News & Research

Hear from the Experts

Market Overview

*15mins delayed

| 10 April 2026

Recent Podcasts:

Wee Hur Holdings Ltd – Construction and worker dorm anchor growth

Advanced Micro Devices Inc. – Clear Instinct GPU roadmap, strong CPU demand

Netflix Inc. – Content, ads, and scale drive the next leg of growth

Singapore stocks ended lower on Thursday (Apr 9), tracking declines across regional bourses as investors remained cautious, despite headlines of a temporary ceasefire in the Middle East. The benchmark fell 0.4 per cent, or 18.97 points, to close at 4,977.08. Wilmar and City Developments Limited (CDL) were the joint worst performers.

US stocks advanced on Thursday, as ongoing negotiations toward a peaceful resolution to the six-week Middle East conflict helped ease worries over the fragile US-Iran truce. The Dow Jones Industrial Average rose 275.88 points, or 0.58 per cent, to 48,185.80, and the S&P 500 gained 41.85 points, or 0.62 per cent, to 6,824.66.

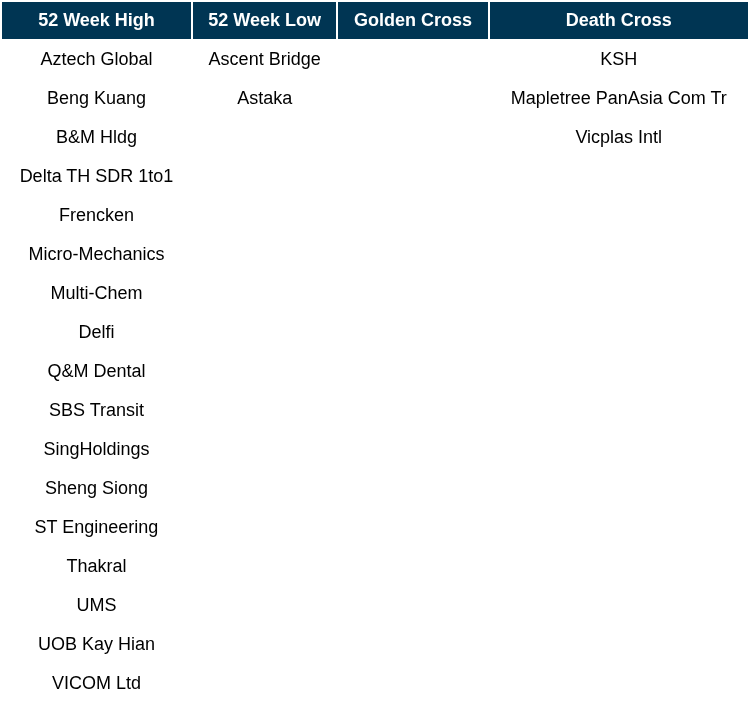

Singapore Technical Highlights

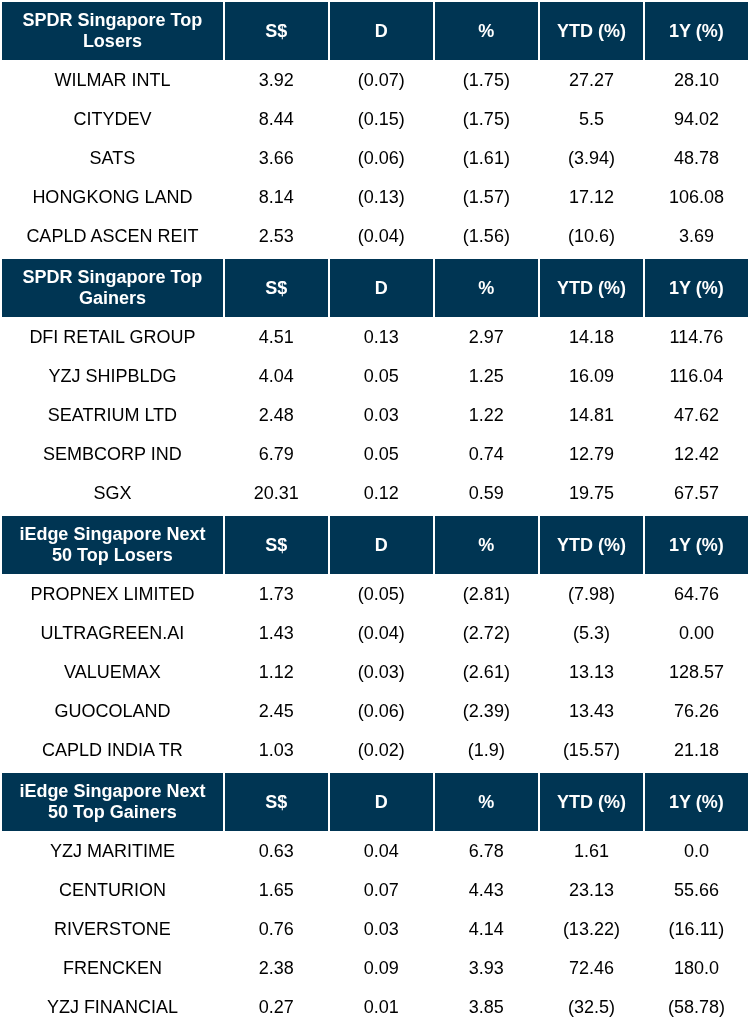

TOP 5 GAINERS & LOSERS

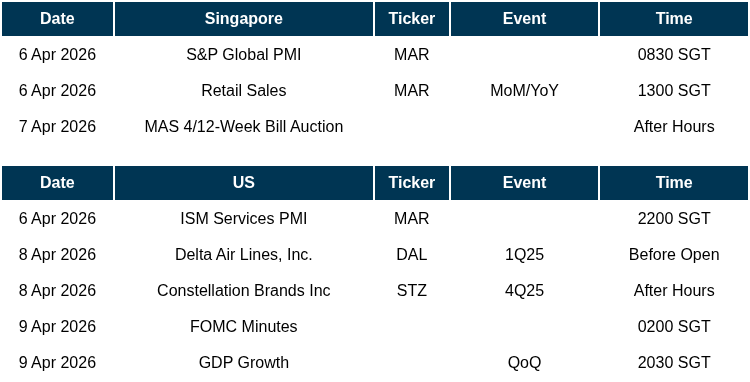

EVENTS OF THE WEEK

SG

SGX’s securities market turnover for March jumped 78% y-o-y $52.8 billion, with securities daily average value (SDAV) up 62% y-o-y at $2.4 billion, or the highest since October 2007, thanks to both institutional and retail participation.

City Developments Ltd (CDL) has launched a S$2 billion multicurrency debt issuance programme.

The net proceeds will be used to finance general working capital requirements and corporate funding of CDL and its subsidiaries, as well as to refinance existing borrowings.

Cloud- and carrier-neutral data centre platform Digital Realty is targeting nearly $7 billion in total investment in Singapore to support the city-state as a hub for artificial intelligence (AI) inference in Asia Pacific.

US

The US wants specific commitments from European allies on their pledge to help secure the Strait of Hormuz after the fighting in Iran stops, requesting that the countries present concrete plans to ensure navigation through the waterway within days, according to a senior Nato official.

Walt Disney is planning to cut as many as 1,000 positions in the coming weeks, many of which will be made in the company’s marketing department. The planned layoffs could affect less than 1 per cent of its total employees. Disney employed about 231,000 people as of the end of fiscal year 2025.

OpenAI said it is pausing its Stargate artificial intelligence (AI) infrastructure project in the UK, as it reins in ambitious spending plans ahead of a highly anticipated public listing.

Oil rebounded on Thursday after its biggest one-day drop since April 2020, as the Strait of Hormuz remained largely blocked and Israeli attacks on Lebanon threatened to derail the fragile ceasefire in the Middle East. Brent rose towards US$97 ($123.64) a barrel after slumping 13% on Wednesday.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

iX Biopharma Ltd – Year of the Unicorn

Recommendation: BUY (Re-initiation); TP S$1.00, Last close: S$0.20; Analyst Paul Chew

- iX Biopharma has secured US$41mn funding from the US Department of Defense (DoD) to support the Phase 3 clinical development of its pain drug Wafermine. It validates iX Biopharma’s WaferiX technology platform and allows entry into the US$5-6bn acute pain drug market in the US.

- Prior to full FDA approval, iX Biopharma will seek approval for Wafermine to be supplied to the DoD under an Emergency Use Authorisation (EUA) for immediate battlefield deployment and operational military medical use. We expect initial orders of S$3mn in FY27e. The larger opportunity is Wafermine adoption into standard field kits and sales into the non-military commercial market following full US FDA approval.

- We re-initiate coverage on iX Biopharma with a BUY recommendation and a SOTP-derived target price of S$1.00.There are three pathways to monetise Wafermine: full commercialisation upon FDA approval (1Q29), out-licensing, or an outright sale of the drug. Until completion of Phase 3 trials, iX Bio will be enjoying three new sources of revenue through Wafermine EUA sales, DoD grant funding, and compound pharmacy in the US. We assign a 40% discount to the underlying net present value of Wafermine and value the compound pharmacy at 20x PE. We also discounted the remaining 30+ drugs, which are under various stages of development.

Nanofilm Technologies International Limited – Poised for a comeback

Analyst: Yik Ban Chong (Ben)

- We visited Nanofilm’s facilities in Shanghai, China, from 24-27 Mar 2026. We saw Nanofilm’s coating solutions, notably Filtered Cathodic Vacuum Arc (FCVA), FCVA-hybrid, and tetrahedral amorphous carbon (ta-C). Nanofilm’s coating solutions can be applied to computers, communications, and consumer electronics (3C), automotive, precision engineering, and semiconductors. Applications include coatings on watch enclosures to increase durability, and to smartphones’ internal electrical components to prevent short circuits.

- 2H25 revenue increased 13% YoY to S$137.4mn, driven by new watch programs from its existing largest customer (“customer Z”). Customer Z is one of the most popular smartphone brands globally, and makes up 60% of Nanofilm’s revenue (prev. 78% during Mainboard listing). Growth is also driven by new contributions from EuropCoating, a European company which coats semiconductor wafer carriers, and higher demand for mould coaters for optical lenses.

- Nanofilm is trading at 1.2x P/B, a 61% discount to peers’ average P/B of 3.1x. Nanofilm targets double-digit growth in 2026e for the semiconductor, automotive and industrial segments. Nanofilm’s FCVA and physical vapour deposition (PVD) solutions are used in electrostatic discharge protection and precision tooling for semiconductor packaging. Nanofilm’s FY25 free cash flow rebounded to a positive S$1.8mn, following two consecutive years of negative free cash flow, driven by a 129% YoY spike in FY25 operating cash flow to S$48.6mn.

Market Journal articles powered by PhillipGPT

Wee Hur Holdings Upgraded to Buy on Strong Performance and Growth Prospects

TeleChoice International Ltd Maintains Growth Trajectory with Strong FY25 Performance

Singapore Banking Sector Faces Mixed Outlook as Rates Stabilise

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Strategy & Stock Picks (Investment Symposium 2026) – SG Market

Date & Time: 11 April 26 | 2.30PM-6PM

Register: poems-20260411-142749

Corporate Insights by The Assembly Place

Date & Time: 22 April 26 | 12PM-1PM

Register: poems-20260422-143868

Corporate Insights by Nordic Group Ltd [NEW]

Date & Time: 23 April 26 | 12PM-1PM

Register: poems-20260423-144485

Corporate Insights by Southern Alliance Mining Ltd

Date & Time: 30 April 26 | 12PM-1PM

Register: poems-20260430-143892

POEMS Podcast:

Research Videos

Weekly Market Outlook: YZJ Maritime, First REIT, Tech Analysis, SG Weekly & more!

Date: 6 April 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.