Previously known as ESR-REIT, the real estate investment trust company has merged with ARA LOGOS to form ESR-LOGOS Real Estate Investment Trust (“ESR-LOGOS REIT”). It began trading on Singapore Exchange Securities Trading Limited (SGX-ST) on the 5th May 2022. ESR-LOGOS REIT invests in income-producing industrial properties also known as New Economy* properties alongside its business parks, and it has a total of $5.5bn in total assets under management. Its portfolio consist of 84 properties located in Singapore (63 assets) and Australia (21 assets). ESR-LOGOS REIT current market capital stands at 2.736 billion as of 31st May 2022.

*New Economy are assets that includes warehouses, high specification industrial properties, logistics assets and data centres.

ESR-LOGOS REIT is sponsored by the ESR Group. ESR is a real estate asset manager and a real estate investment manager powered by the New Economy with a total asset under management (AUM) of US$140.2bn. Its development and investment management platforms spans across key APAC markets, including China, Japan, South Korea, Australia, Singapore, India, New Zealand and Southeast Asia. ESR is also expanding its presence in Europe and the US.

ESR-LOGOS Fund Management (S) Limited (previously known as ESR Fund management (S) limited) will continue to be the manager of the ESR-LOGOS REIT. ESR-LOGOS Fund Management (S) Limited is 67.3% own by ESR group, 25% by Shanghai Summit Pte Ltd and 7.7% Mitsui & Co Ltd.

ESR-REIT Financials in 1Q2022 (ending 31st March 2022)

Gross revenue fell by 1.16% y.o.y from $60.3 million in 1Q2021 to $59.6 million in 1Q2022). This reduction was mainly due to the divestment of 11 Serangoon North Ave 5, 3C Toh Guan Road East in 4Q2021 and 28 Senoko Drive, 45 Changi South Avenue 2 in 1Q2022. These divestments were to partially offset the acquisition of 46A Tanjong Penjuru ($119.6 million) and 10% interest in ESR Australia Logistics Partnership (EALP) ($62.6 million). Higher utilities expenses due to a hike in global energy prices also lowered Net Property Income by 10.4% y.o.y from $44.1 million in 1Q2021 to $39.5 million in 1Q2022. Portfolio rental reversion for 1Q2022 increased by 3.1% as compared to a negative 5% of rental reversion in 1Q2021. This was lifted by the positive rental reversions in logistics, general industrial and business park sectors. In terms of portfolio occupancy, ESR-REIT was at 91.5% in 1Q2022 vs 90.8% in 1Q2021. They have been consistently above JTC’s average of 90.2% in 1Q2022 and 89.9% in 1Q2021.

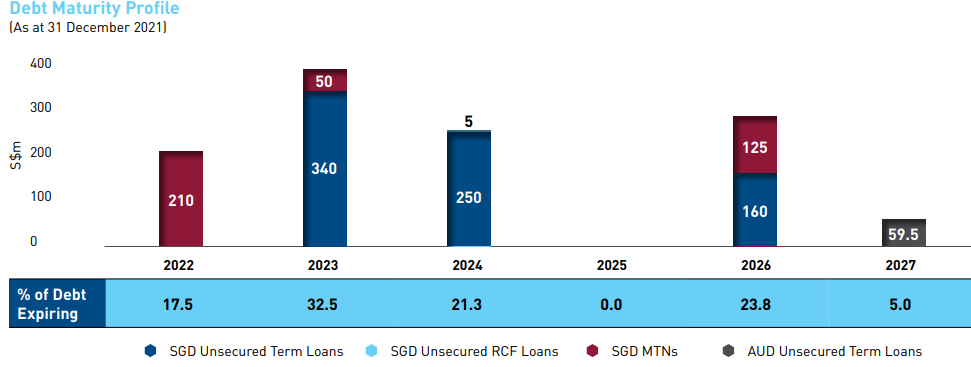

Credit Metric

ESR-REIT leverage ratio was at 39.5% in FY2021 (under MAS leverage limit of 50%) with 93.3% of its total borrowings on fixed interest rates over the next 1.7 years. Its portfolio remained unencumbered and the weighted average debt expiry for ESR-REIT as at FY2021 is at 2.4 years with no more than 32.5% of debt expiring in each year.

Source: ESR-REIT

As at FY2021 cash and cash equivalent is at $24.15 million and a (Cash to ST-Debt ratio) of 0.069 times.

Positives after the merger with ARA LOGOS

+Tapping into overseas market through the leverage of the sponsor. ESR-LOGOS REIT will be able to leverage on its sponsor’s established operations platform and local country resources to tap into overseas markets. This enables the firm to address its structural short land leases in Singapore’s industrial property sector thru the exposure to more freehold and longer land lease tenure assets which would strengthen their portfolio quality.

+Recalibration of their portfolio quality towards New Economy assets. After the merger, the firm’s exposure to logistics and high spec industrial sectors will be enlarged from (41.5% to 64.6%). This allows the firm to be better positioned in capturing the growing demand for New Economy sectors. (As seen in JTC 1Q2022 market report prices of industrial space has rose by 5.6% compared to the previous year)

+Potential projects and assets in the pipeline. Approximately US$2bn of visible and executable APAC New Economy assets available from the sponsor which ESR-LOGOS REIT will able to utilize to accelerate its growth. Additionally, ESR-LOGOS REIT will also have access to the sponsor’s assets of more than US$59bn in logistical assets.

+Increasing presence in Australia. With an additional 21 portfolio of Australian properties and the 2 additional funds from ARA LOGOS namely (New LAIVS Trust – 49.5% and Oxford property fund – 40%). It would certainly increase the exposure and presence to the Australian logistics market.

+Improvement in income diversification. With the merger, it reduces the income concentration risk which was previously fully made up from the Singapore sector to (87.1% in SG, 12.9% in Australia). It also reduces the contribution from its top 10 tenants (29.4% to 26.3%) after merger.

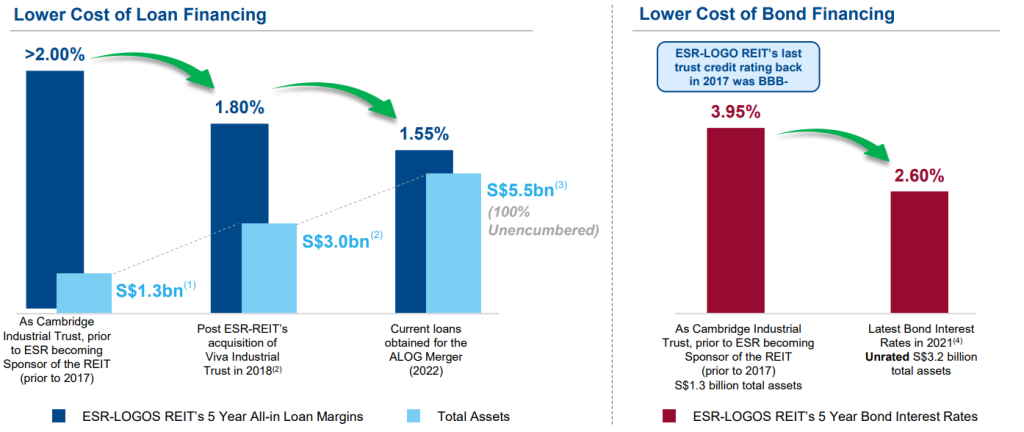

+Lower cost of loan and bond financing. This is due to the increase in unencumbered total assets and increase in diversity of portfolio.

Source: ESR-LOGOS REIT

Recent Issue:

ESR LOGOS REIT 5.50% Perpetual (SGD)

- Issue size: $150,000,000

- Coupon Payment: Semi – annually (9 June & 9 December with the first payment in 9 December 2022

- The issuer will have the option to recall the bonds at the end of year 5 (9th June 2027) but if the issuer does not redeem the bonds, it will be reset at prevailing SGD 5yr SORA-OIS plus the initial spread of 2.958%

- The proceeds from the issuance will be used to finance the merger between ESR-LOGOS REITS (previously known as ESR REIT) and ARA LOGOS Logistic Trust, refinancing existing borrowings of the Group, financing general working capital and capital expenditure requirements of the Group and any development and asset enhancement works initiated by ESR-REIT.

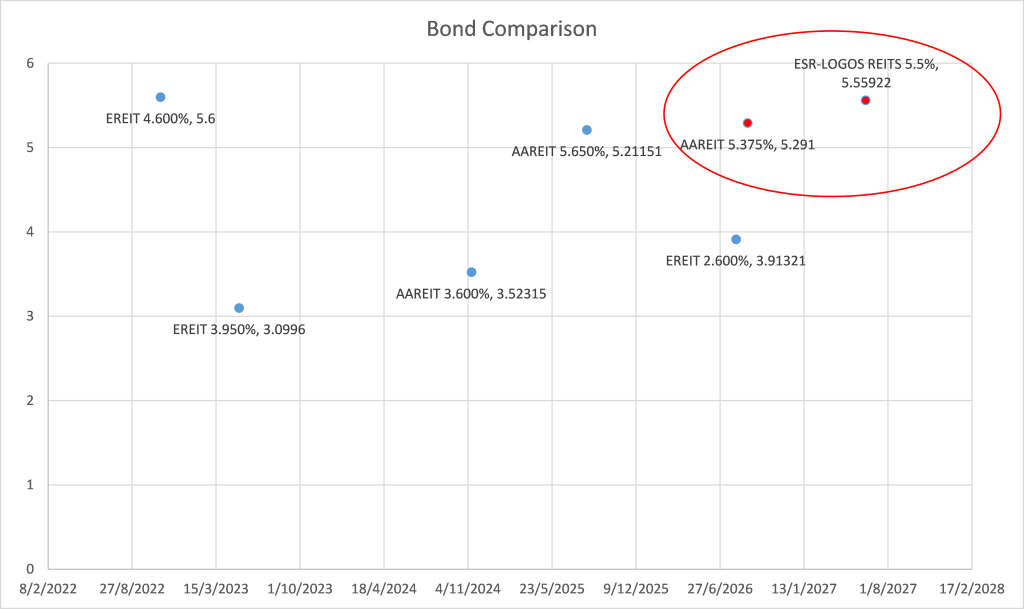

Bond Comparison

A comparable bond of against ESR-LOGOS REIT 5.5% perpetual (ERIT 5.5% Perp) would be Aims APAC REIT 5.375% perpetual (AAREIT 5.375% Perp). AAREIT 5.375% has a yield to worst of 5.291% and call date of 1 September 2026 (Base on the bid price of $100.315 as at 7 June 2022). While ERIT 5.5% has a yield to worst of 5.559% and a call date of 9 June 2027 (Base on the bid price of $99.738 as at 7 June 2022).

Source: Phillip Bond Desk

Overview

Through the merger, ESR-LOGOS REIT will have a greater exposure to logistics and high spec industrial sectors and with a larger and more diversified portfolio, ESR-LOGOS REIT will be able to leverage on its sponsor resources to accelerate its growth in terms of attracting and retaining value tenants. Additionally, the manager will also be able to improve on its management in property expenses due to higher economies of scale. Lastly, with the enlarged group, ESR-LOGOS REIT is seeking to seek a trust credit rating and with a favourable credit rating, it will be able to enjoy greater funding flexibility.