ComfortDelGro - Stock Analyst Research

| Target Price* | 1.63 |

| Recommendation | BUY› BUY |

| Market Cap* | - |

| Publication Date | 4 Mar 2024 |

*At the time of publication

ComfortDelGro Corp Ltd - More growth ahead

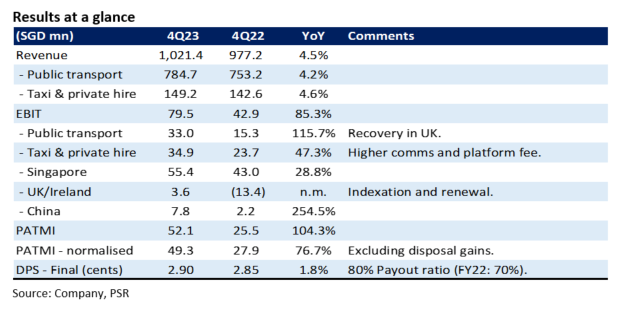

- FY23 earnings beat expectations at 117% of our forecast. Revenue was within our estimates at 98%. 4Q23 PATMI jumped 77% YoY to S$49.3mn.

- The turnaround in UK bus operations and growth in Singapore and China taxi operations were the major drivers of earnings.

- We raised our FY24e earnings by 24% to S$207mn. Our BUY recommendation is maintained and the DCF target price raised to S$1.63 (prev. S$1.57). We expect multiple earnings drivers in 2024; (i) higher platform fees and commission for Singapore taxis; (ii) UK bus indexation and re-contracting; (iii) Increased taxi fleet size in China; (iv) Margin recovery for Singapore rail operations as operating cost stabilises, rail passenger numbers grow and lagged re-pricing of fares.

The Positive

+ Jump in China taxi earnings. Operating profit in China jumped almost 4-fold to S$7.8mn in 4Q23. Earnings recovered as rebates were removed. Demand for vehicles has been strong, and ComfortDelGro is looking to expand its fleet to accommodate the demand.

The Negative

– Meagre rail earnings. We expect Singapore rail operations to be barely profitable. The rise in wages and electricity has impacted margins. We believe margin recovery will occur in FY24e from the lagged 7% rise in fares and slower rise in operating costs, especially electricity.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Trade of the Day - iFAST Corporation Ltd (SGX: AIY)

Trade of the Day - iFAST Corporation Ltd (SGX: AIY) Trade of the Day - Singapore Airlines (SGX: C6L)

Trade of the Day - Singapore Airlines (SGX: C6L) Trade of the Day - COSCO Shipping International (Singapore) Co Ltd (SGX: F83)

Trade of the Day - COSCO Shipping International (Singapore) Co Ltd (SGX: F83) Trade of the Day - Microsoft Corp (NASDAQ: MSFT)

Trade of the Day - Microsoft Corp (NASDAQ: MSFT)