ID: @349vshmi

ID: @349vshmi

Event

The U.S. Federal Open Market Committee (FOMC) concluded its two-day meeting on the 31st of January 2024. The meeting discussed the Fed’s monetary policy stance and economic projection.

Key points to note from this meeting

- Holding rates steady, awaiting greater confidence – In this FOMC meeting, the U.S. Federal Reserve (Fed) has decided to maintain its rates at a 22-year-high of 5.25-5.50%. This decision was made with the acknowledgment that the policy rate is likely at its peak for this tightening cycle and inflationary pressure within the US economy has been easing while the employment figures in the market remain resilient. This marks the fourth consecutive meeting where the rate has been held steady and this decision was in line with market expectations.

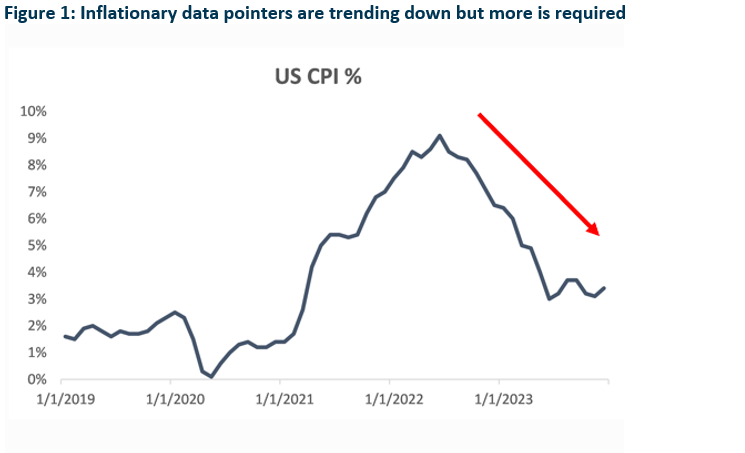

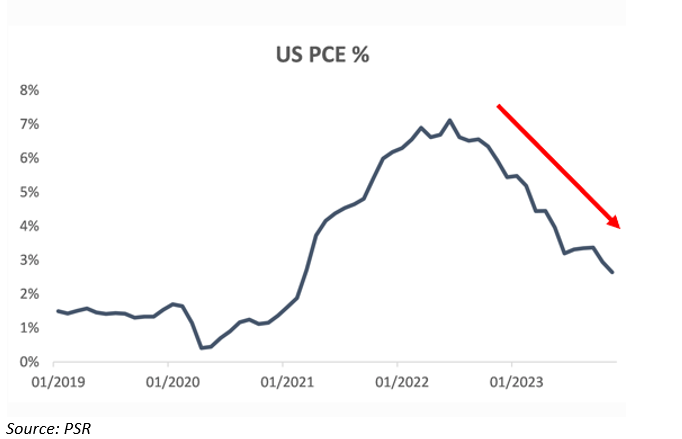

- Progression toward lower inflationary data – In the latest data releases, including indicators such as the Consumer Price Index (CPI) and Personal Consumption Expenditure (PCE), there are consistent indications of progress toward the 2% range. The most recent figures for December show the headline CPI and Core CPI at 3.4% YoY and 3.9% YoY, respectively. Headline CPI was slightly higher than November’s at 3.1% due to higher shelter costs. December’s Total PCE and Core PCE also reflected lower numbers at 2.6% YoY and 2.9% YoY, respectively, compared with November’s figures of 2.6% and 3.2%. Despite rates heading in the right direction, inflation remains relatively sticky.

- Federal Reserve Projection/Guidance – In December’s meeting, the market was pricing for rates to fall by approx. 150bps for this year with rate cuts coming as early as March. However, this optimism was dampened with Chairman Powell saying that he did not expect that it would be appropriate to reduce the target range until more certainty surfaced providing the Fed with the confidence required. It is unlikely that this confidence level will be achieved in the upcoming March meeting. According to the Summary of Economics Projection that was released back in December last year, we should still expect rates to fall to 4.6% in 2024 (75bps cut) but more progressive data in upcoming months will be required since these would play a major role in the decision-making process.

- Lukewarm Sentiments in the Market – With Chairman Powell throwing cold water on the hopes for rate cuts to happen as early as March this year, investors were pessimistic and have toned down the probability of a 25bps rate cut happening in March to 35% as compared to 75% before the meeting. All three major indices slid with the Dow Jones Industrial Average down 0.8% to 38,150.30, S&P500 down 1.6% to 4,845.65, and NASDAQ down 2.2% to 15,164.01.

- Movement on US Treasury Yields – For investors who are looking to park their excess cash for a relatively short period, short-term US treasuries are still priced at a relatively attractive rate with 6-month treasury yields hovering at the 5.18 range and 1-year bills at 4.73 range. At Phillip, we do offer US treasury bills and they are tradable on our POEMS platform. For more information please visit https://www.poems.com.sg/bonds/.