CapitaLand Investment Limited - Stock Analyst Research

| Target Price* | 3.38 |

| Recommendation | BUY› BUY |

| Market Cap* | - |

| Publication Date | 4 Mar 2024 |

*At the time of publication

CapitaLand Investment Limited - Targeting to double FUM in 5 years

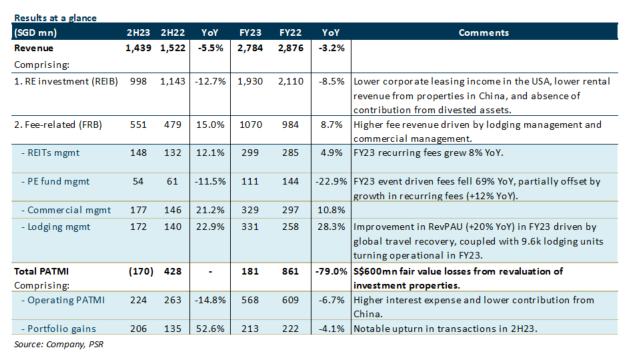

- FY23 revenue of S$2.784bn (-3.2% YoY) formed 92% of our FY23e forecast while PATMI of S$181mn (-79% YoY) was below our estimate due to revaluation losses of S$600mn and lower contribution from China.

- FY23 fee-related revenue (FRB) rose 8.7% YoY, driven by higher recurring fund management fees (+9% YoY), lodging management fees (+28% YoY), and commercial management fees (+11% YoY). However, this was offset by a significant decrease of 52% in event-driven fees. Including S$10bn of funds pending deployment, CLI has reached its FY24 FUM target of S$100bn and has now set a new target to reach S$200bn in five years.

- Maintain BUY with a lower SOTP TP of S$3.38 from S$3.68. We cut our FY24e PATMI by 15% after factoring in a weaker contribution from China. Our SOTP-derived TP of S$3.38 represents an upside of 29.2% and a forward P/E of 15x. We like CLI for its robust recurring fee income stream and asset-light model. We expect the FRB to continue to improve, boosted by the lodging business with higher RevPAU (FY23: +20%) and more lodging units turning operational.

The Positives

+ FY23 FRB revenue grew 8.7% YoY, boosted by lodging management fees (+28.3%), recurring fund management fees (+9.3%), and commercial management fees (+10.8%). This is partially offset by lower event-driven fees (-52% YoY) in a market that is less conducive to deal-making. Including S$10bn in committed equity pending deployment, CLI currently has S$100bn in FUM and is targeting to reach S$200bn in five years.

The Negative

– FY23 REIB revenue fell 8.5% YoY due to lower corporate leasing income in the USA and lower rental revenue from properties in China. Rental reversions in China remain negative across all operating segments.

– Significant fair value losses of S$600mn, which came mainly from China (-S$511mn) due to weaker rents and market outlook, as well as USA (-S$231mn) due to cap rate expansion. This is partially offset by gains in Singapore (+165mn) and India (+S$44mn).

About the author

Darren Chan

Research Analyst

PSR

Darren has over three years of experience on the buy-side as a fund manager. During his time as fund manager, he has managed multiple funds and mandates including dividend income, growth, customised, Singapore focused and regionally focused funds. He graduated from the University of London with a First-Class Honours degree in Banking and Finance.

About the author

Darren Chan

Research Analyst

PSR

Darren has over three years of experience on the buy-side as a fund manager. During his time as fund manager, he has managed multiple funds and mandates including dividend income, growth, customised, Singapore focused and regionally focused funds. He graduated from the University of London with a First-Class Honours degree in Banking and Finance.

Apr 19th - Things to Know Before the Opening Bell

Apr 19th - Things to Know Before the Opening Bell Trade of the Day - iFAST Corporation Ltd (SGX: AIY)

Trade of the Day - iFAST Corporation Ltd (SGX: AIY) Trade of the Day - Singapore Airlines (SGX: C6L)

Trade of the Day - Singapore Airlines (SGX: C6L) Trade of the Day - COSCO Shipping International (Singapore) Co Ltd (SGX: F83)

Trade of the Day - COSCO Shipping International (Singapore) Co Ltd (SGX: F83)