Company Overview

Adobe Inc is a leading software company providing creative, marketing, and document management solutions to professionals and consumers worldwide. The company operates through its flagship Creative Cloud platform, offering tools like Photoshop, Premiere, and Lightroom, alongside productivity solutions such as Acrobat for PDF management.

Strong Performance Driven by Creative Cloud Pro

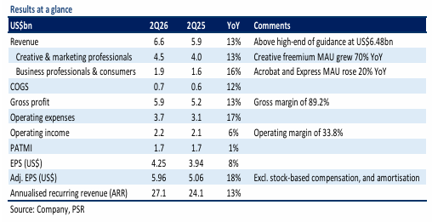

Adobe’s second quarter 2026 results met expectations, with revenue and adjusted profit after tax and minority interest reaching 50% and 51% of full-year forecasts respectively. The company’s performance was primarily driven by the Adobe Creative Cloud Pro offering, which has gained significant traction amongst creative professionals.

The freemium strategy continues to show remarkable results, with Creative freemium monthly active users surging 70% year-on-year to exceed 90 million users. This represents an acceleration from the 50% growth recorded in the first quarter. The user base expansion spans across web and mobile platforms, encompassing Firefly, Express, Premiere, Photoshop, and Lightroom applications.

Document Workflow Expansion Shows Promise

Adobe’s productivity suite demonstrated robust growth, with business professionals and consumers increasing 16% year-on-year. Acrobat and Express experienced particularly strong adoption, with monthly active users rising 20% annually. The integration of artificial intelligence capabilities has significantly enhanced performance, with annual recurring revenue in this segment tripling compared to the previous year.

ARR Growth Challenges Persist

Despite strong user engagement, Adobe faces ongoing challenges with annual recurring revenue growth. Excluding the US$480 million contribution from Semrush, Adobe’s ARR reached US$26.6 billion, representing 10.5% year-on-year growth. This marks the tenth consecutive quarter of organic ARR deceleration, reflecting management’s continued emphasis on user acquisition over immediate monetisation.

Investment Outlook

Phillip Securities Research maintains a BUY recommendation on Adobe with an increased target price of US$385, up from the previous US$368. The company trades at an attractive valuation of 11.5 times FY26 estimated GAAP price-to-earnings ratio, below its one-year average of 18 times. Despite competitive pressures from generative AI, Adobe’s commercially safe intellectual property, enterprise demand for comprehensive tools, and Firefly’s integration capabilities support a resilient outlook.

Frequently Asked Questions

Q: What drove Adobe's strong second quarter performance?

A: Growth was primarily driven by the Adobe Creative Cloud Pro offering, with Creative freemium monthly active users growing 70% year-over-year to over 90 million users.

Q: What is Adobe's current freemium strategy?

A: Adobe follows a "traction first, monetisation later" approach, focusing on acquiring freemium users through Acrobat and Firefly before converting them to paying customers.

Q: How is Adobe's document workflow business performing?

A: Business professionals and consumers grew 16% year-on-year, with Acrobat and Express seeing 20% growth in monthly active users and ARR tripling compared to the previous year.

Q: What challenges is Adobe facing with revenue growth?

A: Adobe's ARR has decelerated for ten consecutive quarters, with organic ARR growth at 10.5% year-on-year, as management prioritises user base expansion over immediate monetisation.

Q: What is Phillip Securities Research's recommendation and target price?

A: Phillip Securities Research maintains a BUY recommendation with a raised target price of US$385, up from the previous US$368.

Q: How does Adobe's current valuation compare to historical levels?

A: Adobe trades at 11.5 times FY26 estimated GAAP P/E, below its one-year average of 18 times, representing a significant discount to its recent historical valuation.

Q: What factors support Adobe's resilience despite AI competition?

A: Adobe's resilience is supported by commercially safe intellectual property, enterprise demand for end-to-end tools, and Firefly's large language model integrations.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.