Executive Summary

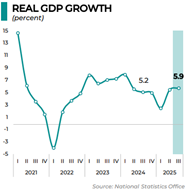

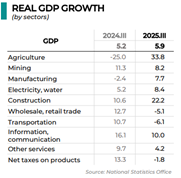

Mongolia’s growth profile strengthened into 2025, with real GDP expanding 6.8 % YoY in 2025, rebounding from 5.1% in 2024, primarily driven by a recovery in agriculture, which contributed 2.9 percentage points to growth, followed by mining (1.4pp) and manufacturing and construction (1.5pp). While agriculture was the largest contributor to growth in 2025, the mining sector remains structurally more important for Mongolia’s macroeconomic stability, as it generates the majority of export revenues and foreign-currency inflows.

Figure 1: Real GDP Growth

Growth Dynamics: Mining and Agriculture Drive Recovery

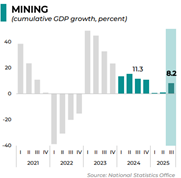

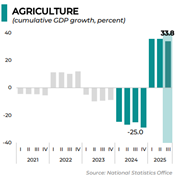

Mongolia’s economic growth has remained relatively strong in recent years. Real GDP expanded by 7.4% in 2023, before moderating to 5.1% in 2024, largely due to weaker agricultural output and a moderation in mining growth. Growth rebounded to 6.8% in 2025, supported by a recovery in livestock production and continued expansion in the mining sector.

Agriculture was a key contributor to the growth rebound in 2025, reflecting improved livestock output following weaker performance in the previous year. Mining continues to play a central role in Mongolia’s economy, generating approximately ₮4.7tn in value added, compared with ₮3.7tn for agriculture, and accounting for the majority of export revenues and foreign-currency inflows.

While services account for the largest share of domestic economic activity, they are largely domestically oriented and have a more limited impact on export earnings. As a result, Mongolia’s macroeconomic performance remains closely tied to developments in the commodity sector, leaving growth and fiscal revenues sensitive to fluctuations in mining output and global commodity demand.

Figure 2: Real GDP Growth (by sectors)

Figure 3: Mining Growth

Figure 4: Agriculture Growth

Public Debt Declining on Stronger Growth

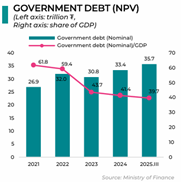

Mongolia’s public debt has declined materially over recent years, supported by stronger economic growth and improved mining revenues. Government debt stood at ₮35.7tn, equivalent to 39.7% of GDP in 3Q2025, continuing a downward trend from 41.4% in 2024, 43.7% in 2023, 59.4% in 2022, and 61.8% in 2021 (Figure 5). The improvement largely reflects stronger GDP growth and higher export earnings from the mining sector, particularly copper, which boosted fiscal revenues and strengthened external buffers.

Figure 5: Government Debt

External Accounts: Large trade surplus but highly concentrated export base

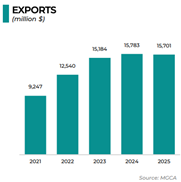

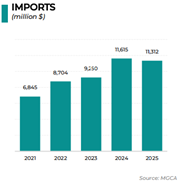

Mongolia recorded total foreign trade turnover of USD 27.0 bn in 3Q2025, with a trade surplus of USD 4.4 bn. Exports reached USD 15.7 bn (Figure 6), while imports declined slightly to USD 11.3 bn (Figure 8).

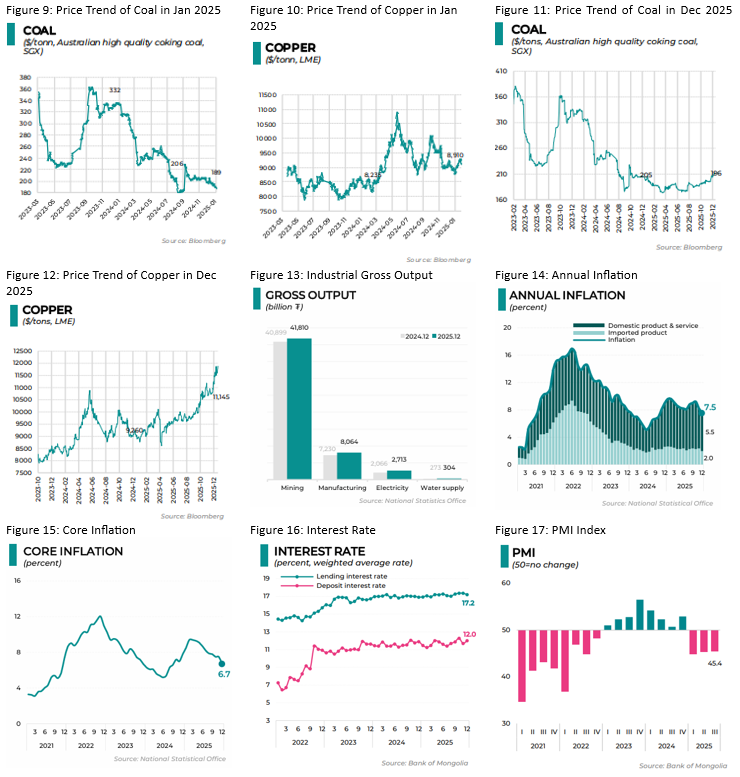

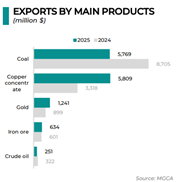

Export concentration remains structurally high, with mining products accounting for 93% of total exports; coal and copper concentrate make up the bulk. In 2025, coal export revenue declined sharply (–34% YoY), while copper concentrate exports surged (+75% YoY). In 2025, coal export revenue declined sharply (–34% YoY), while copper concentrate exports surged (+75% YoY) (Figure 7).

The divergence between coal and copper performance reflects global commodity price movements. In January 2025, coking coal averaged US$194/ton, down 41% YoY (Figure 9), while copper averaged US$8,981/ton (Figure 10), up 7% YoY. Coal prices later recovered to US$196/ton in December 2025 (Figure 11), a 15% YoY increase. Copper averaged US$13,056/ton, 45% increase YoY (Figure 12).

Figure 6: Exports

Figure 7: Exports by main products

Figure 8: Imports

External buffers: Strengthened reserve position

A notable macro improvement in 2025 was the rise in international reserves to US$7,005mn by year-end, up from US$4,884mn reported in January 2025. This reserve accumulation enhances Mongolia’s external liquidity buffer and supports exchange rate stability, providing greater resilience against commodity-related volatility.

Fiscal Position: Widening deficit amid revenue sensitivity

As of December 2025, the budget balance recorded a deficit of ₮1,232 bn, compared to -₮493bn in January 2025. Fiscal performance remains closely linked to mining-related revenue, particularly coal export receipts.

While trade performance remains supportive overall, commodity price volatility directly influences government revenue. This structural revenue sensitivity underscores the importance of commodity trends for Mongolia’s fiscal outlook.

Inflation and Monetary Conditions: Moderation but still elevated rates

Inflation moderated to 7.5% in December 2025, down from 9.6% in early 2025 (Figure 14). Producer prices showed mixed trends, with coal mining prices declining but metal ore mining prices rising. Despite easing inflation, interest rates remain elevated at 17.2% (Figure 16).

Business Sentiment and Private Sector Conditions

Despite stronger headline growth, business confidence indicators remain weak. The Purchasing Managers’ Index (PMI) stood at 45.4 in 3Q25 (Figure 17), signalling contractionary expectations. Construction and small and medium-sized enterprises reported particularly weak sentiment. This suggests that while mining and agriculture have rebounded, broader private-sector momentum remains cautious.

Bond Market Landscape

Ratings Overview (Moody’s, Fitch, S&P)

Mongolia’s sovereign credit profile has improved in recent years, with all three major rating agencies highlighting stronger macroeconomic fundamentals and improved fiscal management.

| Agency | Rating | Outlook |

| Moody’s | B1 | Stable | Fitch | B+ | Stable | S&P | BB- | Stable |

Key Credit Strength

Strong economic growth supported by mining

Mongolia’s economy is driven largely by the mining sector, especially copper and coal exports. Expansion of major projects such as the Oyu Tolgoi mine is expected to support economic growth over the medium term.

Declining government debt

Government debt has been trending lower as fiscal management improved and economic growth strengthened.

Stronger external buffers

Higher export revenues and improved foreign-exchange reserves have strengthened Mongolia’s ability to service foreign-currency debt and refinance external bonds.

Key Credit Constraints

Despite improvements, rating agencies highlight several structural risks.

Heavy dependence on commodity exports

Mongolia’s economy is highly sensitive to fluctuations in global commodity prices because mining exports dominate fiscal revenue and external balances.

Exposure to external financing conditions

The country relies on international capital markets to refinance sovereign bonds, making it vulnerable to global financial conditions.

Small and concentrated economy

As a frontier market, Mongolia’s economic structure remains relatively narrow compared with larger emerging markets.

Credit Outlook

Looking ahead, Mongolia’s sovereign credit profile is likely to gradually strengthen, supported primarily by the expansion of the mining sector. In particular, copper production at the Oyu Tolgoi LLC is currently ramping up as underground operations expand across multiple panels. Output reached roughly 345,000 tonnes of copper concentrate in 2025, and project guidance indicates production could rise to around 500,000 tonnes annually on average between 2028 and 2036. This increase in copper output is expected to significantly boost Mongolia’s export revenues and foreign-currency inflows, strengthening external balances and supporting the government’s capacity to service external debt. Nevertheless, Mongolia’s credit outlook remains sensitive to commodity price cycles, particularly fluctuations in copper and coal prices, which continue to influence fiscal revenues and external accounts.

Frontier Sovereign USD Bond Yield Comparison

| Region | Avg Coupon (%) | Credit Rating |

| Central Asia | ||

| Mongolia | 6.03 | BB-/B1/B+ |

| Kazakhstan | 5.03 | BBB/BBB-/Baa1 |

| Uzbekistan | 6.08 | BB/Ba3 |

| Kyrgyzstan | 7.75 | B3/B+/B |

| Middle East | ||

| Oman | 5.74 | BBB- |

Source: Bloomberg

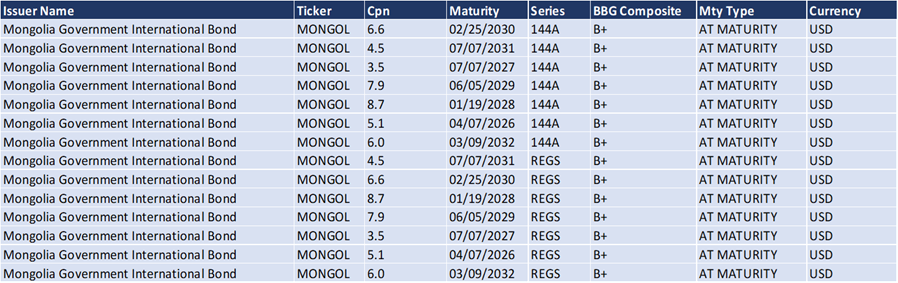

List of Mongolia Government Bonds