Stock Market Today

| 9 April 2026

Recent Podcasts:

Wee Hur Holdings Ltd – Construction and worker dorm anchor growth

Advanced Micro Devices Inc. – Clear Instinct GPU roadmap, strong CPU demand

Netflix Inc. – Content, ads, and scale drive the next leg of growth

Singapore market advanced on Wednesday as US President Donald Trump announced a two-week ceasefire with Iran, bringing momentary pause to the conflict. The local benchmark rose 1.2% to 5,018.19 points at market open, buoyed by the three Singapore banks which all traded higher. DBS was up 0.1%, UOB rose 1.5% and OCBC increased 2.2%.

US stocks closed sharply higher on Wednesday after a last-minute, two-week ceasefire agreement between the United States and Iran lifted investor sentiment. The Dow Jones Industrial Average rose 1,326.33 points, or 2.85%, to 47,910.79, and the S&P 500 gained 165.98 points, or 2.51%, to 6,782.83.

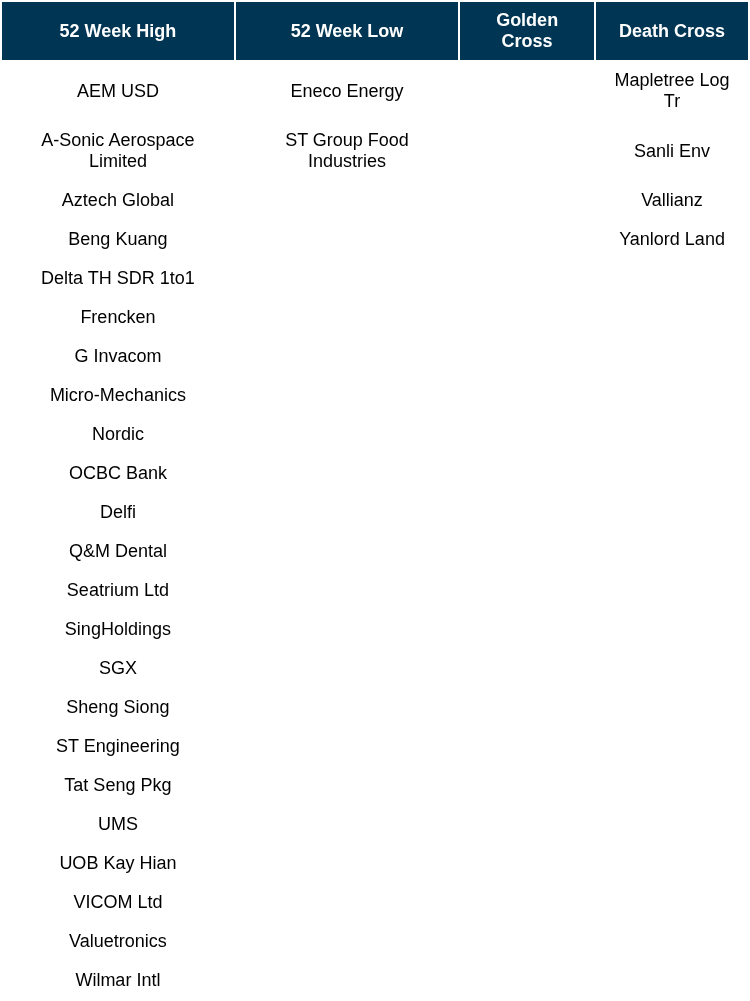

Singapore Technical Highlights

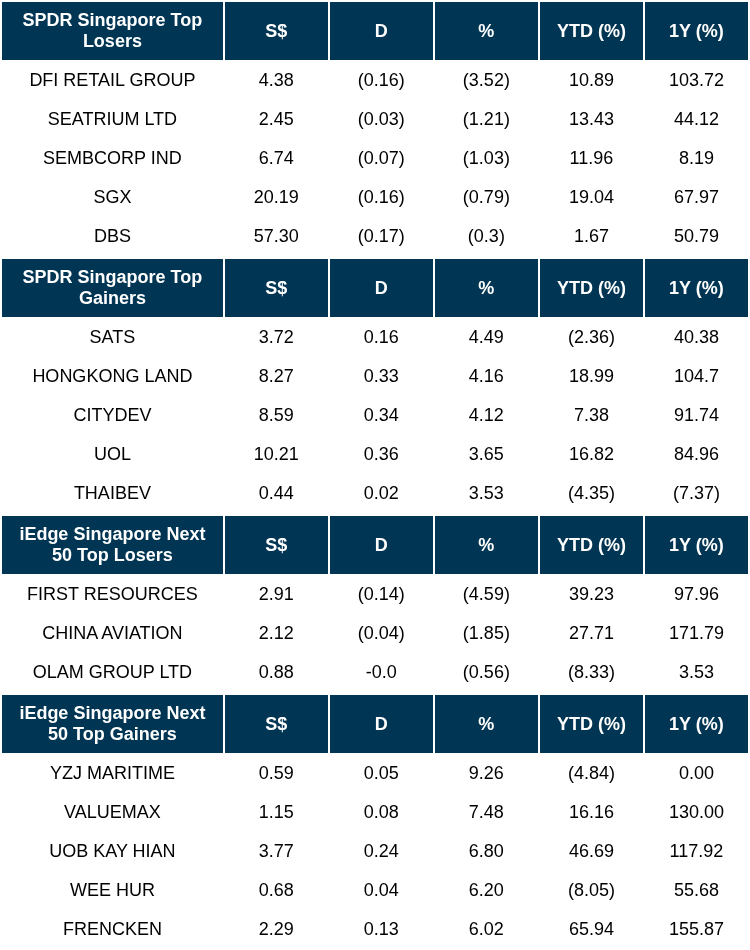

TOP 5 GAINERS & LOSERS

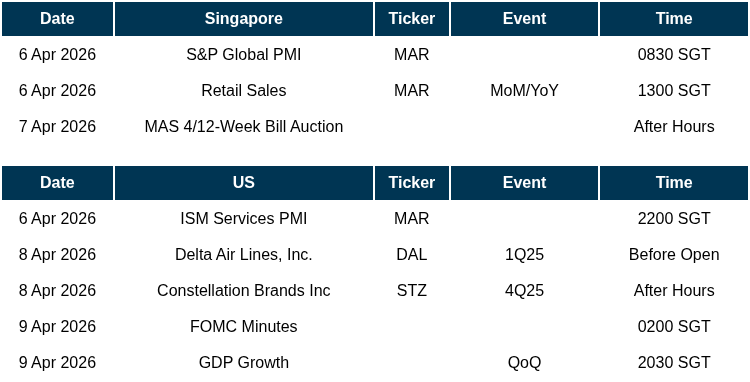

EVENTS OF THE WEEK

SG

iX Biopharma announced that it has allotted and issued 10 million new ordinary shares at a price of six cents per warrant share as part of its exercise of warrants. Following the exercise, the number of issued shares in iX Biopharma increased from 1,038,324,529 shares to 1,048,324,529 shares.

Thakral has raised $4.26 million through the sale of 2,367,500 treasury shares at a price of $1.80, which represents a 1.89% shareholding in the company. The proceeds raised will be used for working capital purposes, which includes advancing its growth initiatives in the lifestyle and investment segments.

Innotek plans to raise up to $16 million by placing out up to 24.6 million new shares at 65.06 cents each. The placement price represents a discount of approximately 9.5% to the volume weighted average price of 71.89 cents, based on the last full market day of April 2.

Seatrium has launched a S$3 billion multicurrency debt issuance programme, the offshore and marine group said on Wednesday (Apr 8). The net proceeds will be used for refinancing existing borrowings, funding potential acquisitions and investments, working capital and capital expenditure requirements, as well as providing internal loans within the group.

Lim Sim Seng has been appointed as deputy chairman and non-executive independent director of the board of SIA Engineering, effective Wednesday. He has 42 years of banking experience in Asia, North America and the Middle East.

Grab Holdings unveiled 13 artificial intelligence (AI)-powered features at its annual product showcase GrabX 2026 on April 8, as the Southeast Asian superapp looks to deepen its role in users’ daily lives and expand its services across travel, payments and merchant tools.

US

The US and Iran agreed to a two-week ceasefire and Tehran pledged to reopen the Strait of Hormuz, a last-ditch deal that saw President Donald Trump back off from threats to escalate the war. US will be talking tariff and sanctions relief with Iran, and threatens 50% tariffs on countries supplying weapons to Iran.

Meta Platforms on Wednesday unveiled Muse Spark, the first artificial intelligence model from a costly team it assembled last year to catch up with rivals in the AI race. U.S. tech giants are under pressure to prove their massive AI outlays will pay off.

Anthropic on Monday had disclosed that their annualized run-rate revenue surpassed $30 billion, up from $9 billion at the end of 2025 and $19 billion one month ago. Over 1,000 businesses now spending more than $1mn annually on Anthropic’s AI models, roughly double the number seen just weeks earlier.

Pacific Investment Management Company (Pimco) is in talks with Bank of America to help provide roughly US$14 billion of debt financing to build a massive Oracle data centre in Michigan.

AppLovin Corporation (APP) announced succession plans for key executive roles and appointed Craig Billings as independent chairperson of its board of directors.

Gold rose after US President Donald Trump and Iran agreed to a two-week ceasefire to finalise talks on ending the war that’s upended global markets. Bullion climbed as much as 3.2% to above US$4,850 an ounce, adding to a 1.2% gain in the previous session.

Oil slid the most in almost six years and stocks surged after the US and Iran agreed to a two-week ceasefire. West Texas Intermediate tumbled as much as 19% after US President Donald Trump agreed to suspend bombing on Iran in a move that will help resume oil flows through the Strait of Hormuz.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Market Journal articles powered by PhillipGPT

Wee Hur Holdings Upgraded to Buy on Strong Performance and Growth Prospects

TeleChoice International Ltd Maintains Growth Trajectory with Strong FY25 Performance

Singapore Banking Sector Faces Mixed Outlook as Rates Stabilise

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Strategy & Stock Picks (Investment Symposium 2026) – SG Market

Date & Time: 11 April 26 | 2.30PM-6PM

Register: poems-20260411-142749

Corporate Insights by The Assembly Place

Date & Time: 22 April 26 | 12PM-1PM

Register: poems-20260422-143868

Corporate Insights by Nordic Group Ltd [NEW]

Date & Time: 23 April 26 | 12PM-1PM

Register: poems-20260423-144485

Corporate Insights by Southern Alliance Mining Ltd

Date & Time: 30 April 26 | 12PM-1PM

Register: poems-20260430-143892

POEMS Podcast:

Research Videos

Weekly Market Outlook: YZJ Maritime, First REIT, Tech Analysis, SG Weekly & more!

Date: 6 April 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials