- Completed redevelopment at 3 Tuas Ave 2, which will strengthen cash flows

- Dialed down exposure to CWT from 7.9% to 4.8% gross rental income

- Warehouse supply in Singapore expected to taper in 2020-2023, while AAREIT searches for new tenants for their multi-tenant lease properties

- Stand to benefit from extension of Land Intensification Allowance (LIA) scheme, option to develop under-utilised portfolio

AIMS APAC REIT (AAREIT) shows signs of resilience amid a stabilizing industrial property environment. We point out the REIT’s status at this moment, and the path they have ahead.

Company Background

AIMS APAC REIT, formerly MacarthurCook Industrial REIT, is an industrial REIT listed on the SGX in 2007. AAREIT has a market cap of S$1.006 billion, with a portfolio of 27 industrial properties based in Singapore and Australia – 25 of which are located throughout Singapore, and the remainder in Gold Coast, as well as a 49.0% interest in a business park, Optus Centre, located in New South Wales. AAREIT’s portfolio is valued at S$1.5 billion.

AIMS Financial Group (AIMS), the sole sponsor of AAREIT, is a diversified financial services and investment group, rated AAA by Standard & Poor’s and Fitch Ratings. AIMS APAC REIT Management Limited, the REIT manager of AAREIT, is wholly-owned by AIMS.

Holding a 8.05% stake, the group’s Chairman Mr. George Wang is a key stakeholder of AAREIT.

Expect new cash flow from 3 Tuas Ave 2

AAREIT expects to receive additional rental income from 31 March 2020 following the expiry of the fitting-out period and commencement of the master lease at 3 Tuas Ave 2. The c.25,000 sqm four-storey ramp-up industrial facility was under a redevelopment programme. Upon completion, additional revenue will elevate EBITDA interest cover, which stands at c.3.7x as of 31 December 2019.

Figure 1: 3 Tuas Ave 2

Source: Company

Portfolio occupancy slashed in one-off lease changes

In Q3FY2020, a conversion of properties from master leases into multi-tenant leases led to portfolio occupancy rates dropping from 92.2% to 89.4%. These properties are 1A International Business Park, a 19,949 sqm GFA business park catered to high-technology industries, including software development, research and ancillary support activities, and 20 Gul Way, a 153,892 sqm GFA five-storey warehouse and logistics facility.

We note that this is a one-off event and expect occupancy rates to remain stable as AAREIT focuses on new tenant search.

Figure 2: 1A International Business Park, Singapore

and 20 Gul Way

Source: Company

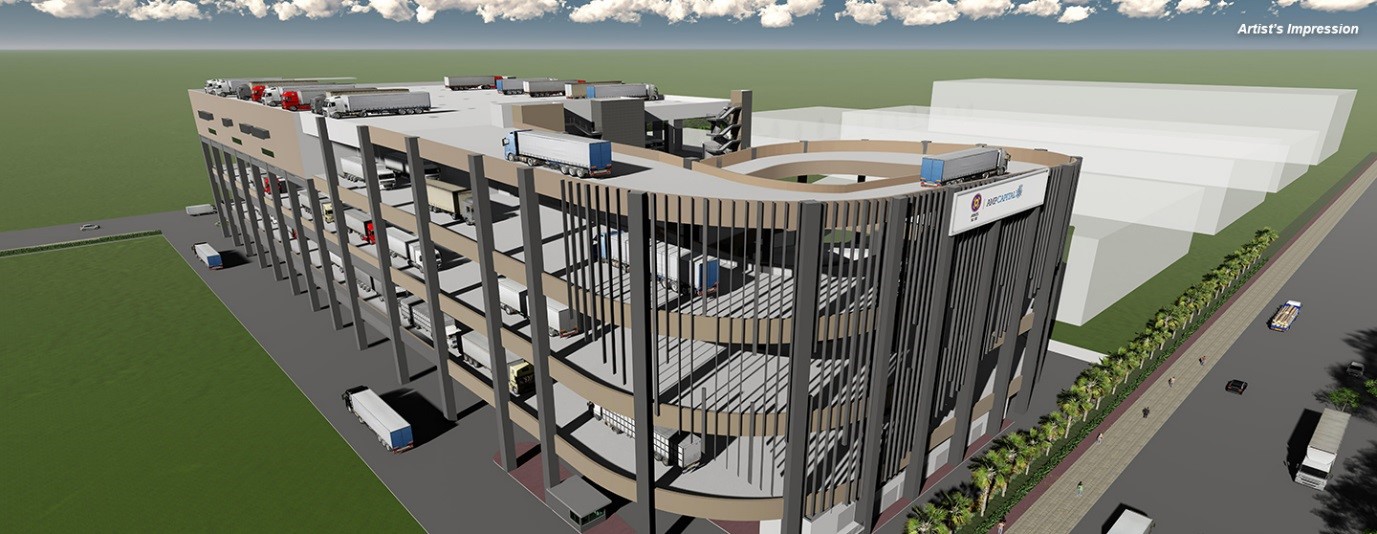

Encouraging logistics supply outlook

According to a Real Estate Market Outlook 2020 report by CBRE, warehouse supply in Singapore is expected to taper from 2020-2023. Average new warehouse supply per annum from 2020-2023 is estimated to be 1.53mn sqft, a significantly lower figure compared to the historical 10-year average of 4.42mn sqft from 2010 to 2019. This led to industrial property rentals stabilizing. AAREIT’s rental reversions have also held steady at c.-0.9% versus c.-24.6% a year ago, reflecting the more sanguine environment.

Figure 3: Singapore industrial property rental index exhibits stabilizing rental rates

Source: URA, CEIC

Despite this, Singapore warehouse vacancy rates remain high at 12.0%. As the virus situation affects economic growth, we expect vacancy rates to remain high and could offset against any rental gains.

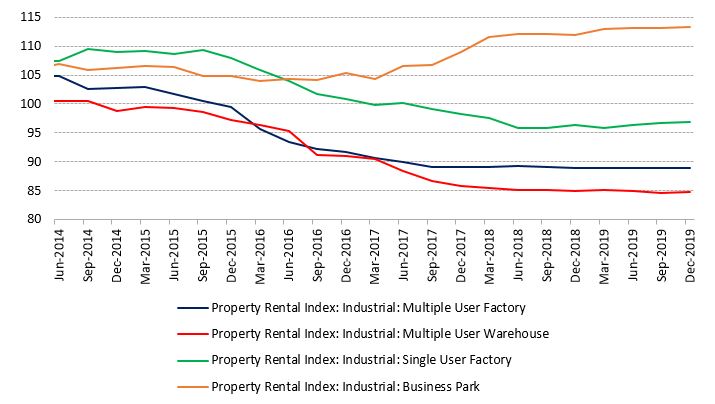

Well spread debt maturity profile

As at 31 December 2019, AAREIT’s debt maturity is well spread, with no more than 30% of total debt maturing in any year from FY2021 to FY2025, with gearing standing at a comfortable level of 35.2%, representing a large debt headroom from the MAS gearing limit of 45%. This gives AAREIT room to maneuver through economic troubles. At the moment, the group has S$185.5 million in undrawn credit facilities, sufficient to cover total debt maturing this year (FY2021).

Figure 4: Well spread debt maturity, with no more than 30% of total debt maturing in any one year

Source: Company

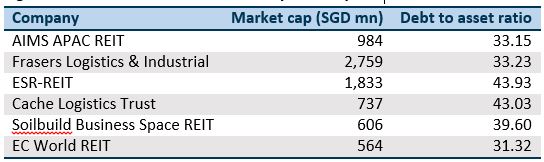

Figure 5: Debt to asset ratio is low compared to peers

Source: Bloomberg

Newly executed long-term lease agreement with top tenant

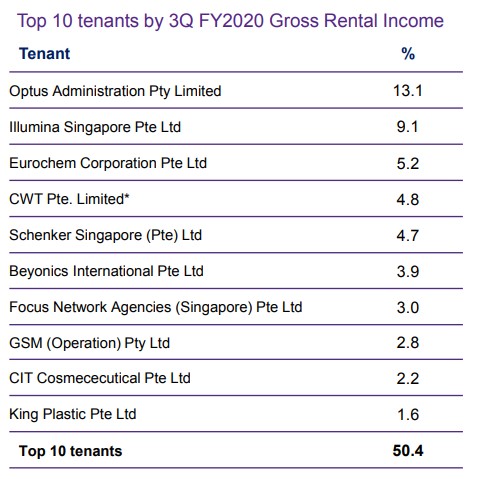

AAREIT serves a well-spread tenant base, with top ten tenants contributing 50.4% of total gross rental income (GRI) in 3QFY2020. The group’s top tenant, Optus Administration, contributed 13.1% of GRI, and is a wholly owned subsidiary of SingTel Group.

On 25 November 2019, AAREIT successfully executed a new 12-year lease with Optus Administration, commencing from 1 July 2021. The new lease is estimated to bring in c.AUD28.3mn in net property income (NPI) for the first year, with an average of c.AUD36.5mn NPI annually over the lease term, representing roughly c.40% of FY2019 NPI. This long lease term further extends AAREIT’s income visibilty.

Figure 6: Top tenant contributes 13.1% of gross rental income

Source: Company

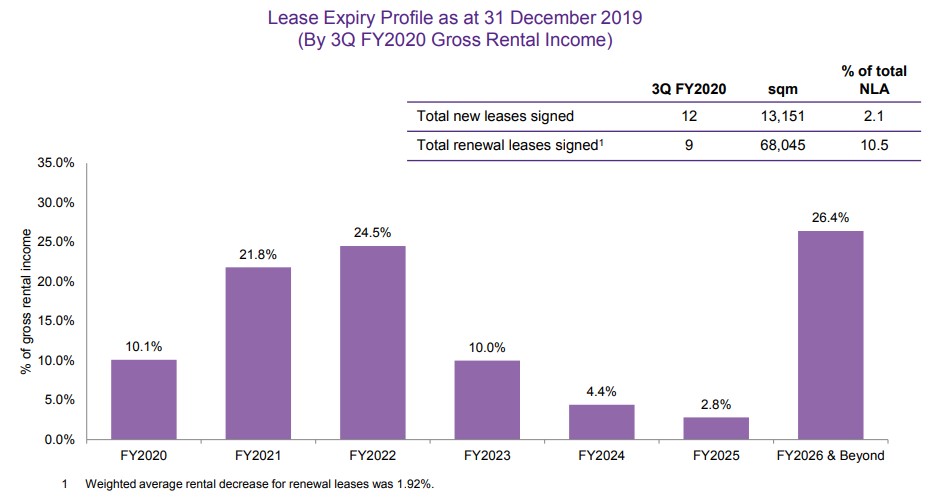

Better WALE of 4.01 years, up from 2.45 years

Within 3QFY2020, AAREIT secured a longer weighted average lease expiry (WALE) profile of 4.01 years, up from 2.45 years quarter on quarter (accounting for forward committed leases). 10.1% of GRI in the group’s portfolio is set to expire in the final quarter of FY2020. The group renewed c.6.5% of FY2020 expiring leases during 3QFY2020.

Figure 7: 10.1% of gross rental income leases set to expire in FY2020

Source: Company

CWT exposure dialed down

Upon expiry of all CWT Pte Ltd (CWT) leases at 20 Gul as at December 2019, the group’s exposure to the distressed company fell from 7.9% to 4.8% of GRI. Exposure is expected to decline an additional c.2.7% in FY2020 as more leases expire. CWT’s final lease at 30 Tuas West expires in July 2021 (2QFY2022).

In April 2019, CWT Pte Ltd suffered from a cross default tiggered by its parent, CWT International, placing concern over its lease obligations with several Singapore REITs.

Singapore Budget measures ideal for under-utilised portfolio development

AAREIT holds about 0.5mn sf in untapped gross floor area (GFA) in its underutilised portfolio, representing c.7% of existing net lettable area. To foster organic growth, the group has the option of developing the area, which we understand to be encouraged by the extension of the Land Intensification Allowance (LIA) scheme from 31 June 2020 to 31 December 2025 in the Budget 2020 measures.

The scheme encourages the intensification of industrial land use by providing an allowance of 25% for qualifying Capex incurred on construction/renovation/extension of an approved LIA building. This is to address the issue of depleting land reserves in Singapore.

Key financials