivals, Singapore Exchange is looking to establish itself as the hub for blank-cheque firms, riding on regulatory overhaul, support by state firms, and a tech boom in its back yard. Encouraged by the flurry of Southeast Asian tech start-ups seeking funding and the bourse’s revised rules, Singapore could list up to a dozen special-purpose acquisition companies (SPACs) within the next 12-18 months, bankers, venture capitalists, and analysts say. A key test for SGX will come when such companies, also known as blank-cheque or shell firms, have to seal merger targets within two years, a “de-SPACing” process already weighing on US deals as hundreds of SPACs chase targets.

The average return over 10 years for the March issue of the Singapore Savings Bonds (SSBs) has hit 1.79 per cent – its highest rate since 2019. SSBs last recorded an average return over 10 years of 1.95 per cent per annum for its September 2019 issue. The first-year interest rate for the March 2022 issue stands at 0.59 per cent, while the 10-year interest rate is 2.18 per cent. The edging up of interest rates comes amid expectations of an interest rate hike in March by the Federal Reserve, in a bid to tame rising inflation. The US central bank is projected to raise the target interest rate by a quarter of a percentage point from the current near zero level.

US

Sky-high valuations for Procter & Gamble (P&G) and other household-goods makers are deterring some investors from loading up on these classic defensive plays even as soaring inflation and the prospect of Federal Reserve rate hikes rattle stocks. The S&P 500 Household Products Index has outperformed the broader market amid stocks’ rocky start to 2022, and also for the past 6 months. It has climbed about 11 per cent in that period versus a roughly 3 per cent gain in the broader index, including dividends. The downside to that superior record, however, is that shares of household-products companies are trading around the priciest level since 2000 based on projected earnings, at valuations that are on a par with high-flying tech shares.

The director of the US Centers for Disease Control and Prevention (CDC) signed off on the US Food and Drug Administration’s full approval of Moderna’s Covid-19 vaccine in those aged 18 and over, the agency said on Friday (Feb 4). The vaccine has been in use under the US Food and Drug Administration’s emergency use authorisation since December 2020, and is now the second fully approved vaccine for Covid-19 in the US. Earlier on Friday, a CDC panel voted unanimously to recommend the vaccine’s use, after the FDA granted full approval of the shot on Monday.

Apple is targeting a date on or near Mar 8 to unveil a new low-cost iPhone and an updated iPad, according to people with knowledge of the matter, kicking off a potentially record-setting year for product launches. The announcement will mark Apple’s first major event since a new MacBook Pro debuted in October. Like the company’s other recent launches, it is expected to be an online presentation rather than in-person, said the people, who asked not to be identified because the deliberations are private. Apple is coming off a holiday quarter that far exceeded Wall Street predictions, helping quell fears that supply-chain problems would hurt sales. Now the company is setting its sights higher for 2022. The March announcements – along with the usual flood of product news expected later in 2022 – suggest Apple will introduce its biggest crop of new devices ever in a single year.

Source: SGX Masnet, The Business Times, Bloomberg, Channel NewsAsia, Reuters, CNBC, PSR

Lendlease Global Commercial REIT – Room for organic and inorganic growth

Recommendation: ACCUMULATE (Maintained), Last Done: S$0.85 Target Price: S$0.94, Analyst: Natalie Ong

• 1H22 DPU of 2.40 Scts (+2.6% YoY) was in line, forming 48.4% of our FY22 forecast. DPU was lifted by the acquisition of an additional 28.1% stake in JEM over Aug-Sep21.

• 313@Somerset occupancy at an all-time high of 99.7%, 17% of GRI de-risked with weighted average reversions in high single-digits.

• Gradual deployment of c.11k sq ft from higher plot ratio could lift NPI by 2-3%.

• Maintain ACCUMULATE, DDM target price lowered from S$0.97 to S$0.94. FY22e-26e DPUs have been lowered by 1.4-1.9% on the anticipated rising cost of borrowing. Our DDM-based TP dips from S$0.97 to S$0.94 on lower DPU estimates and higher cost of equity of 7.72% assumption (previous 7.66%). Impending acquisition of remaining stake in JEM and deployment of additional GFA at 313@Somerset are catalysts for LREIT.

Meta Platforms Inc – Competition knocks growth and raises expenses

Recommendation: BUY (Maintained); TP US$312.00, Last close: US$237.09; Analyst: Jonathan Woo

• 4Q21 earnings in line with expectations. FY21 revenue/PATMI at 102/105% of our FY21e forecasts

• Apple iOS 14 privacy changes decreases the accuracy of FB’s targeted ads, making it increasingly tougher to track and measure the outcomes of these ad campaigns

• The company guided weak 1Q22 revenue growth of 3-11% and FY22e expenses to rise at least 26% to US$90bn-95bn. FB is also undertaking major capital expenditure of US$29bn-34bn to beef up its IT infrastructure.

• We maintain a BUY recommendation with a reduced DCF target price from US$424.00 to US$312.00 (WACC 6.6%, g 3.5%). Our target price is lowered due to growth pressures from increased competition and reduced earnings of 24% due to increased expenditures.

POEMS Podcast: Let the Money Talk

Recent Podcasts:

Daily Morning Note – February 4, 2022

Microsoft Corporation 2Q22 Results – SGX Company Insights Ep 49

Apple Incorporation 1Q22 Results – SGX Company Insights Ep 48

Visit www.stocksbnb.com to learn more!

Join our Phillip Securities Research Telegram channel for the latest update on our stock coverage!

Click here to join: https://t.me/stocksbnb

Webinar Of The Week

Weekly Market Outlook: Del Monte, Keppel Corp, Keppel DC, Frasers, Microsoft Corp, Netflix, TDCX….

Date: 31 January 2022

Updates summarised in 3 minutes

Phillip Research in 3 minutes: #29Keppel Corporation; Initiation

For more videos on Phillip in 3 Mins

| Disclaimer |

| The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials. |

| Confidentiality Note |

| This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation. |