研报 | 枫叶教育 (1317.HK) – 轻资产模式驱动,内地国际学校前景看好

投资概要

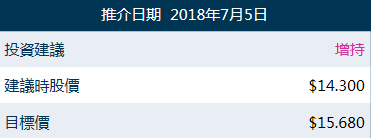

枫叶教育是一家在中国领先的学前教育到12年级教育(K-12)国际学校运营商。由于中国中产阶级的崛起,轻资产发展模式和独特的双文凭课程,我们相信枫叶将成为中国教育界最有前途的公司之一。 因此,我们给予枫叶“增持”评级,并得出目标价15.68港元,基于2019年纯利,并假设1倍PEG(2018-20年的盈利複合增长率为30%),潜在上涨空间为9.7%。(现价截至7月3日)

公司概况

枫叶教育是一家在中国领先学前教育到12年级教育(K-12)的国际学校运营商。公司成立于1995年,并在大连,武汉,天津,重庆,镇江,洛阳,上海,深圳等地开办了82所学校(其中5所是新收购,尚未併表)。近年,集团加快学校扩展, 2018年3月淨增17个,不包括5个新收购。 目前,集团拥有13所高中(10至12年级学生),21所中学(7至9年级学生),21所小学(1至6年级学生),19所幼儿园及3所外籍人员子女学校。

截至2018年3月,集团共有29,991名学生。在过去的三年半内,学生数目的複合增长率为26%。 由于集团希望打造一个小学到高中的金字塔型入学结构,小学学生的比例从2015年的26%上升到2017年的34%; 而高中学生从2015年的39%则下降到2017年的34%,表明集团决心扩大义务教育业务。

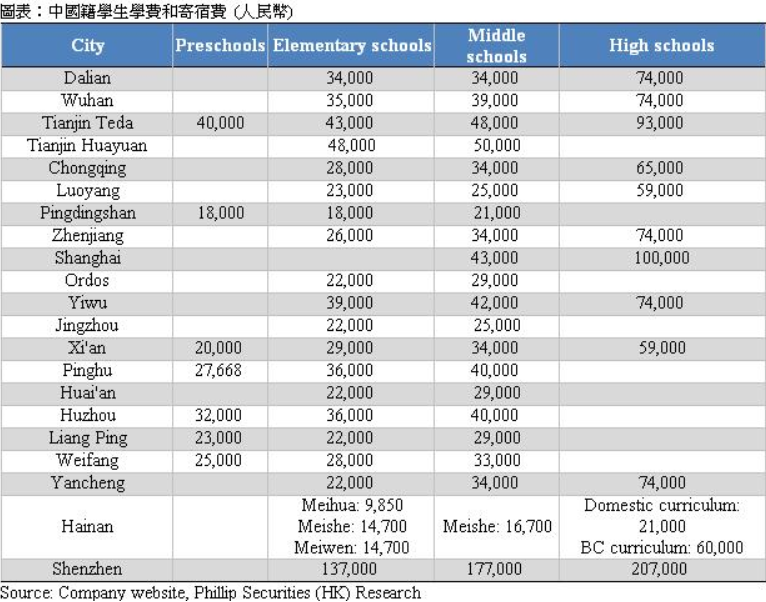

幼儿园/小学/中学/高中的平均学费和寄宿费分别为29,000 / 44,850 / 47,588 / 86,833元人民币。 2017年每名学生的平均学费则为38,642元人民币,同比下降2%,主要原因是收取较低学费的小学生比例增加。

行业概况 – 中国中产阶级崛起

经济改革后,中国成为仅次于美国的世界第二大经济体。 随着经济发展,中产阶级的数量也在不断增加。 根据波士顿谘询公司的数据,2021年中国可投资资产超过100万美元的家庭将达到4百万户,复合增长率为13.6%。 拥有超过500万美元可投资资产的家庭比例也预计从2015年的14%上升到2021年的16%。中产阶级的崛起将对国际学校产生巨大需求,因为父母能够负担得起学费。

留学生人数稳步上升

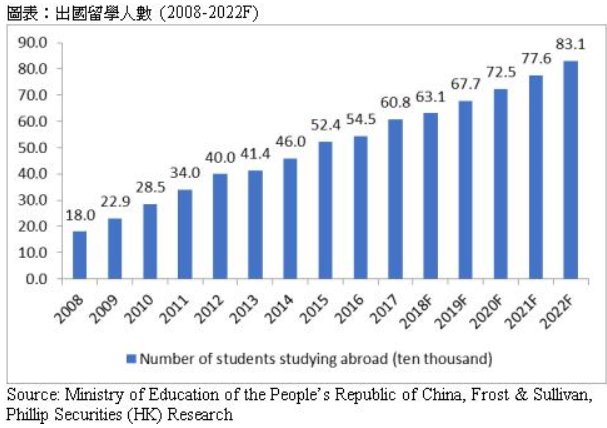

由于父母渴望为子女提供更好的教育,出国留学在中国越来越受欢迎。根据中华人民共和国教育部统计,出国留学人数从2008年的17.98万人增加到2017年的60.84万人,年复合增长率达14.5%。 Frost & Sullivan预测2022年该数字将会达到83.05万人,2018年至2022年的複合增长率为7.1%。大部分留学申请都是本科生和研究生,两者均佔36%。 这表明家长倾向让孩子在出国留学前完成K-12教育。这将有利于本土的K-12国际学校,因为这些学校都是主要帮助学生准备出国留学,如枫叶教育。

公立学校国际班的限制

2013年,中国政府实施了《高中阶段国际项目暂行管理办法》,以限制公立学校的国际课程供应。市政府停止批出新的国际班。2016年国际班数目下降1个至224;2016年国际私立学校数量则增加了136间至392。由于国际班是私立国际学校的替代品,国际班供应限制将减少该行业的竞争程度。

长期发展动力 – 轻资产发展模式

自2012年以来,集团开始以轻资产模式发展。轻资产发展模式代表集团与第三方合作,主要是地方政府[如果第三方是政府,便会是公私合作伙伴关係(PPP)],其中第三方提供土地或学校设施,而集团负责日常营运,包括﹕教师、教材或设施翻新。合作模式可以是租赁或利润分享。在租赁模式中,费用通常取决于学生人数或特定事件的触发因素。在利润分享模式中,利润通常与第三方分享一半利润。

轻资产发展模式的优势在于:1)投资回收期缩短,2)加速扩张。

首先,与第三方合作,集团可以节省大量在土地和学校设施的初期资本投资,这将使投资回收期能从两年以上(自有学校)缩短到一年左右。另外,这种模式亦可以充分利用集团丰富的运营经验。

其次,在初期资本支出减少和地方政府帮助下,集团可加快扩张并扩大经营规模。透过规模增大,集团可以通过在学校之间共享资源来提升运营效率,并提高校誉,从而向地方政府争取更多的PPP项目。

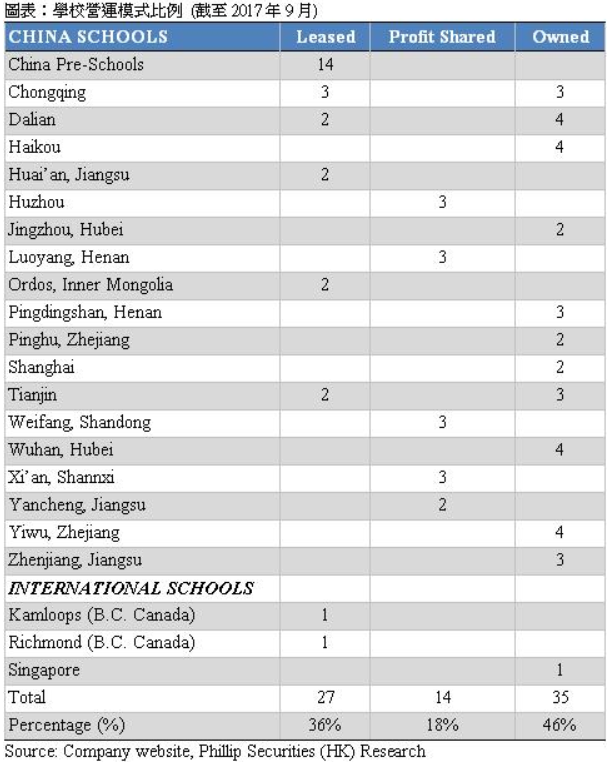

截至2017年9月,集团54%的学校分别属于租赁或利润分享模式。我们预计这战略将继续推行,使租赁和利润分享模式的学校比例在未来几年内继续上升。

长期发展动力 – 扩展至顶级一线城市

集团首先选择聚焦在一线,二线,三线和四线城市,然后才扩展至顶级一线城市。 刚开始,集团难以在顶级一线城市与北京国际学校、北京德威学校等知名学校竞争。然而,随着在中等城市积累更多运营经验和校誉, 它为集团进军顶级一线城市打下基础。 2013年,集团在第一个顶级一线城市 ─ 上海建立了第一所国际学校,并于2017年收购了深圳市伊思敦龙岗学校55%的股权,成为集团第二所位于顶级一线城市大城市的学校。我们预计集团将通过併购或自建学校,逐步扩大在顶级一线城市的网络。

长期发展动力 – 学费上涨加上额外收入来源

集团已确认将于2018年9月在大连,重庆,武汉,镇江,天津和洛阳提高学费25%。 管理层称其他学校也有可能在9月份提高学费,但需要进一步确认。 虽然新的学费只适用于新生,所以我们相信对收入和毛利率的影响将会在未来几年逐步体现出来。 儘管学费上涨了25%,但我们认为与其他国际学校相比,集团的学费仍然具有竞争力,因为集团的学费在过去远低于其竞争对手。

此外,集团亦通过提供海外学习谘询服务、游学团、教育假期活动和教育书籍租赁等其他服务来开拓更多的收入来源。其他服务收入佔总收入比例从2013年的14%上升至2017年的19%。通过为学生提供更多增值服务,学生不仅可以受惠,集团还可以获得额外收入。

双文凭课程 – 中国及不列颠哥伦比亚省(BC)高中文凭

集团的高中已获得加拿大不列颠哥伦比亚省教育部和中国政府的认证。毕业生将获得中华人民共和国和加拿大不列颠哥伦比亚省高中毕业证书,这为毕业生在选择上提供更大灵活性。

学校需要六个步骤才可得到BC离岸认证;1)兴趣表达,2)面试,3)申请,4)申请审查,5)前期认证,6)认证。首先,申请人需要联繫工作人员表达其兴趣,然后教育部将审查提交的内容。其次,教育部的代表将进行面对面访谈,以评估申请人的动机、经营离岸学校的能力及学校的目标和计划。第三,申请人需要提交文件,包括:离岸学校的商业计划、已审计财务报表、开支预算及地方政府批准。第四,教育部将任命考察团对其学校进行现场检查。第五,如果申请人通过检查,他们将与教育部签署为期一年的前期认证协议。教育部将根据考察团的建议以及学校是否符合前期认证协议中规定的要求,决定是否对学校进行认证。最后,通过前期认证后,申请人将与教育部签署一年的认证协议。另外,为认证续期,申请人需要通过年度实地检查。

我们相信严格的BC认证过程,将为潜在申请人製造进入壁垒,以保护现有离岸学校运营商的优势 ─ 枫叶教育。

据BCMOE称,中国38所离岸学校中有13所属于枫叶教育,佔学校总数的三分之一。

毕业生可以凭藉BC高中毕业证书进入顶级大学,特别是加拿大的大学。 由于BC高中文凭是加拿大认证的文凭。相比其他文凭的毕业生,如IB,AP或A-level,BC文凭的毕业生会更容易被加拿大的大学取录。根据JJL海外教育的研究,加拿大在中国留学生最喜欢的国家中排名第四,佔9.51%,仅落后于美国,英国和澳洲。我们相信集团的BC认证离岸学校对希望在加拿大留学的学生有一定吸引力。

毕业生优秀的入学记录

根据枫叶全球百强大学指南(美国《新闻周刊》全国类大学排名前30位、美国《新闻周刊》精英文理学院排名前10位、英国《泰晤士报》高等教育专刊英国大学综合排名前20位、加拿大《麦考林》杂志教育专刊大学医博类排名前10位、加拿大《麦考林》杂志教育专刊综合类排名前10位、QS世界大学综合排名最高的10所澳洲大学和QS排名最高的10所新加坡、中国香港、爱尔兰和新西兰大学),截至2017年8月31日止,1,807名毕业生中有56%获得了枫叶全球100强大学的录取,其中46人更得到了全球十大学校的录取通知书,包括﹕伦敦帝国学院及伦敦大学学院。毕业生优秀入学记录成绩反映了良好的教育质素,并为集团强大的竞争优势。

盈利预测

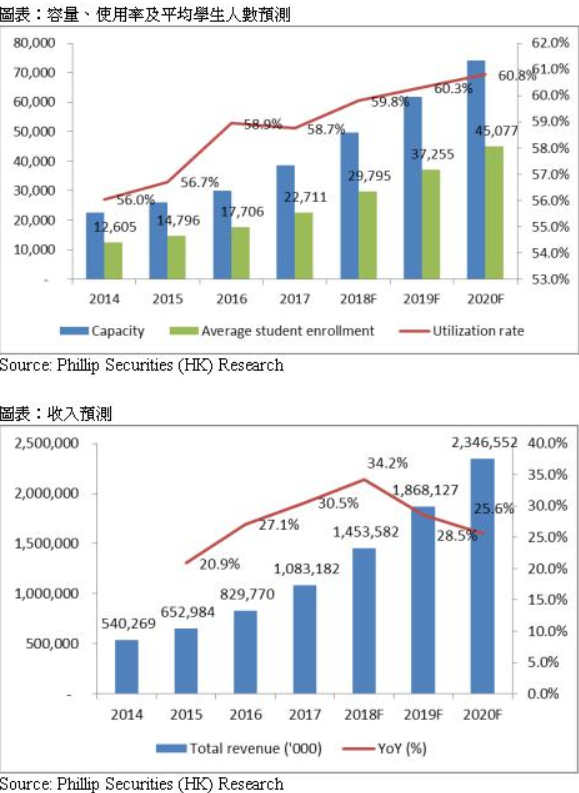

我们预计未来三年的容量增长将会保持强劲,但会逐步下降,并主要通过实现PPP、併购或自建,分别为28.9%/24%/20%。 同时,预计使用率将从2017年的58.7上升至2020年的60.8%。 由于容量增长强劲,我们在此并没有很进取的假设。 平均学生人数将从2017年的22,711人增加到2020年的45,077人。 此外,由于集团将继续为学生提供更多额外服务,我们预计其他服务的收入比例将从2017年的19%上升至2020F的22%。 为了反映从2018年9月起学费上涨,我们预计2018F-20F学生的平均学费将会上升1%/ 1.5%/ 2.5%。因此,我们预计2018F-20F的收入增长率分别为34.2%/ 28.5%/ 25.6%。

随着学费上涨,我们预计毛利率将从2017年的49.8%上升至2020F的52%。

我们预计2018F-20F的增长率将达到24%/31.1%/28.7%,这要归功于毛利率和学生入学人数的增加。

估值

由于中国中产阶级的崛起,轻资产发展模式和独特的双文凭课程,我们相信枫叶将成为中国教育界最有前途的公司之一。 因此,我们给予枫叶“增持”评级,并得出目标价15.68港元,基于2019年纯利,并假设1倍PEG(2018-20年的盈利複合增长率为30%),潜在上涨空间为9.7%。(CNY/HKD = 1.17)

风险提示

VIE 结构在中国被禁止

新收购学校未能为集团带来价值

关键字:新加坡股票研报,新加坡股,新加坡研报,嘉德置地商业信托 ,新加坡账户,交易新加坡股票,新加坡股票开户,免费开户,在线开设新加坡股票开户,新加坡证券,新加坡券商,投资组合,新能源汽车,补贴新政