中国2019年投资策略:紧随政策,看好新能源汽车和房地产行业

事件:2018年中央经济工作会议在中国北京召开 2018年12月19日至21日,一年一度的中央经济工作会议在北京举行。该会议是中共中央,国务院召开的最高规格经济会议,其核心任务是总结2018年全年经济工作情况,分析当前经济形势,部署规划2019年的经济重心。

研究概要

• 稳需求将成为2019年政府工作主要目标,2019年GDP增长预计稳定在6.2%左右。

• 重点关注有政府政策支持的消费行业,如新能源汽车。

• 政府释放房地产宽松信号,2019年尤其是一线城市房地产市场或将迎来政策回暖。

2018年中央经济工作会议确定了2019年的经济工作的主要工作思路,会议指出2019 年中国经济面临下行压力。2019年中国政府将以更加积极的财政政策和货币政策来稳定总需求,保持经济运行在合理区间,进一步稳就业,稳金融,稳外贸,稳外资,稳投资,稳预期(6个稳字)。

在经济下行的背景下,我们观察到多数板块价格都处于低点。2019年我们更加关注政策对行业的推动与支持,同时关注行业以及上下游产业链的增长潜力。基于这两点我们在2019年重点关注新能源汽车行业和房地产行业。

稳需求增长将成为2019年政府工作主要目标,2019年GDP增长稳定在6.2%左右。

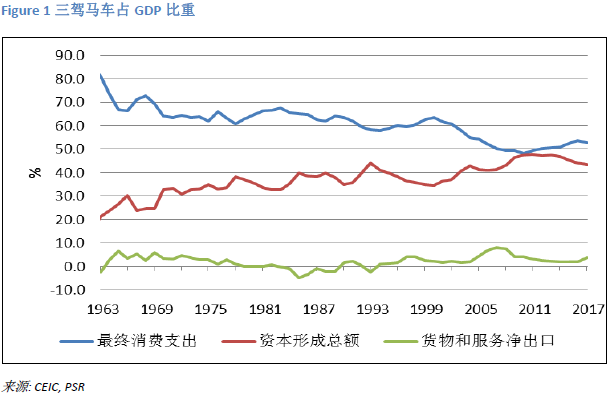

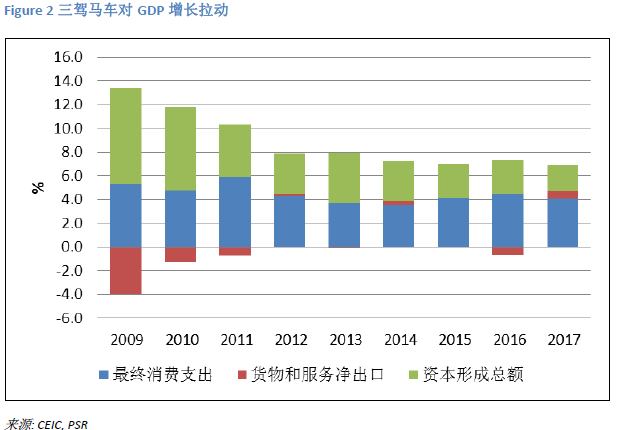

2019年政府经济工作将围绕六个稳字展开。结合六个稳的内容,我们认为政府重点在于稳定需求。从需求侧来看,结合图一以及图二三驾马车占GDP比重以及对GDP增长的拉动,我们认为2019年政府将大力促进消费,稳中有升鼓励资本投资,以对冲贸易战以及其他因素导致的不利影响。

2019年是新中国成立70周年,是全面建设小康社会的关键之年。根据十八大提出的要求,到2020年,人均国内生产总值力争比2010年翻一番,由此2019以及2020年中国GDP增长值速度将力争保持在6.2%左右。财政政策和货币政策的重心会是稳定经济增长。

需求端中消费对经济下行的对冲力度有限,重点关注有政府政策支持的消费行业,如新能源汽车。

从最终消费占GDP总量和对GDP增长拉动看,稳定消费增长显得尤为重要。在2019年我们期待政府将出台更积极地财政政策以刺激实体消费,具体将会从减税和降费两个角度展开。

此次中央经济工作会议中提到更好落实好个人所得税专项附加扣除政策,增强消费能力。具体来看,此次修改的个人所得税法将基本费用标准由每月3500元人民币提升至5000人民币,同时对子女教育,赡养老人等共6项个人支出作出专项附加扣除。此次减税力度虽大.

但是由于中国个税纳税人占比较低,且缴纳主力是中国一二线城市的就业人群,对于三四线城市的消费拉动影响不大,我们认为该项政策对拉动消费总量增长影响有限。

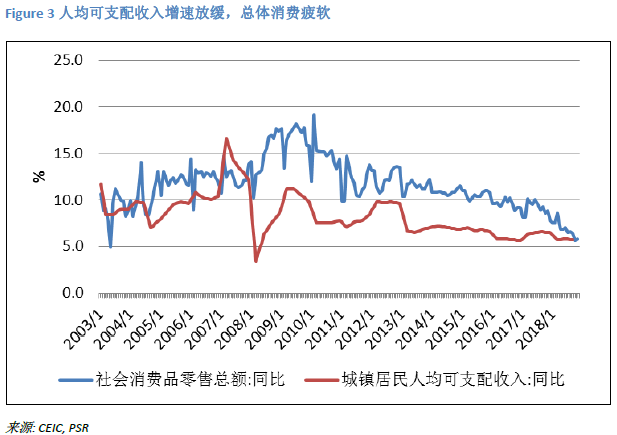

同时由图三人均可支配收入增速以及社会消费品零售总额的增速来看。2013年年城镇居民可支配收入增速逐年放缓,预计2019年居民消费对经济进一步拉动贡献有限。

但是从消费总量以及消费对经济拉动总量角度看,相比其他板块,消费板块仍然是经济增长的主力。因此2019年我们仍看好消费行业。尤其是有政府政策支持的相关消费行业,我们认为在政策支持下,个别板块行业将高速发展。

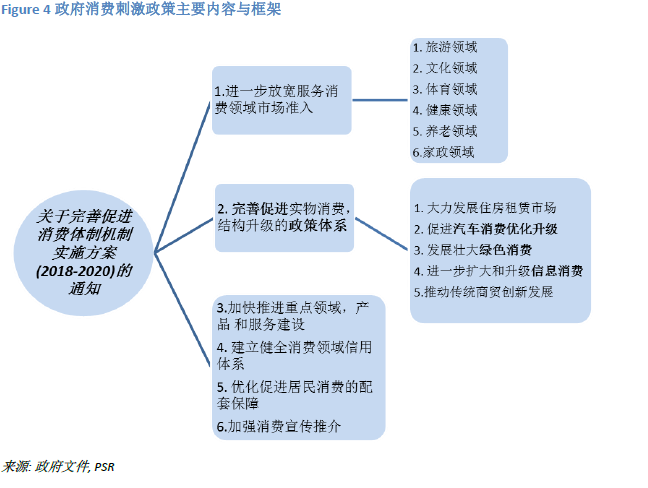

在消费刺激政策上,2018年9 月 20 日和 10 月 11 日分别落地的《关于完善促进消费体制机制进一步激发居民消费潜力的若干意见》和《完善促进消费体制机制实施方案(2018—2020年)》(下面简称《实施方案》)为未来三年消费刺激政策指明了大方向。

在行业选择上,我们重点关注有政府政策支持,且在政府三年消费促进方案中大力推进的相关消费行业。从《实施方案》中我们可以看到,在完善促进实物消费结构升级方案中中,未来三年,政府将大力促进房屋租赁,汽车消费消费升级以及信息消费。

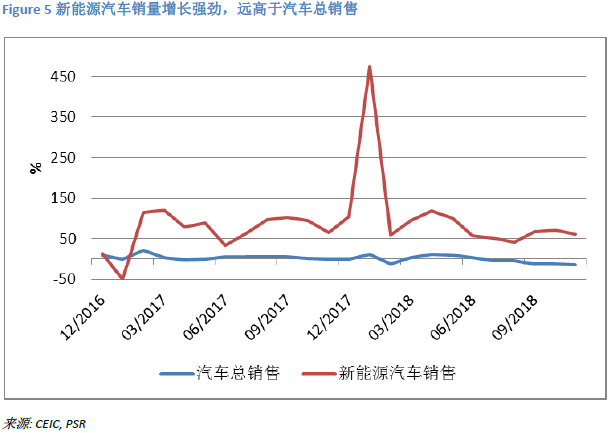

在新能源汽车,绿色环保,信息消费,电商等政府大力支持的行业中, 我们看好新能源汽车在2019年的发展。主要从总量和增长速度两个角度来看:

总量上,2018年中国新能源汽车销量占全球总销量超过40%。2019年我们认为中国电动汽车市场有望变得更大,因为中国政府对所有在中国运营的主要制造商提出生产新能源汽车的最低要求。如果没有达到要求的企业要受到暂停高油耗产品申报及生产的处罚。中国政府计划到2020年,新能源汽车的年产量要达到200万量,累计产销500万辆。根据2018年11月的数据,新能源汽车累计生产110万量,若要达到2020年的目标,平均每年将保持超过30%的年增长率。

增长速度上,自2017年以来,新能源汽车销量增长强劲,且保持在50%以上的年增长,远高于中国汽车总销量增长。

自2019年1月1日起,中国政府推出了新的双积分政策。在新标准下,公司生产高油耗汽车将产生负分,生产新能源汽车和节油汽车产量将增加正分。同时,新能源汽车的积分应占总分的10%,2020年该比例将提高到12%。

值得注意的是,没有足够的新能源汽车生产点的企业需要从其他企业购买相关积分,否则就不得不削减油耗汽车的产量。

补贴方面,我们注意到政府对优质新能源汽车补贴力度加大,如政府将可行驶400多公里以上的高耐力车补贴标准从4.4万元提高到5万元。

2019年,我们认为在财政政策补贴和双积分政策的推动下,企业将大力生产新能源车型,提高燃油车的节能水平,加速升级技术。因此新能源汽车将持续保持高速增长,规模进一步扩大。尤其是新能源汽车的上下游产业链较长,新能源汽车行业的崛起将为经济增长提供新活力。

因城施策,政府释放房地产宽松信号,下半年房地产尤其是一二线城市房地产市场或将迎来政策回暖。

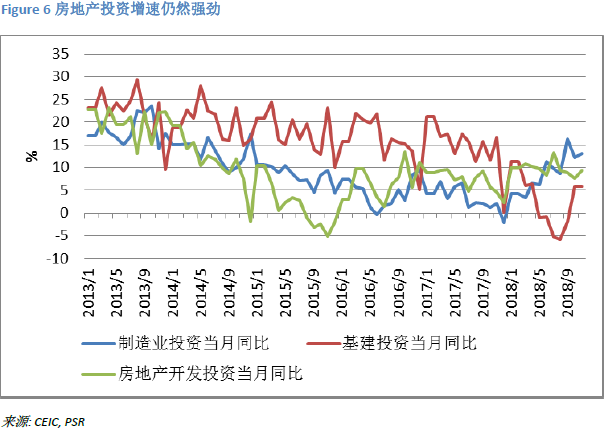

由图6固定资产投资各项来看,2018年制造业投资增速稳中有升,地产投资较为稳定且在市场波动情况下韧性较强,基建投资增速下滑较快。整体固定资产投资增速也从2017年的7.2%年增速回落到 2018 年 前三个季度的5.4%。

制造业方面,我们认为由于影响制造业投资的主要因素是企业的盈利状况。从近期的PMI数据以及企业盈利数据来看,两者皆低于预期。尤其是12月PMI落入荣枯线以下,制造业在2019年一二季度的压力加剧。

基建方面,尽管今年政府将大力支持基建行业。但是我们认为,相较房地产行业,基建行业的产业链较短,在经济下行压力加剧的背景下,缺乏增长韧性,对经济整体拉动效果有限。

房地产开发投资方面,我们认为政策对房地产影响较大。此次中央经济工作会议再度强调因城施策,与此前的“一刀切”性质的房地产政策不同,给地方政府在房地产政策上更多自主性与空间。加之房地产发展同样会拉动地产后周期产业的发展,带动消费,2109年我们看好房地产行业的发展,尤其是一线城市房地产行业。

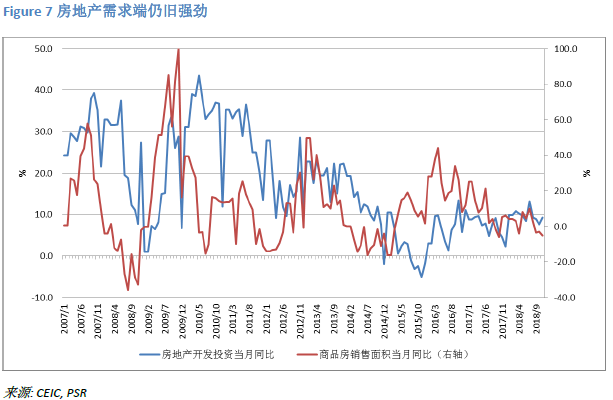

从供需看,自2015年年末房地产去库存以来,商品房投资增速明显减缓,而商品房销售增速保持稳定。2015年商品房销售增速同比增长6.5%,而房地产开发投资同比减少0.99%。2015年到2017年商品房销售增速远高于同期房地产投资开发增速。且房地产库存自2016年来逐年下降,目前商品房库存已经回落到2014年的水平。

随着城市化的推进,联合国预测,2010-2020年间有约2.05亿农村人口移居城市,2020-2030年将有约1.24亿人口移居城市。我们认为在2019年对于中国一二线城市房产的需求将持续增长。

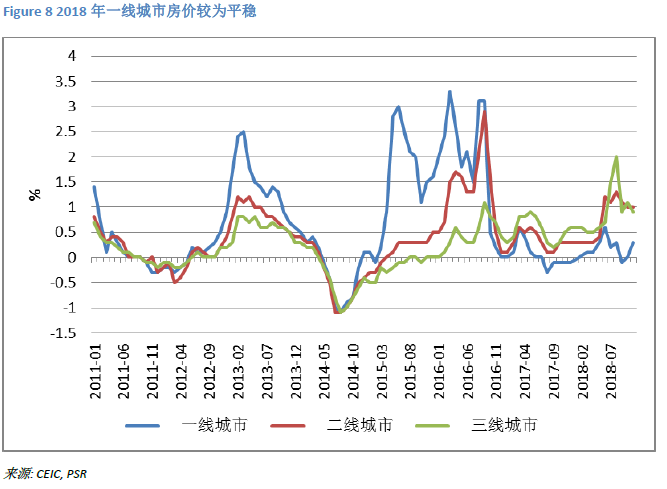

由图八房地产价格看,三线城市和部分二线城市在棚改货币化政策的刺激下价格有明显拉升。相比之下,2018年政府偏紧控一线城市房地产,一线城市维持严格的限售和限贷政策。一线城市整体住房贷款利率更高、放款时间更长。故2018年一线城市的房地产价格较为稳定。

我们认为,如 2019 年经济下行压力继续加大,单靠加大投资基建较难达到传到流动的效果,而减税对经济下行的对冲力度有限。地方政府将转向放松房地产政策,利用地产及地产后周期行业对经济增长进行支撑。

但房地产政策转向也会在坚持“房住不炒”的大逻辑下,重点保护刚需。由于2018年三四线城房价增长迅速,政策放松的可能性较低。相比之下,一线城市2018年房价较为平稳,放松一线和部分二线城市的调控措施,尤其是放松首套房的政策,以兼顾稳增长与保障刚需的可能性较大。

事实上自会议释放房地产放松信号以来,2018年12月共有17个城市首套利率均值出现回调,北上广深以及多数热门二线城市首套利率均值均有不同程度下降。而2018年11月,四个一线城市中仅有广州、深圳首套利率回调。

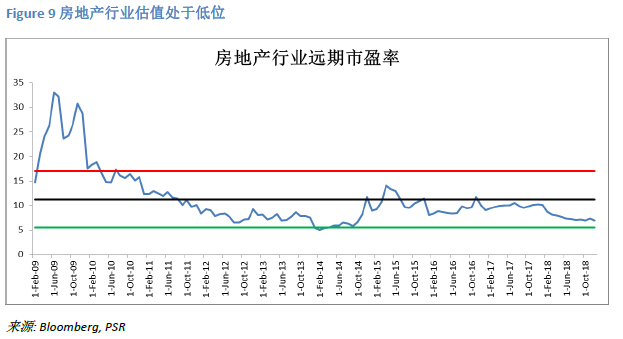

投资者应该密切关注2019年第一季度与第二季度的GDP增长数据,若一二季度经济增长不及预期,一二线城市政府可能出台更积极的房地产政策。且房地产行业远期市盈率处于低位。因此我们看好房地产尤其是一线城市房地产市场。

投资建议:

2019年,在经济下行的压力下,我们更关注政府政策对于优质行业的推动。我们认为在积极的财政政策推动下,该类行业将持续高速增长。

在消费行业中,我们看好有政府政策支持和补贴的新能源汽车行业。在固定资产投资方面,我们认为在政府放宽地产行业的大背景下,我们看好一线城市房地产行业的发展。

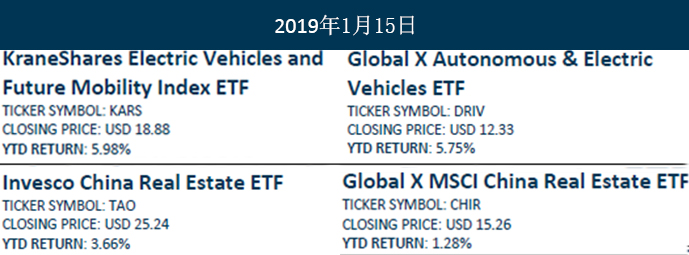

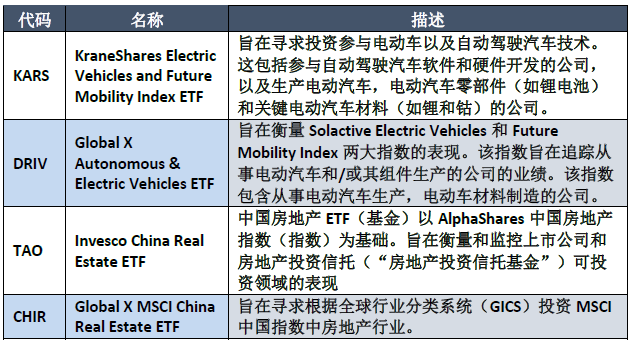

以下是我们推荐的该行业的交易所交易基金:

如果有想了解更多全球股市资讯,请关注微信公众共 “辉立资本新加坡” (SGPSPL)。同时提供在线免费开设股票账户,一个账户轻松交易美股,港股,新加坡股

关键字:新加坡股票研报,新加坡股,新加坡研报,新加坡账户,交易新加坡股票,新加坡股票开户,免费开户,在线开设新加坡股票开户,新加坡证券,新加坡券商,投资组合