SINGAPORE |CREDIT PROFILE

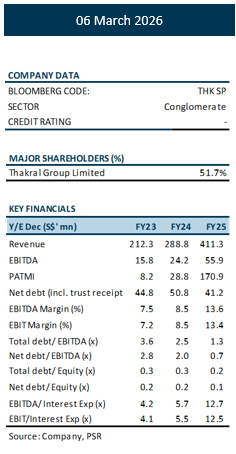

- PATMI rose to S$171mn (+493% YoY) in FY2025, largely driven by a S$128.5mn fair value gain following the IPO of two investments. Excluding this, EBITDA increased to S$56mn (+122% YoY), driven by stronger performance in the Lifestyle segment where core profit +36% YoY to S$14.8mn. Management guides ~25% growth in the Lifestyle segment in FY2026, supported by retail expansion across India and South Asia. The Lifestyle segment is the distribution of L’Oreal related beauty and fragrances in Greater China, DJI products across South Asia and Nespresso in India.

- Thakral listed two major investments in 2025 that are worth S$338.4mn (25Feb26). These entities are Australian Stock Exchange listed GemLife (S$304.8mn) and London Stock Exchange listed The Beauty Tech Group (S$33.6mn). We view these assets as a pool of liquidity that can be monetised to raise liquidity if required.

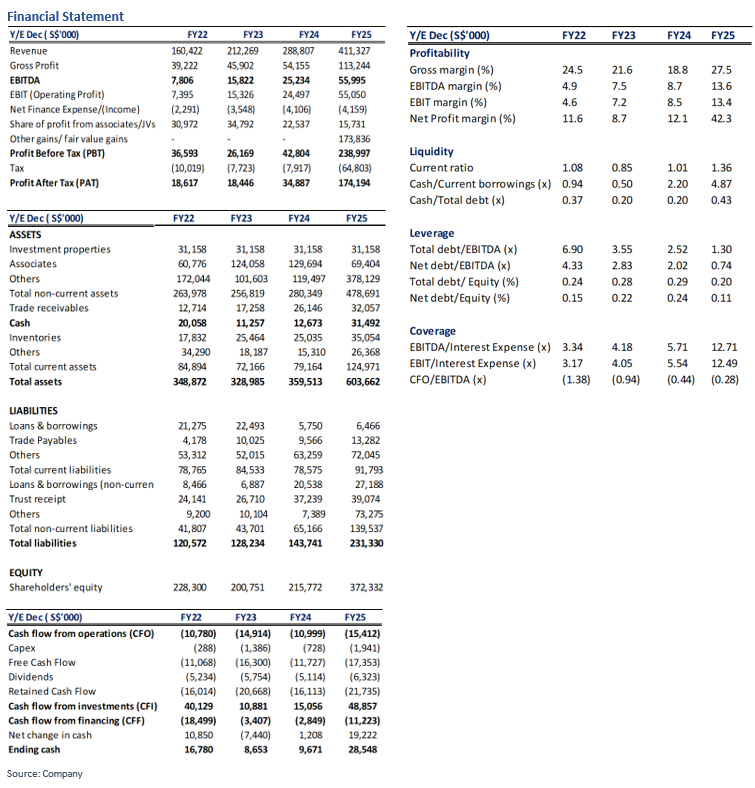

- EBITDA/interest exp improved to 12.7x (FY24: 5.7x), supported by stronger EBITDA. The leverage also improved with net debt/EBITDA declining to 0.74x (FY24: 2.02x) and net debt/equity to 0.11x (FY24: 0.24x). The improved coverage and lower leverage indicate a stronger capacity to service debt and accommodate additional funding if needed, particularly for its 21-acre mixed used development in Delhi.

Credit Performance Highlights

- PATMI rose to S$171mn (+493% YoY) in FY2025 (FY2024: S$29mn), mainly driven by a S$128.5mn fair value gain following the IPO of two investment. Excluding this one-off gain, underlying operating performance also strengthened, with EBITDA increasing to S$56mn (+122% YoY). The improvement was primarily driven by continued expansion of the Lifestyle segment, where the core operating profit of the segment increased 36% YoY to S$14.8mn. The segment generates earnings primarily from distribution of DJI products across South Asia, Nespresso distribution in India, and premium beauty and fragrance retail in Greater China, which continued to benefit from strong consumer demand.

- Thakral holds S$338.4mn of listed investments as at 26 Feb 2026, primarily comprising 16.8% stake in GemLife (S$304.8mn) and 6.04% stake in The Beauty Tech Group (S$33.6mn). These listed holdings could potentially be monetised to raise liquidity if required.

- The Lifestyle segment retails and distributes established global brands across beauty, fragrance and technology. Key brands include Maison Margiela, Atelier Cologne, Viktor & Rolf, Mugler, Ralph Lauren Fragrances, Yue Sai and Miu Miu. In South Asia, the Group distributes DJI products and Nespresso. The Group operates 65+ retail stores and counters in Greater China, supporting product demand and contributing to segment earnings.

- Looking ahead, management guides 25% Lifestyle segment growth in FY2026, supported by continued expansion in India and South Asia. Key drivers include (i) the planned 20–30 DJI retail store openings, (ii) expansion of Nespresso’s retail presence in India, and (iii) participation in India’s growing drone ecosystem through Bharat Skytech, which will commence in-house component manufacturing from May 2026. These initiatives should support continued earnings growth and enhance the scale of the Lifestyle segment. In our view, stronger earnings generation should support the Group’s debt-servicing capacity and interest coverage over time.

- Thakral is increasing its stake to 95.28% in a 21-acre mixed-use development site in Gurugram for S$93.9mn, with approximately 2.5mn sq ft of development potential across residential and healthcare components. The site is located within Delhi’s National Capital Region (NCR), one of India’s most active property markets. Gurugram has seen strong demand for high-end residential housing, with S$3.36bn of transactions for homes priced above S$1.4mn in 2025. Management expects the project to begin contributing cash flows in next 5–7 years. The healthcare component is expected to generate recurring rental income, while the residential component will provide revenue from the sale of housing units, diversifying the Group’s earnings base and supporting longer-term cash-flow visibility once stabilised.

- Credit metrics improved alongside stronger earnings. EBITDA/interest increased to 12.7x (FY24: 5.7x), indicating stronger capacity to service interest obligations. At the same time, leverage improved, with net debt/EBITDA declining to 0.74x (FY24: 2.02x) and net debt/equity to 0.11x (FY24: 0.24x), given EBITDA expansion and higher cash balances. We believe these metrics provides the group with headroom to accommodate additional funding needs and absorb moderate earnings volatility without placing immediate pressure on credit metrics.

Credit View:

We are positive on Thakral’s credit profile, supported by stronger earnings generation and lower leverage. EBITDA expansion, driven primarily by the Lifestyle segment, has materially strengthened credit metrics, with EBITDA/interest improving to 12.7x and net debt/EBITDA declining to 0.74x, indicating headroom for debt servicing. Looking ahead, earnings should remain supported by continued expansion of the Lifestyle platform, particularly through retail growth in India and South Asia and increasing participation in India’s drone ecosystem. In addition, the Group’s S$338.4mn listed investment asset provides meaningful asset backing and liquidity optionality, offering strong downside protection for creditors.

Company Background

Thakral Corporation Ltd has been listed on the SGX Mainboard since December 1995. The Group’s core business comprises a growing investment portfolio in Australia, Japan, and Singapore. Investments in Australia include the development and management of over-50s lifestyle resorts under the GemLife brand. The Japanese investment portfolio consists of landmark commercial buildings in Osaka, the country’s second-largest city. The Group currently manages 65 retail stores or counters – including 26 stores of L’Oreal-owned skin care brand Yue Sai – across its portfolio of brands in Greater China (including Mainland China, Hong Kong and Macau) and India. It serves customers directly through retail flagship stores, multi-brand speciality retailers, and e-commerce platforms. Furthermore, the Group makes strategic investments in new-economy ventures that complement its existing business relationships and networks, including serving as a cornerstone investor or participating in early-stage funding. These investments aim to harness potential synergies and explore new business opportunities.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd (“Phillip Securities Research”), which is a holder of a financial adviser’s license under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSES

Where the report contains research analyses or reports from a foreign research house, please note:

- recipients of the analyses or reports are to contact Phillip Securities Research (and not the relevant foreign research house) in Singapore at 250 North Bridge Road, #06-00 Raffles City Tower, Singapore 179101, telephone number +65 6533 6001, in respect of any matters arising from, or in connection with, the analyses or reports; and

- to the extent that the analyses or reports are delivered to and intended to be received by any person in Singapore who is not an accredited investor, expert investor or institutional investor, Phillip Securities Research accepts legal responsibility for the contents of the analyses or reports.