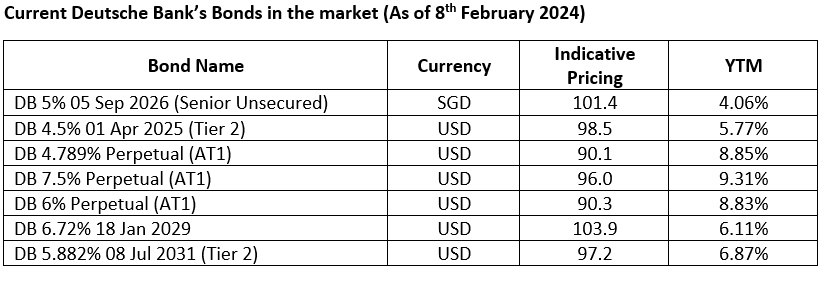

ID: @349vshmi

ID: @349vshmi

Company Overview

Deutsche Bank is a German multinational investment bank and financial services company headquartered in Frankfurt, Germany. It is dual-listed on both the Frankfurt Stock Exchange (FRA ticker: DBK) and the New York Stock Exchange (NYSE ticker: DB). It is also a constituent of the DAX stock market index which is a stock market index that consists of the 40 major German blue chip companies trading on the Frankfurt Stock Exchange. The bank has a global network spanning across Europe, Asia and America. There are four main divisions within Deutsche Bank, which are Corporate Bank, Investment Bank, Private Bank and DWS (which is its asset management arm). The main revenue driver for Deutsche Bank would be its private bank division which constituted (33.3%) of its total net revenue in FY2023, followed by its investment bank division (31.9%), corporate bank division (26.7%) and Asset Management (8.3%). As of 6 February 2024, Deutsche Bank has a market cap of USD26.88bn.

Deutsche Bank’s FY2023 Financials (ending 31st December 2023)

- Stable revenue uptick: In FY2023, Deutsche Bank’s total net revenue grew by 6% Y.o.Y (from €27.2 billion in FY2022 to €28.8billion in FY2023) mainly due to an improvement from its corporate and private bank sectors as product innovation in Corporate Bank has accelerated deals being won with largest multinational clients with substantial net inflows in AuM of € 57bn across Private Bank and Asset Management with combined AuM of € 1,455bn.

- Higher cost weighed on margins: Despite an increase in total revenue, higher noninterest expenses and income tax expenses have offset its revenue gains resulting in a decline of 13.6% Y.o.Y in net profit (from €5.7 billion in FY2022 to €4.9billion in FY2023)

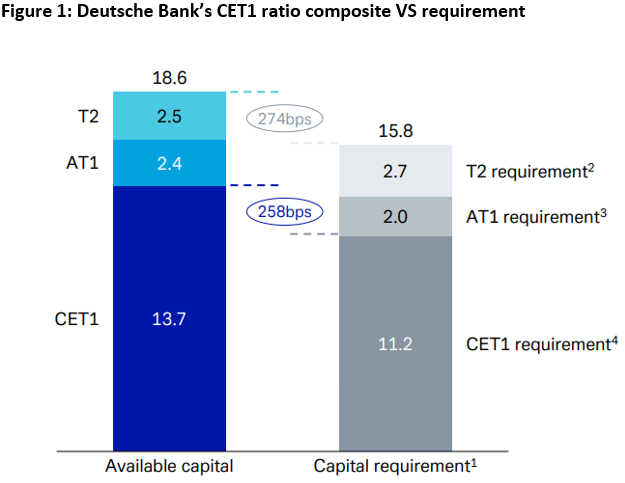

- Healthy capital structure: In terms of its capital management, Deutsche Bank’s liquidity coverage ratio has fallen slightly to 140% (142% in FY2022) but still maintains above its targeted range of 130% with a surplus of €62 billion above requirement. Deutsche’s Net Stable Funding Ratio (NSFR) which is a ratio that ensures the bank has enough stable funding to cover its long-term assets has maintained at 121% similar to FY2022. This was also above its targeted range of 115-120% with a surplus of €107 billion above the requirement. Last but not least, its CET 1 ratio (Figure 1) has also seen an improvement of 40bps (from 13.3% in FY2022 to 13.7% in FY2023) translating to a 258bps buffer as compared to the regulatory capital requirement and this was attributable to a strong organic capital generation and reduction in its risk-weighted asset (RWA) due to securitization transactions.

Source: Deutsche Bank

- Higher provision for credit losses: Elevated provisions were observed in FY2023 results. Provision for credit losses has been bumped up from 25.1bps in FY2022 to 31.1bps in FY2023. This was predominately driven by the higher Stage 3 provisions that were being set aside from their investment and private bank sectors and mainly for their Commercial Real Estate (CRE) loans.

- Cost management agenda in 2024 – 2025: Deutsche will be looking to manage its cost measures through the expected savings of € 1.3bn from the progression of Germany’s optimization, technology, and infrastructure efficiency. While also a reduction of ~3,500 roles mainly in non-client-facing areas. Bringing its current cost-to-income ratio of 75.1% down to approx. 62.5%.

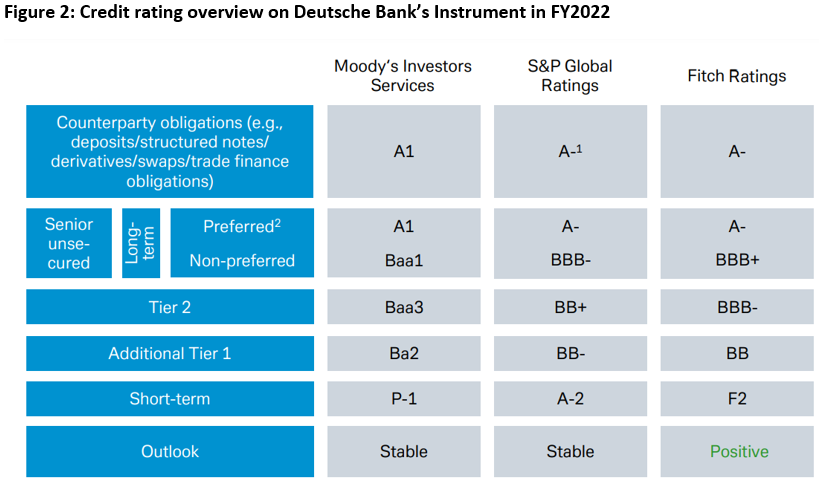

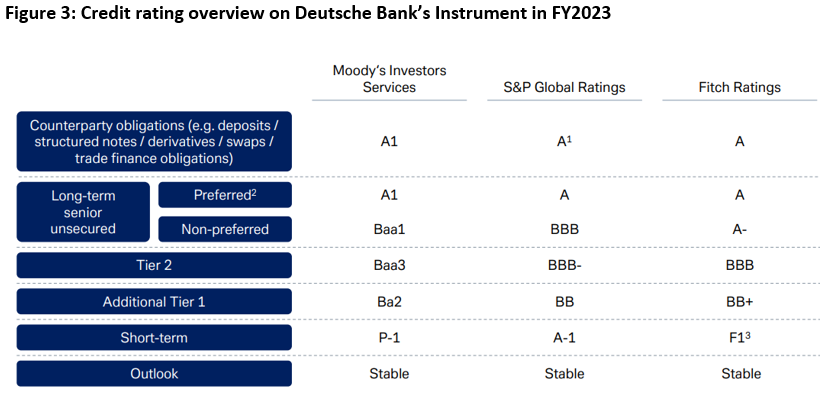

- In terms of its credit ratings, although in FY2023 after the default of Credit Suisse’s AT1 bonds, many investors tend to shy away from banking instruments for a little while. During this time, Deutsche Bank has also stepped up its credit rating by achieving a rating upgrade from major rating agencies which will support further spread contraction while also injecting more confidence for their fixed income investors (Figure 2 & 3)

Source: Deutsche Bank

Source: Deutsche Bank