- The stock falls below the strike price of the call and the call option expire worthless.

- The stock trade above the strike price and either

- exercise the option and buy the stock at the strike price and profit from the higher current market

- close out the long call position in a profit.

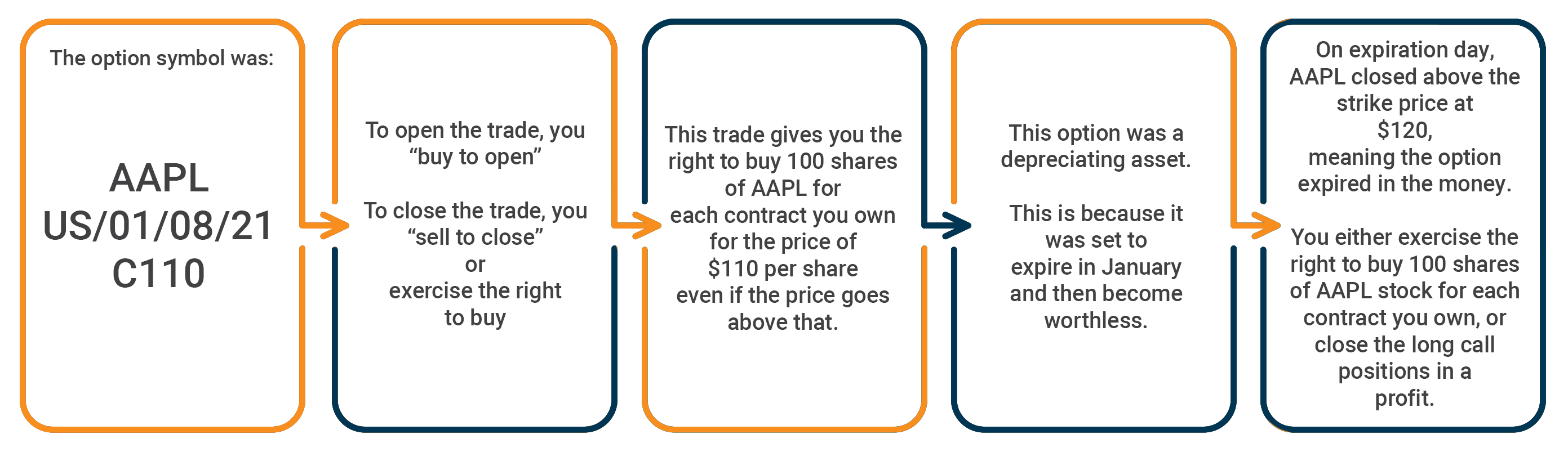

Long Call Trade Example

The trade was the Apple (AAPL) January 8th $110 Long Call (AAPL US 01/08/21 C110). You paid $139 ($1.39 x 100 shares) when you long the call and, at expiration, the option was in the money. The seller is obligated to sell the stock to us on Jan. 8, 2021, or you may close the long call position in a profit. Below are the details of the trade broken down step-by-step.

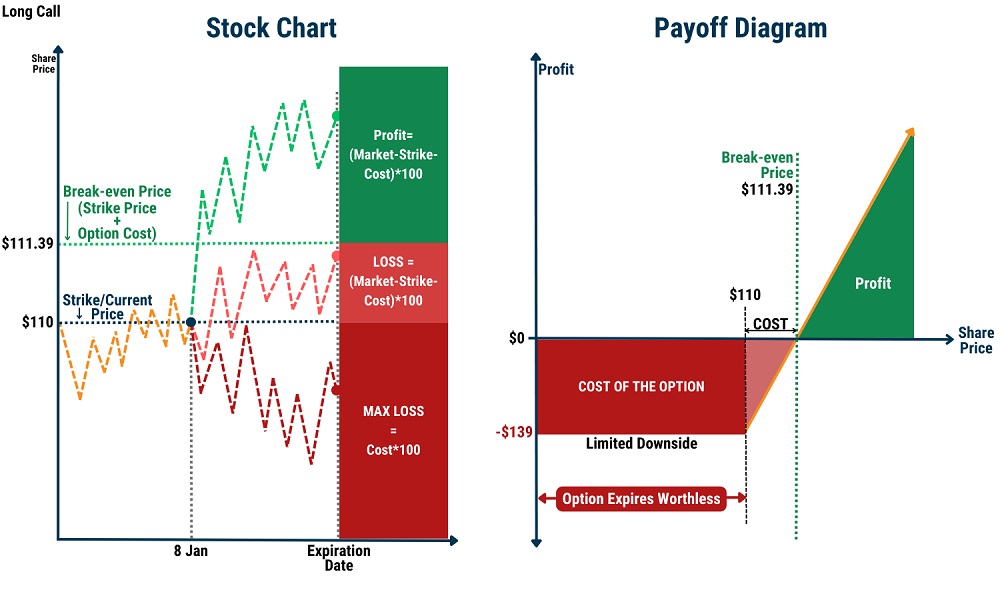

Long Call Stock Chart and Payoff Diagram

The Calls below can be employed with a Long Call Strategy:

The Calls below can be employed with a Long Call Strategy:- Deep OTM Call

- The option will be cheap as it is deeply OTM. The investor may employ this low cost strategy to profit when the option moves ITM.

- The risk that the option will expire worthless is great but therein lies the potential for a large return.

- Deep ITM Call

- This is an alternative to buying the shares outright while profiting from the same underlying stock price movement.

- A Call that is deep ITM has delta value that is close to 1, which means it will mimic the price movement of the underlying closely i.e. if the price of the underlying moves by $1, this will result in a very similar price movement in the option value as well.

- The investor may employ this strategy to benefit from the leveraging nature of options, you may also see LEAPS below.

- The stock trades above the strike price of the put and the put option expire worthless.

- The stock fall below the strike price and

- exercise the option and sell the stock at the strike price and profit from the lower current market

- close out the long put position in a profit.

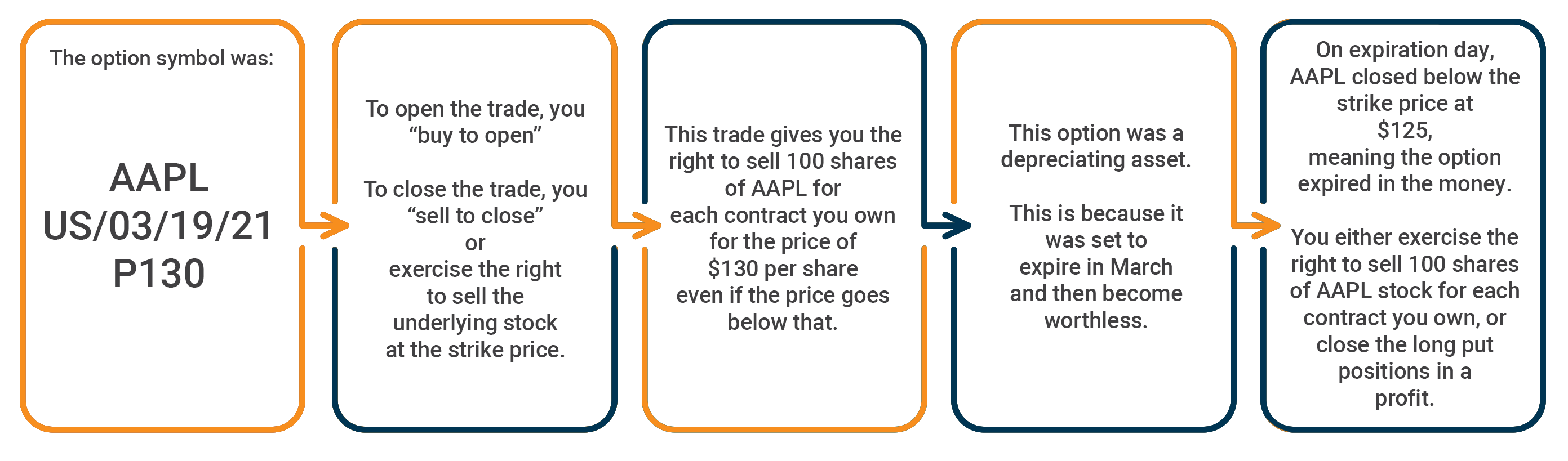

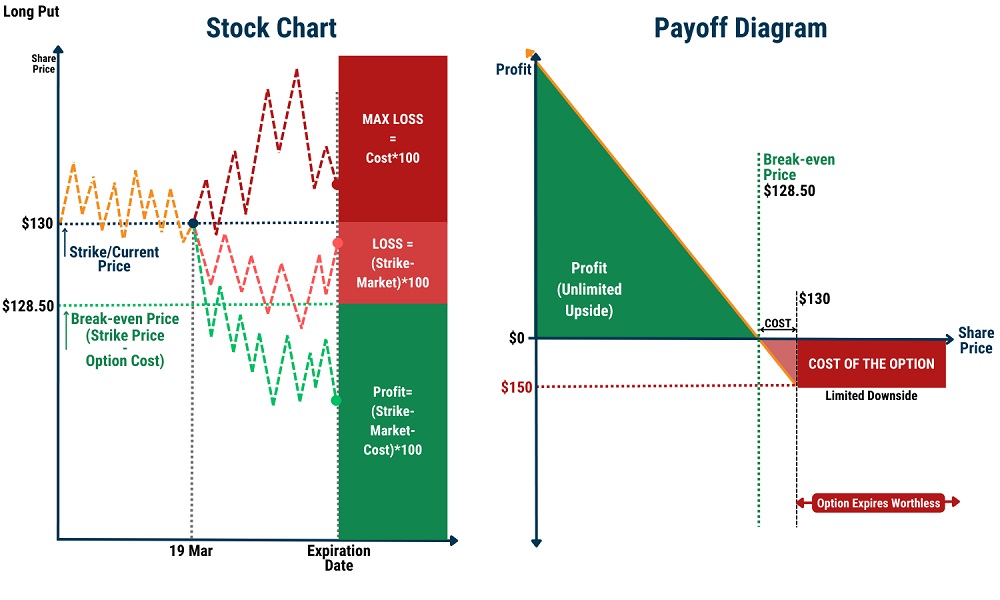

Long Put Trade Example

The trade was the Apple (AAPL) March 19th $130 Long Put (AAPL US 03/19/21 P130). You paid $150 ($1.50 x 100 shares) when you long the put and at expiration, the option was in the money. The seller is obligated to buy the stock from us on Mar. 19, 2021, or you may close the long put position in a profit. Below are the details of the trade broken down step-by-step.

Long Put Stock Chart and Payoff Diagram

A long put can be combined with a stock purchased previously to form a Protective Put.

This is a form of insurance against a decline in stock price which may result from events such as poor Earning Release or short-term bearish sentiment on the stock.

Protective Put Trade Example

Trade: Apple (AAPL), 19 March, $130 Long Put (AAPL US 03/19/21) bought and combined with the underlying stock holding of 100 shares of AAPL trading at $130. Near-term volatility or bearish sentiment may cause AAPL stock price to decline below $130 and cause a loss in the investment of the AAPL stock.

This decline however, will result in the AAPL Long Put to be more valuable and ITM hence offsetting the loss. Investors may close out the long put position in profit or “put” 100 shares of AAPL to the obligated seller at the exercise price of $130.

A covered call strategy involves selling an option to collect premium as income. For this strategy you will need to have the underlying stock before executing the strategy. Selling a call obligates you to sell 100 shares of a stock, which would be a bad idea if you don’t already own the stock. After all, you’d have to go out and buy 100 shares on the open market and then sell them back to the option buyer. But if you already own shares of the underlying stock, you wouldn’t have to buy shares to sell to the call buyer.

The shares you already own would “cover” the call you sold, hence the term “covered call.” Covered calls are ideal for generating income on stocks you already own. Rather than letting the stocks sit idle in your equity account, it can be used to generate extra income by doing covered calls on top of also profiting from the increase in price of the underlying stocks.

Stocks with high volatility (such as Tesla, Alibaba,) are great with generating more income due to the volatility priced into the option premium. This strategy can be utilise to generate constant income by rolling forward on the covered call contracts (ie. Extending the expiry date). Do take note if the covered calls expired ITM, the underlying needs to be delivered at the exercise price.

There are two potential outcomes when selling a call option:

- The stock rises past the strike price and the call seller is obligated to sell 100 shares of the stock for the strike price.

- The stock does not rise past the strike price and the call expires worthless, allowing the seller to keep the entire premium. Most of the time, we will buy back a call write that is out of the money and has lost most of its value.

Covered Call Trade Example

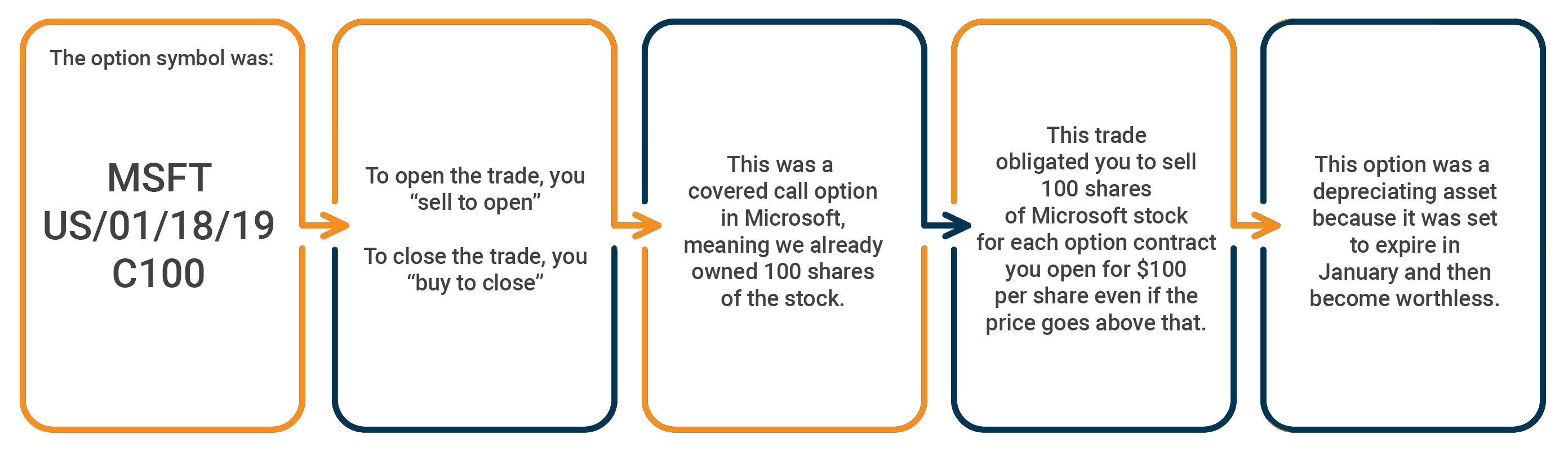

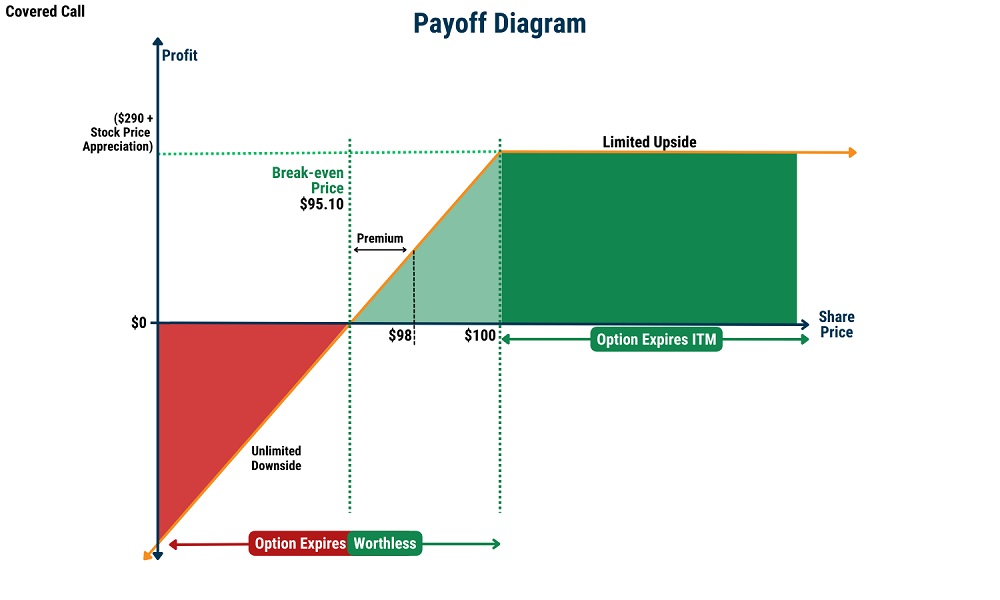

(1)The trade was the Microsoft (MSFT) January 18th $100 Covered Call while your average cost for MSFT stock is at $98. You earned ($2.90×100 shares) when we sold the covered call and, at expiration, the call expire worthless if MSFT trade below $100.

Below are the details of the trade broken down step-by-step. The trade was a covered call trade in Microsoft with an expiration date of Jan. 18, 2019. We expected the stock stay below $100 through expiration.

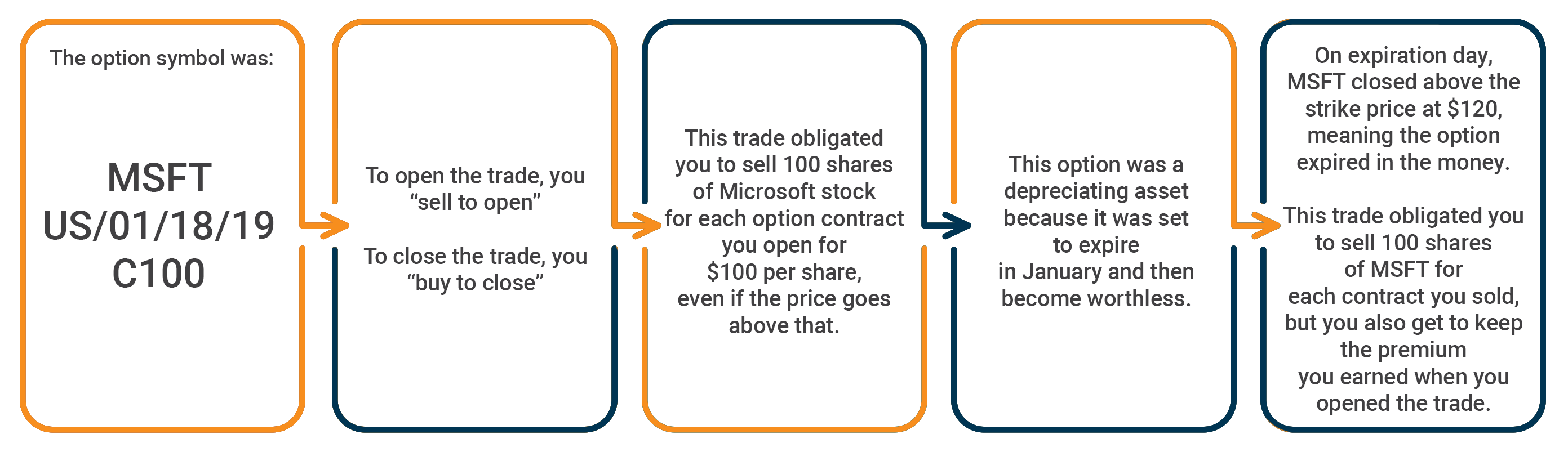

(2) The trade was the Microsoft (MSFT) January 18th $100 Call Write while your average cost for MSFT stock is at $98. You earned ($2.90×100 shares) when you sold the covered call and, at expiration, the option was in the money.

The buyer call the stock from us on Jan. 18, 2019, but we still got to keep the $290 in premium we received for selling the option.

Below are the details of the trade broken down step-by-step.

Covered Call Payoff Diagram

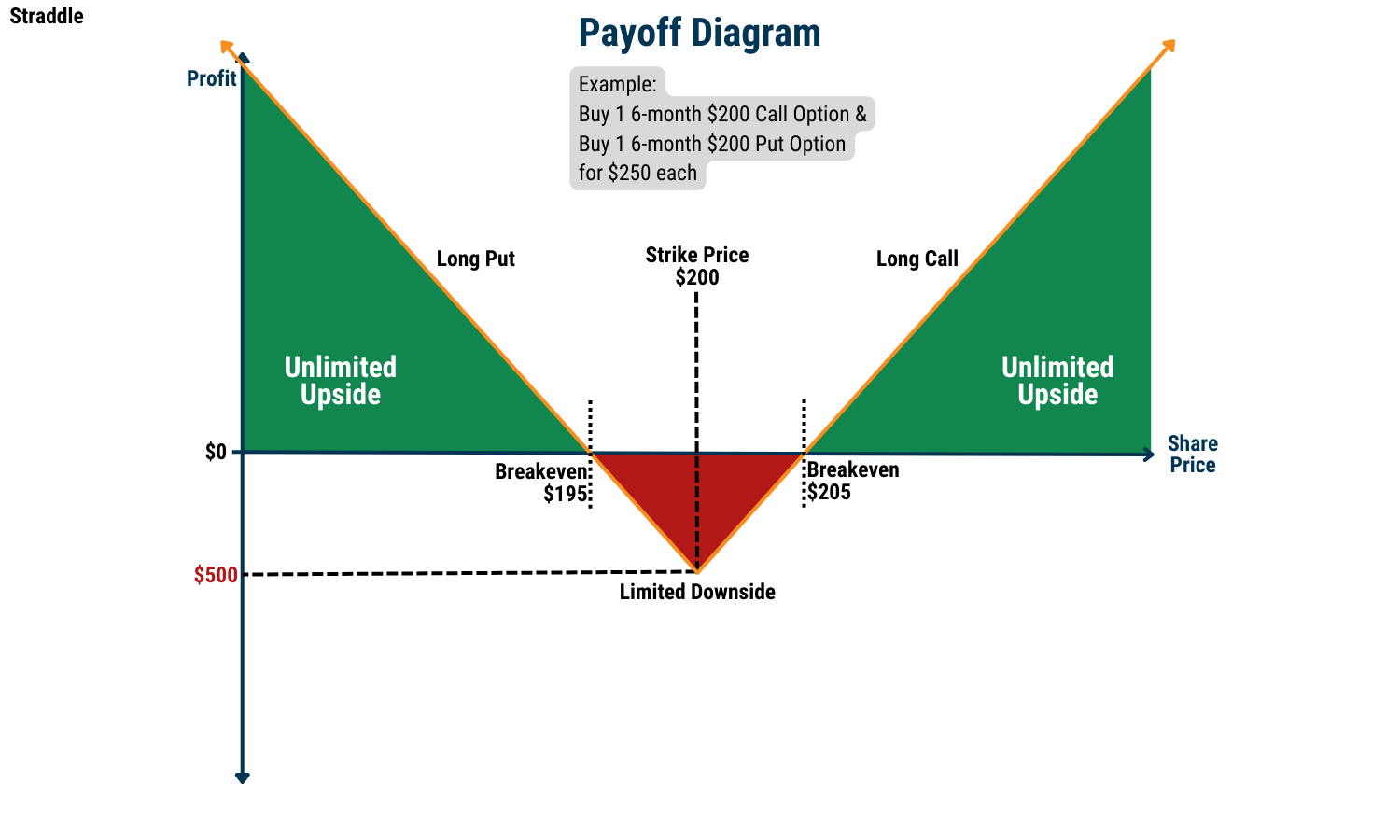

Straddle

A long straddle strategy involves both a Long Put and Call on the same underlying same strike price with the same expiration date.

The primary motivation behind this strategy is to profit from drastic movement (in either direction) of the stock price. This can take place during Earnings Announcements, where results might be unpredictable, potentially resulting in a huge impact on the stock price, causing it to deviate greatly.

Straddle Trade Example

Trade: Tesla (TSLA), 28 April, Long Call (TSLA US 04/28/23 C200) and Long Put (TSLA US 04/21/23 P200) bought with the underlying stock price of TSLA trading at around $200. On 27 April, TSLA announced a better (or worse) than expected Earnings results, causing TSLA stock price to move drastically.

This movement caused the Long Call (or Put) to be deep ITM, the position can be closed out in profit. Due to the drastic changes in price, the position that was deep ITM will cover for the initial investment in both Long Call and Put.

*Do note that volatility spikes that take place prior to earnings announcements will mean that the cost of options are usually more expensive and the resultant volatility post-announcement may result in a loss even though the options position moved ITM.

Straddle Payoff Diagram

Straddle Variants

There are multiple variants to the Straddle Strategy:

Strangle

Buy both Long Call and Long Put, with the strike price of the Call HIGHER than that of the Put. This will result in a lower premium paid (OTM options are cheaper than ATM/ITM options). The drawback to this would be that the price movement would have to be even more drastic for the position to be profitable.

Strip

Buy both a Long Call and Long Put with the quantity of the Put HIGHER than that of the Call (e.g. Long 1 Call and 2 Puts). This strategy relies on drastic stock price movement(s), biased towards a decrease in stock price.

Strap

Buy both a Long Call and Long Put with the quantity of the Put LOWER than that of the Call (e.g. Long 2 Calls and 1 Put). This strategy relies on drastic stock price movement(s), biased towards an increase in stock price.

LEAPS – Long-term Equity Anticipation Securities

LEAPS are long-term options that are still at least a year from expiration. They behave identical to that of other options, only difference being the longer expiration date. Besides the longer shelf life, LEAPS will also be deep ITM with a delta value of 0.80 or higher (-0.80 for Puts) at the chosen strike price. The high delta value essentially allows the LEAPS option to behave similarly to a stock in terms of price movement, for example a 0.80 delta option will move $0.80 for a $1 move of the underlying stock.An Example of LEAPS

AMZN stock is currently trading at $100, a LEAP option will be one where the expiry date is a year or more away and the option strike price chosen has a delta of 0.8 or more. For example, if today is 10 February 2023, the chosen AMZN call option has an expiry at 10 December 2025, a strike price of $50, delta value at 0.93 and currently trades at $60. Whenever the stock price moves $1, the option will move $0.93 or more depending on the delta. We see that the option price moves with a 93% similarity to the stock itself and investors using much less capital for the position.Cash Secured Put

A cash-secured put strategy involves selling a put option to collect premium as income while ensuring you have enough cash on hand to buy the underlying stock if assigned. For this strategy, you will need to set aside sufficient capital to purchase 100 shares of the stock at the strike price before executing the trade. Selling a put obligates you to buy 100 shares of the stock if the option is exercised. If you don’t have the necessary funds, you might face liquidity issues or be forced to close the position at a loss.

Cash-secured puts are ideal for investors looking to generate income while potentially acquiring stocks at a discount. If the stock price remains above the strike price by expiration, you keep the premium without having to buy the shares. If the stock drops below the strike price and you are assigned, you purchase the shares at the agreed-upon price, often at a lower effective cost due to the premium received.

There are two potential outcomes when selling a put option:

1. The stock falls below the strike price, and the put seller is obligated to buy 100 shares of the stock at the strike price, regardless of its lower market value.

2. The stock stays above the strike price, and the put expires worthless, allowing the seller to keep the entire premium.

Most of the time, traders will buy back a put option that is out of the money and has lost most of its value to lock in profits and free up capital for new trades.

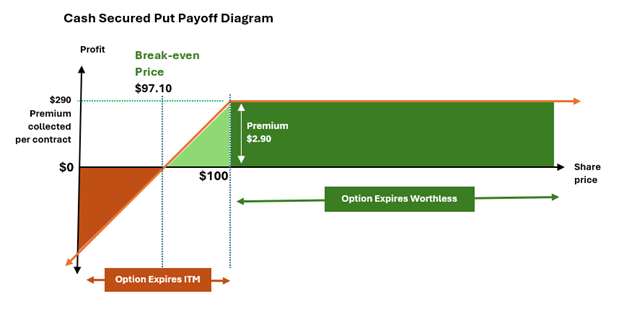

Cash-Secured Put Trade Example

Scenario 1: Put Expires Worthless

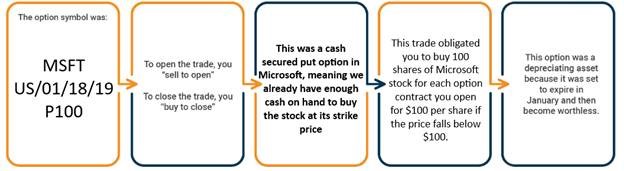

The trade was the Microsoft (MSFT) January 18th $100 Cash-Secured Put while you were willing to buy MSFT stock at $100. You earned ($2.90 × 100 shares = $290) when you sold the put option. At expiration, if MSFT trades above $100, the put expires worthless, and you keep the entire premium without having to buy the stock.

Below are the details of the trade broken down step-by-step. The trade was a cash-secured put in Microsoft with an expiration date of Jan. 18, 2019. We expected the stock to stay above $100 through expiration.

Scenario 2: Assigned the Stock

The trade was the Microsoft (MSFT) January 18th $100 Cash-Secured Put while you were willing to buy MSFT stock at $100. You earned ($2.90 × 100 shares = $290) when you sold the put option. At expiration, the option was in the money, meaning MSFT traded below $100, and the put buyer assigned the stock to us at $100 per share. However, we still kept the $290 in premium received for selling the option, effectively lowering our cost basis on the purchased shares.

Below are the details of the trade broken down step-by-step.

Minimum trade size: 1 contract which generally covers 100 underlying shares

| Action | Requirement |

|---|---|

| Long Call | Option premium |

| Long Put | Option premium |

| Short Call | Underlying asset |

| Short Put | 100% of strike price x 100 in available cash |

For positions unable to meet the obligations of options contracts (including auto-exercise) where the exposure risk is deemed excessive, one of the following actions will occur. Any proceeds will be credited/debited to the client prior to the contract’s expiry.

⦁ Liquidate Options prior to the expiration date

⦁ Allow the Options to lapse

⦁ Allow delivery and liquidate the underlying shares

All open positions should be rolled forward or closed before expiry if the client does not intend to exercise. Otherwise, they will be subject to one of the above actions. Force liquidations related to expiration typically commence two hours before market close, although we reserve the right to initiate this process earlier or later depending on prevailing conditions.

Manual exercising of options is available for positions that can meet the required obligations. Please submit the exercise request with the options contract details (symbol, expiration date, type of options, strike price, and quantity) by sending us an email at globalnight@phillip.com.sg no later than 2:00 A.M. SGT (3:00 A.M. SGT for non-DST). Any request submitted after the cutoff time will be handled on a best-effort basis.

The US Stock Option tab will only reflect positions and balance relating to US Stock Option(s). All trades are denominated in USD.

Order details

| Order Placement | Via 1) POEMS 2.0 Web 2) POEMS Mobile 3 |

|---|---|

| Trading lot(Minimum trade size) | 1 contract which generally covers 100 underlying shares |

| Live price | Via POEMS Mobile 3 or Poems Web (live Option price quote) |

| Order Type | Limit Order only |

| Minimum bid size | 0.01 (some subject to 0.05 increment bid) |

Trading Hours

| Singapore Time | 09:30pm – 04:00am (Daylight Savings Time) |

|---|---|

| 10:30pm – 05:00am (Non-Daylight Savings Time) | |

| US(Eastern) Time | 09:30am – 04:00pm |

*Order placement are allowed only during regular trading hours. Orders submitted outside of regular trading hours will be rejected, these includes orders in ETFs that trades an additional 15 minutes after regular close.

Settlement

| Settlement Date 1 | T+1 market days |

|---|---|

| Order Amalgamation | No |

| Settlement Currency | USD only |

1. Should the due date coincide with Singapore public holiday/s – The due date will follow the traded market’s due date

Transfer Timeline

Stock to Option | |

Cash transfer | Same day processing if request is made before 10am SGT, else T+1 |

Stock transfer | Same day processing if request is made before 3pm SGT, else T+1 |

Option to Stock | |

Cash transfer | T+1 processing if request is made before 10am SGT, else T+2 |

Stock transfer | T+1 processing if request is made before 3pm SGT, else T+2 |

US Options Live Prices

US Options Live Price feed is available for subscription FOR FREE on the web portal if you are a non-professional investor. Each subscription will go on for 12 months, and is not auto-renewed. After a 12-month subscription period, your US Options Live Price Feed will expire. Users will have to re-subscribe if they want to continue enjoying the US Options Live Price Feed for the next 12 months (at no additional cost).

For professional investors, you can subscribe to our US Options Live Price feed at SGD $45 monthly.

Please note: if you do not subscribe to the Live Price Feed, Option prices displayed are delayed by 15-30 minutes.

Only Option prices are live. In order to have accurate IV/Delta/Gamma, investors are advised to subscribe to both US Equities and Options live prices.

Options Price Increments

There may be instances where your Option order has invalid price increments.

Below is a summary of how Option price increments are determined.

In general, most Options trade in either nickel or dime increments depending on the price of the option.

| Nickel and Dime Increments Options | |

|---|---|

| Options Price | Price Increment |

| Below US$3 | US$0.05 |

| Above US$3 | US$0.10 |

However, there are some options that trade in increments of a penny or a nickel depending on the price of the option.

| Penny Program Pricing Increments | |

|---|---|

| Options Price | Increment |

| Below $3 | $0.01 |

| Above $3 | $0.05 |

The Options Clearing Corporation (OCC) maintains a list of equity options that are part of the Penny Program.

The list can be downloaded from the OCC website here.

How to activate stock options account (POEMS MOBILE 3 )

Video Guide

Screenshot Guide

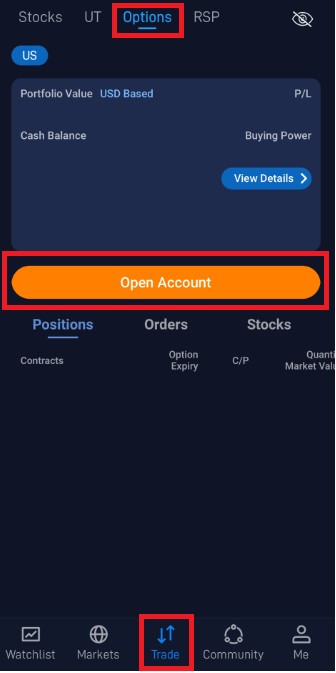

Step 1:

Navigate to (1)Trade > (2)Options and click on (3)Open Account

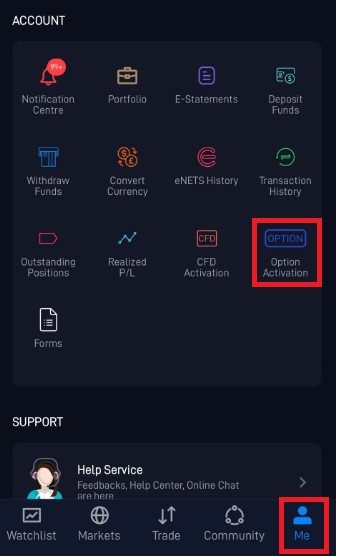

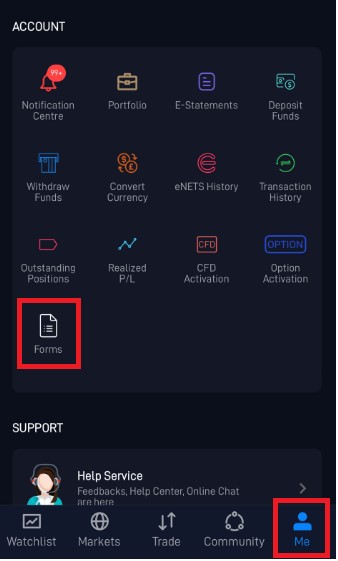

VYou can also navigate to (1)Me > (2)Option Activation to open Stock Option account

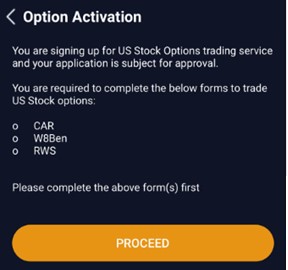

Step 2(inactive CAR/W8Ben/RWS):

Validation page for CAR/W8Ben/RWS. Click (1)Proceed to being filling up the respective forms

On click of respective forms, you will be redirected to fill up the forms.

*Do note CAR form can only be completed online on POEMS Web.

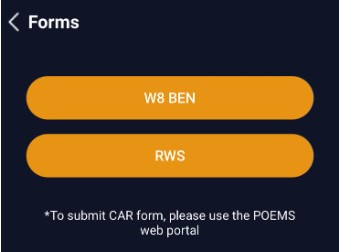

You may also submit W8Ben and Risk Warning Statement(RWS) under (1)Me > (2)Forms

Step 3(active CAR/W8Ben/RWS):

Redirect to acknowledge Option’s Risk Declaration Statement under ‘Option Activation’

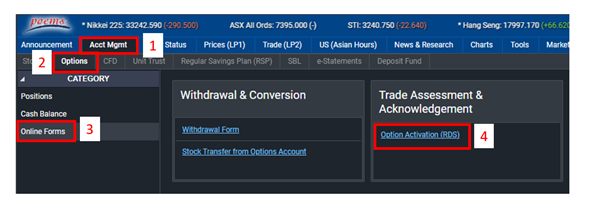

How to activate stock options account (POEMS WEB)

Screenshot Guide

Step 1: Acct Mgmt > Options > Online Forms > Options Activation (RDS)

Step 2: Upon clicking Options Activation (RDS) you will be prompt to acknowledge the risk disclosure for Options

How do I place a trade? (POEMS MOBILE 3)

Video Guide

Screenshot Guide

Step 1:

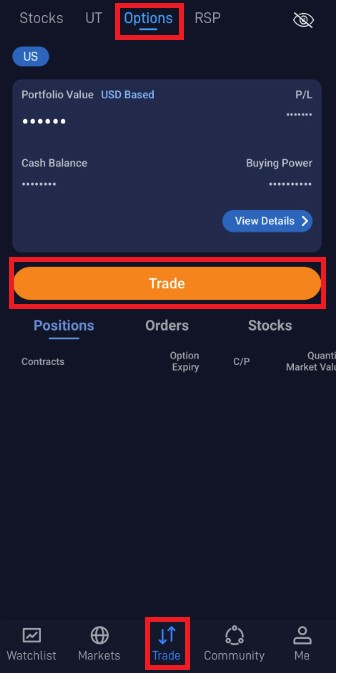

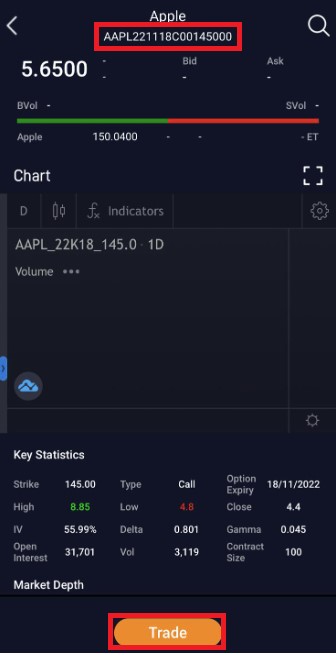

To place a trade, navigate to (1)Trade > (2)Option > (3)Trade

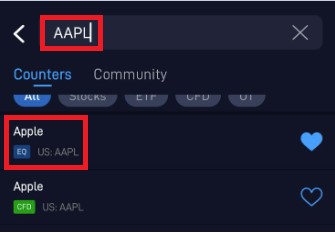

In the search bar, (1)search for the underlying counter > (2)Select the specific counter under EQ – Equity or ETF – Exchange Traded Funds respectively

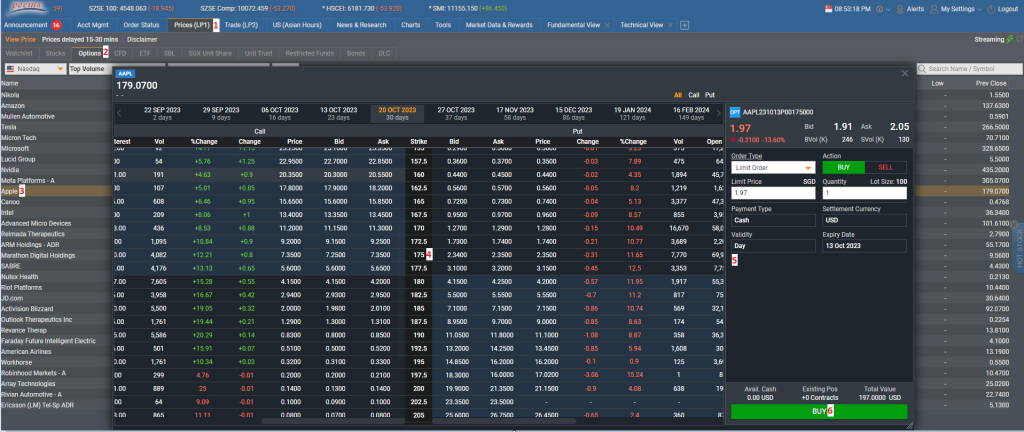

Select (1)Option and under the option page, you may choose for the (2)Options types ie. Call or Put to displayed separately or All to be displayed together. (3)Select the expiry date and the (4)Strike price respectively

(1)Show the option symbol and click on (2)Trade

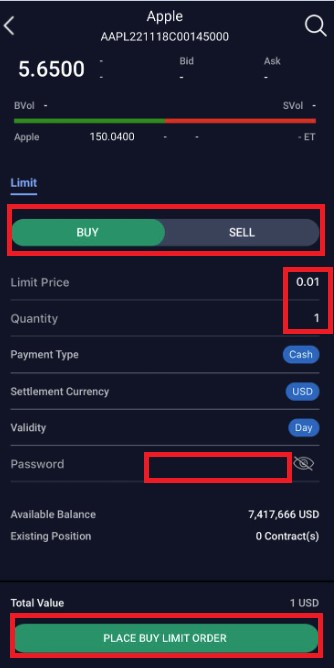

Select (1)Buy or Sell > (2)Input the limit price and quantity respectively > (3)Key in password > (4)Click on place order to submit order

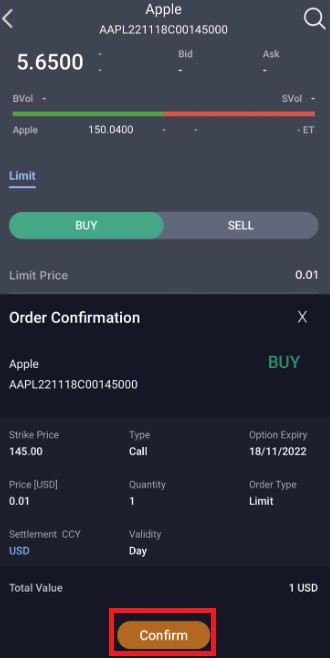

Order confirmation shown here, (1)Click on confirm to submit order

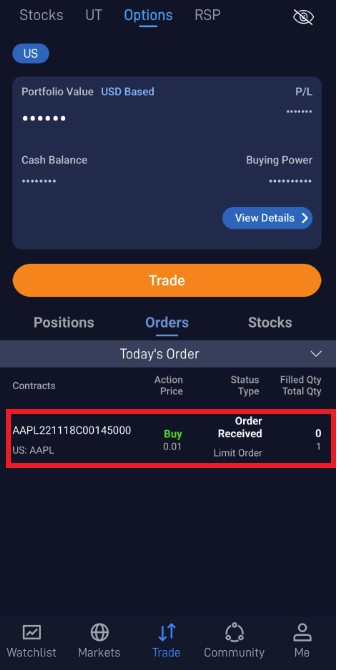

(1)Submitted order will be reflected under today’s order

How do I place a trade? (POEMS WEB)

Screenshot Guide

Step 1: Prices > Options > Select stock to launch Option Chain > Select contract to launch Trade Ticket > Fill in order details > Submit order

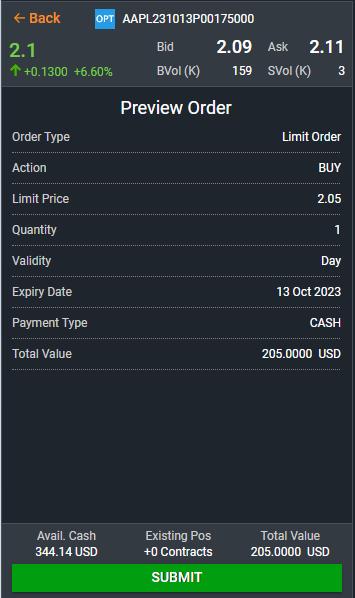

Step 2: Review order details and submit order

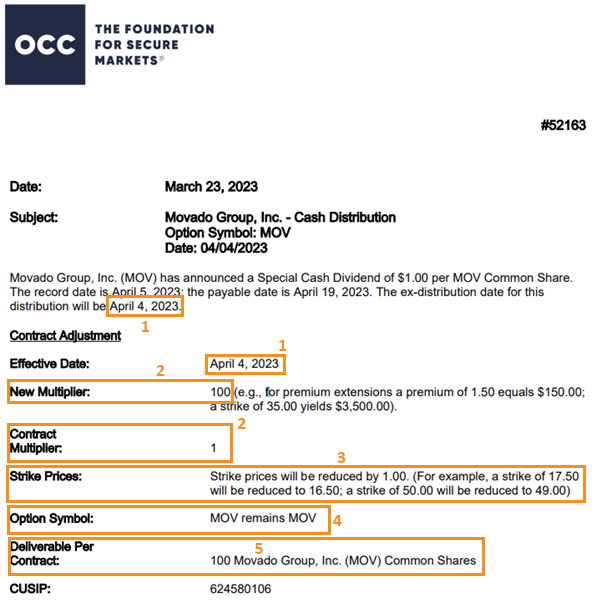

Special Cash Dividend

When a special cash dividend is issued, there are normally two scenarios.

Scenario A

The strike price of the options contract decreases accordingly.

The memo from OCC on MOV.US is explaining the following:

1. Options opened before 4 April 2023 will be adjusted

2. Multipliers remain unchanged

3. Strike price will all be reduced by $1.00

4. Option symbol remains unchanged

5. Deliverable remains unchanged

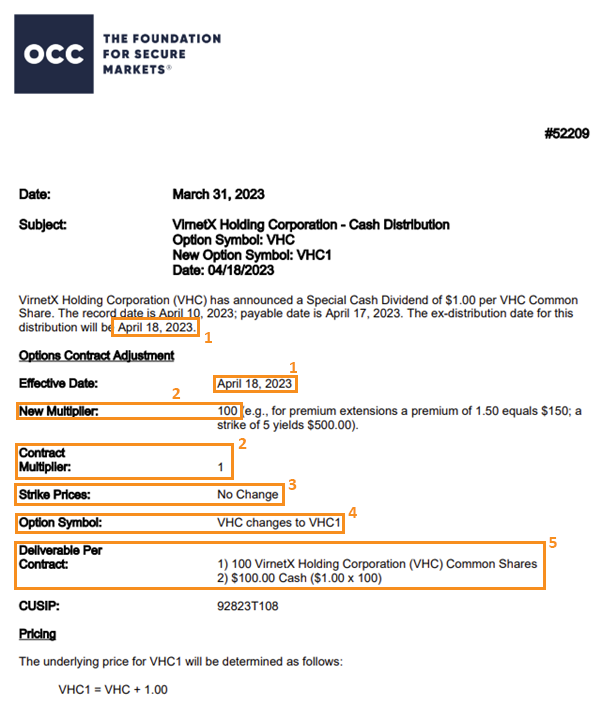

Scenario B

Strike price will remain unchanged with a change in option symbol and an additional deliverable of the cash distribution.

The memo from OCC on VHC.US is explaining the following:

1. Options opened before 18 April 2023 will be adjusted

2. Multipliers remain unchanged

3. Strike price will remain unchanged

4. Option symbol change from VHC to VHC1

5. Contract deliverable per contract will consist of:

a. 100 VHC.US common shares

b. $100 cash per contract.

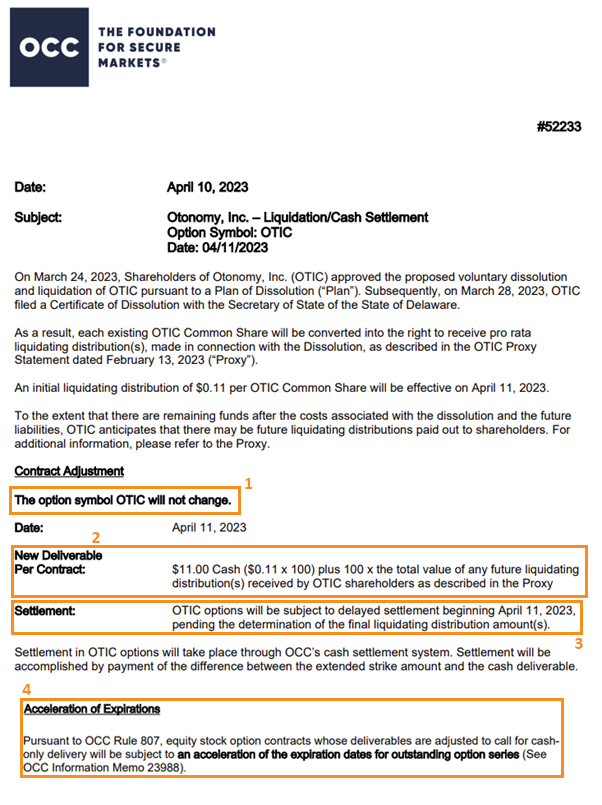

Liquidation

When the underlying stock liquidates and ceases trading in the market, the shares that make up the contract will turn into the cash-per-share amount the company allocates. Thus, the contract will be valued 100 times more than the company’s chosen pay out for each share.

Both the Symbol and Strike price will not change, but the Options Clearing Corporation (OCC) will bring forward the expiration date for the contract.

The memo from OCC on OTIC.US is explaining the following:

1. Option symbol will remain unchanged

2. Contract deliverable per contract will be $11.00 ($0.11 x 100) plus any future liquidating distributions.

3. There will be a delay in settlement from 11 April 2023

4. The expiry date of the option will be brought forward

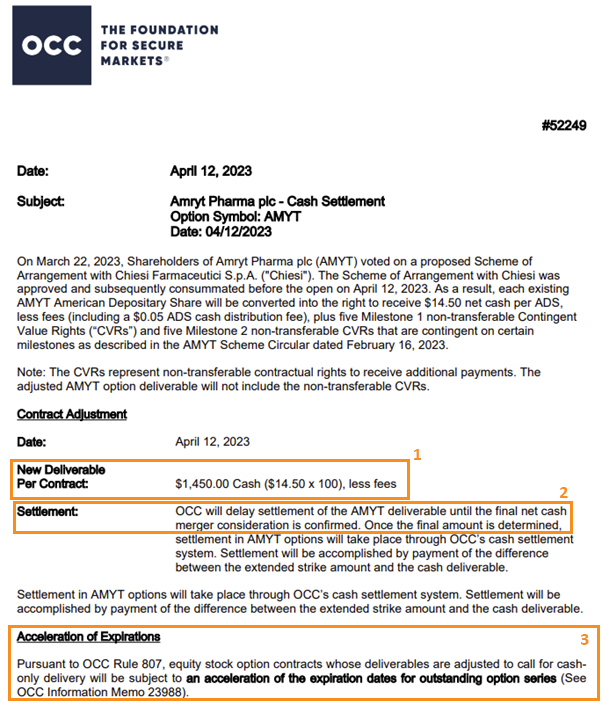

Acquisition

When the underlying stock gets acquired and ceases trading in the market, the expiration will be accelerated with the shares that make up the contract, turning into the cash-per-share amount that the company allocates.

The memo from OCC on AMYT.US is explaining the following:

1. Contract deliverable per contract will be $1,450.00 ($14.50 x 100) less fees

2. Settlement will be delayed until the final net cash merger consideration is confirmed

3. The expiry date of the option will be brought forward

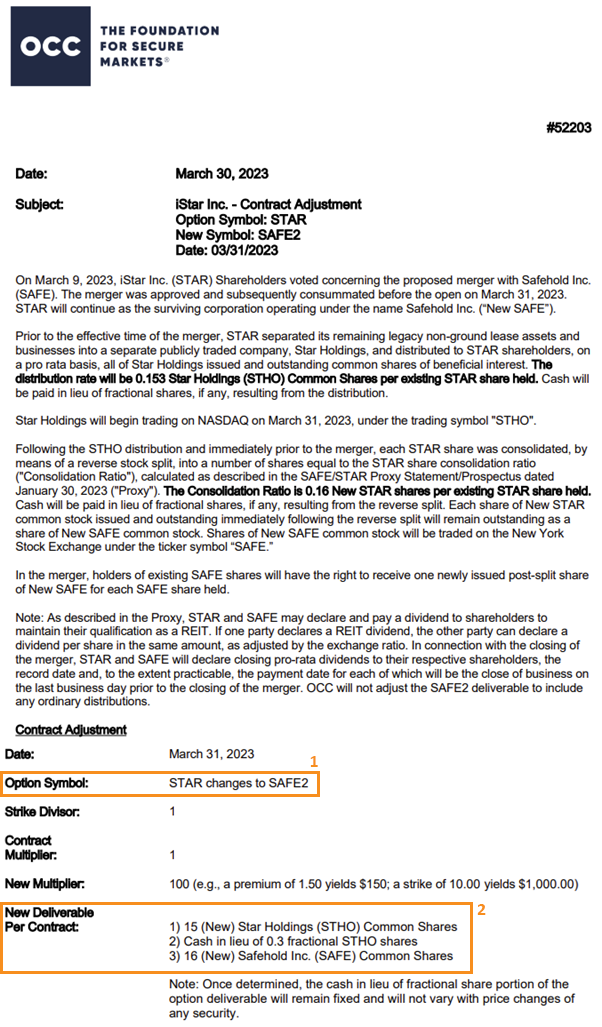

Cash and Stock Merger

In the event of a cash and stock merger, please note that the ticker of the options contract will change. The number of shares in the contract will also vary based on the merger conditions and deliverables that may include shares along with cash. Both the Strike price and Expiration date will however remain the same.

The memo from OCC on STAR.US is explaining the following:

1. Option symbol will change to SAFE2

2. Contract deliverable per contract will be:

a. 15 STHO.US common shares

b. Cash in lieu of 0.3 fractional STHO.US common shares

c. 16 SAFE.US common shares

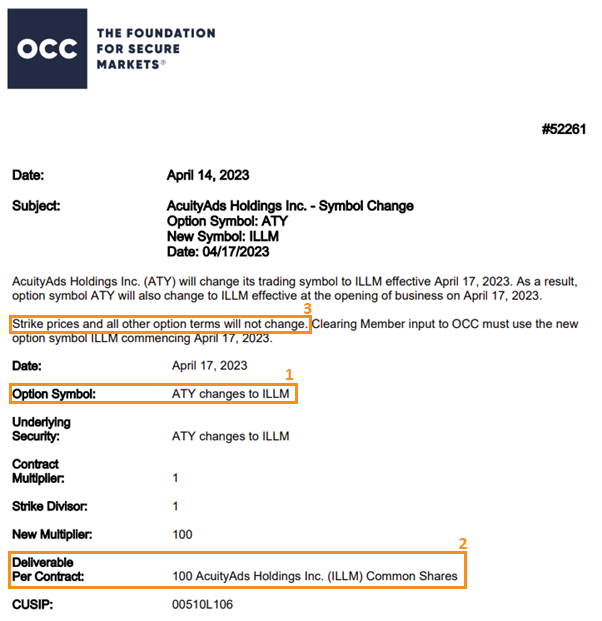

Ticker Change

During a ticker change, the Options contract will change to reflect the new ticker of the underlying stock. Both the Strike price and Expiration date will however, remain unchanged.

The memo from OCC on ATY.US is explaining the following:

1. Option symbol will change to ILLM

2. Contract deliverable per contract will be 100 ILLM.US shares

3. Strike price and other options terms will remain.

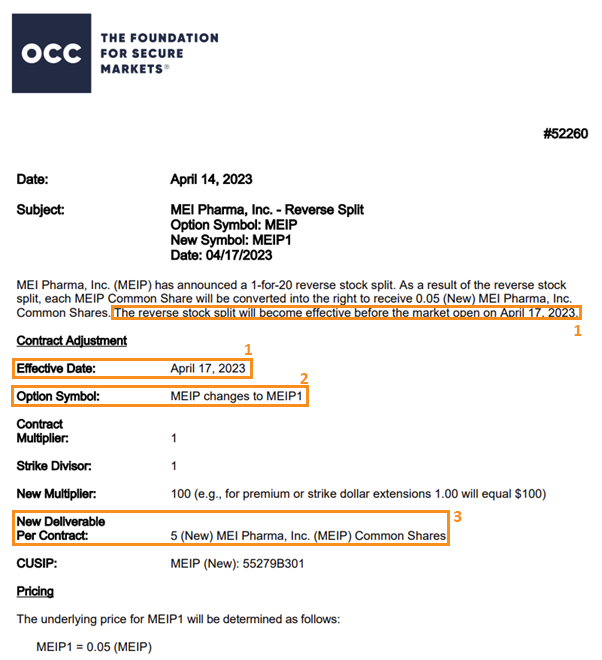

Reverse Split

During a reverse split, there will be a number that is added to the ticker of the Options contract. The number of shares in the contract will decrease based on the conditions of the reverse split. Both the Strike price and Expiration date will however, remain unchanged.

The memo from OCC on MEIP.US is explaining the following:

1. Options opened before 17 April 2023 will be adjusted

2. Option symbol will change to MEIP1

3. Contract deliverable per contract will be 5 (new) MEIP.US shares

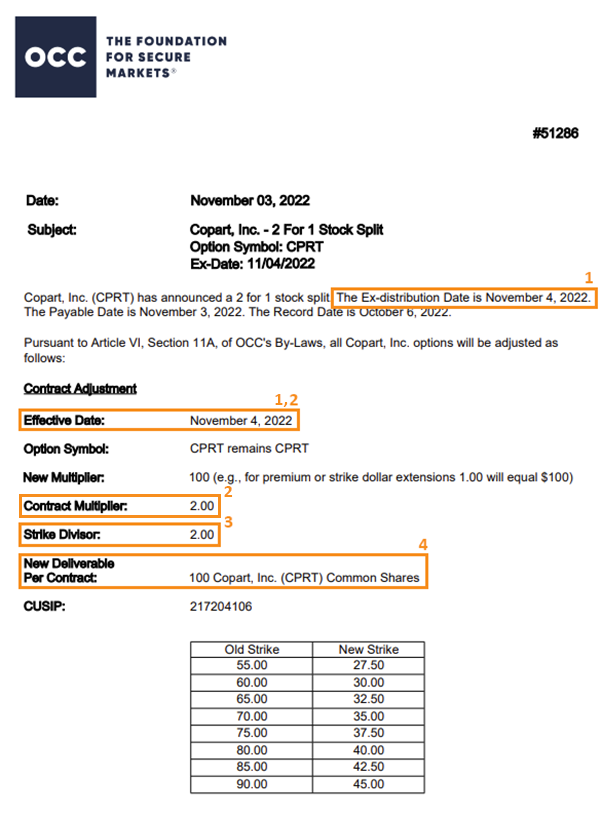

Forward Split

Forward splits are the division of the outstanding shares of a company into a larger number of shares. When a forward split occurs, there are normally two types of possible scenarios:

Scenario A

When the forward split results in a round number. (e.g. 2 for 1, 5 for 1, 10 for 1)

⦁ The ticker and expiration date will remain the same if you have Options on a stock that undergoes a forward split. The Strike price however, will be divided by the forward split multiplier.

The memo from OCC on CPRT.US is explaining the following:

1. Options opened before 4 Nov 2022 will be adjusted

2. Holders of the contract before 4 Nov 2022 will hold double the number of option contract

3. Strike price will be divided by 2. E.g. the old options contract with a strike price of $55 is adjusted to $27.50 ($55/2)

4. Contract deliverable per contract will still be 100 CPRT.US shares

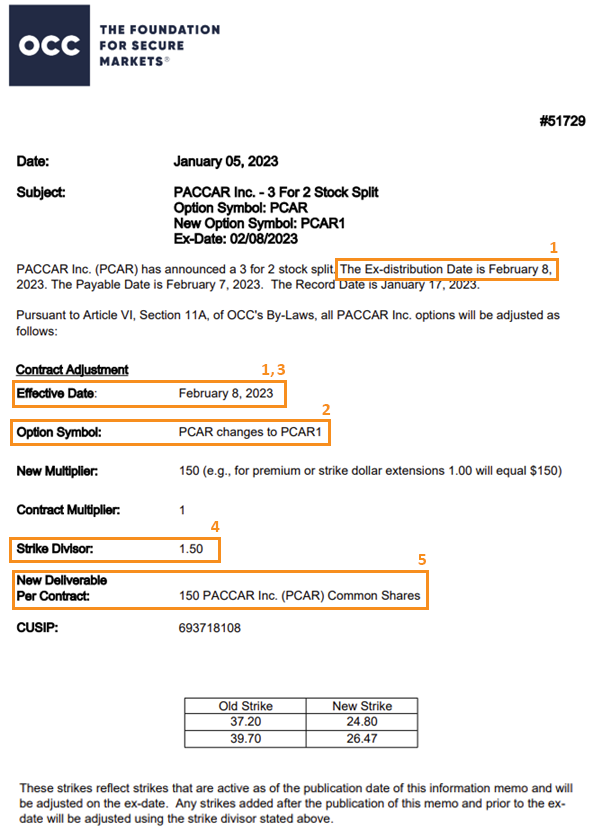

Scenario B

When the forward split does not result in a round number (5 for 4, or 3 for 2):

⦁ There is a change in symbol

⦁ Number of contracts remain the same but the deliverable of the contracts increase according to the forward split multiplier

⦁ Strike price decreases by the strike divisor

The memo from OCC on PCAR.US is explaining the following:

1. Options opened before 8 Feb 2023 will be adjusted

2. The option symbol is changed to PCAR1

3. Holders of the contract before 8 Feb 2022 will hold same number of option contract

4. Strike price will be divided by 1.5. E.g. the old options contract with a strike price of $37.2 is adjusted to $24.80 ($37.2/1.5)

5. Contract deliverable per contract will increase to 150 PCAR.US shares

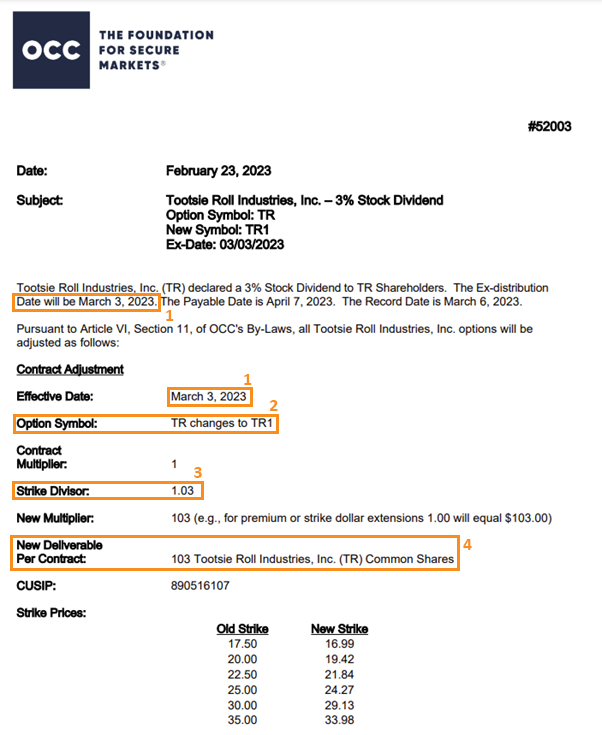

Stock Dividend

When the firm pays a stock dividend, the Option’s strike price will lower and the number of deliverable shares in the contract will increase by the amount of the dividend. There will be a number that is added to the ticker of the Options contract if the firm of the underlying stock is issued a stock dividend.

The memo from OCC on TR.US is explaining the following:

1. Options opened before 3 Mar 2023 will be adjusted

2..The option symbol is changed to TR1

3. Strike price will be divided by 1.03. E.g. the old options contract with a strike price of $17.50 is adjusted to $16.99 ($17.50/1.03)

4. Contract deliverable per contract will increase to 103 TR.US shares

Spinoff

When the firm of the underlying stock executes a spinoff, the number of shares in the contract will remain the same. In addition to the existing shares, the new shares paid out by the issuing firm will be included in your contract. During a spinoff, there will be a number that is added to the ticker of the options contract.

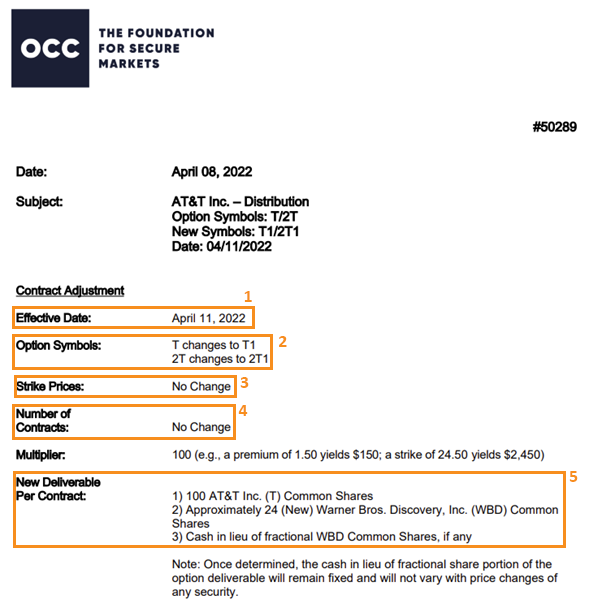

The memo from OCC on T.US is explaining the following:

1. Options opened before 11 Apr 2022 will be adjusted

2. The option symbol is changed to T1 and 2T1

3. Strike price remain unchanged

4. Number of contracts remain unchanged

5. Contract deliverable per contract will consist of;

a. 100 T.US shares

b. 24 WBD.US shares

c. Cash in lieu

Are there any forms required prior to trading Options?

- Active W8Ben

- Acknowledged Risk Warning Statement (RWS)

- Passed Customer Account Review (CAR)

- Acknowledged Option Risk Disclosure Statement (Option RDS)

What are the eligible account types to trade Options?

The eligible account types are Cash Management (KC), Margin/Cash Plus (M), Prepaid (CC), and Custodian (CU) accounts.

Additionally, the trading account should also be opted in for e-statement.

How long is the approval process for Option Activation?

If acknowledgement of Options RDS is done before 6.15pm SGT, the option sub-account will be activated the next business day (T+1) by 4.00pm SGT, otherwise it will take up to 2 business days (T+2), excluding any SG/US holidays.

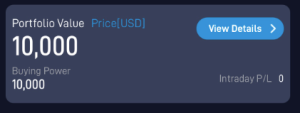

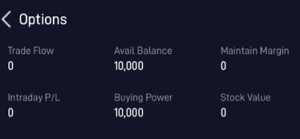

How do I read the Option Portfolio balance?

· Portfolio Value: Total portfolio valuation which is the aggregate of all positions(Equities and Options) and cash balance.

· Buying Power: Amount available for trading. It is calculated as SOD Cash Balance +(Sell added upon fill) OR -(Buy to open deducted upon order placement) premiums for option trades.

· Intraday P/L: P/L for all option positions. It is calculated based on the mid price of bid & ask quotes with previous close as reference price.

· Trade Flow: Intraday total cash flow from option trades. It is calculated as negative for buy trades and positive for sell trades.

· Avail Balance : Amount available for trading. It is calculated as SOD Cash Balance +(Sell added upon fill) OR -(Buy deducted upon order placement) premiums for option trades.

· Maintain Margin: Margin requirement for option positions.

· Intraday P/L: P/L for all option positions. It is calculated based on the mid price of bid and ask quotes with previous close as reference price.

· Stock Value: Market value of stock positions

Example to calculate Portfolio Value

Available Balance = Buying Power = Cash available for trading = 6,528.72

Maintenance Margin = Cash earmarked for cash secured puts position = 3,800

Stock Value = 2,198

Options Value (Market Value) = (-15) + (-30) + (-76) + 6,110 = 5,989

Portfolio Value = Available Balance/Buying Power + Maintenance Margin + Stock Value + Options Value

18,515.72 = 6,528.72 + 3,800 + 2,198 + 5,989

Why are Exercise/Assignment activities not shown on the same day of the e-statements?

As exercise/assignment activities are processed after the market has closed, it will only be shown on the e-statements on T+2.

Do note however, portfolio balances and positions are updated accordingly prior to market open on T+1.

What are some of the common reasons for order rejection?

• Account does not have enough position: The order quantity must be equal to or less than your current position as the account does not have sufficient holdings. No splitting of orders.

• Account does not have enough balance: The Buy open gross amount should be equal or less than the available balance.

• Insufficient Stock position to cover: Sell to Open positions will be rejected if not covered by the underlying stock i.e. Covered Call.

• Short Put Option is not allowed.

How do I transfer funds into my Options Account?

How do I transfer stocks into my Options Account?

Transfers can be done via the POEMS Mobile 3 App and there will be no applicable changes for transfers between these accounts. For detailed steps, please refer to the image below:

![]()

![]()

Why is there a need to transfer funds/stocks prior to trading options?

Option ledger is kept separately from the main Poems equity account ledger, as such option sub-account will only have activities related to options only. Any liquidation of shares in the option sub-account will need to be transferred back to the main Poems equity account.