Thai Beverage PLC - Beer leading the recovery

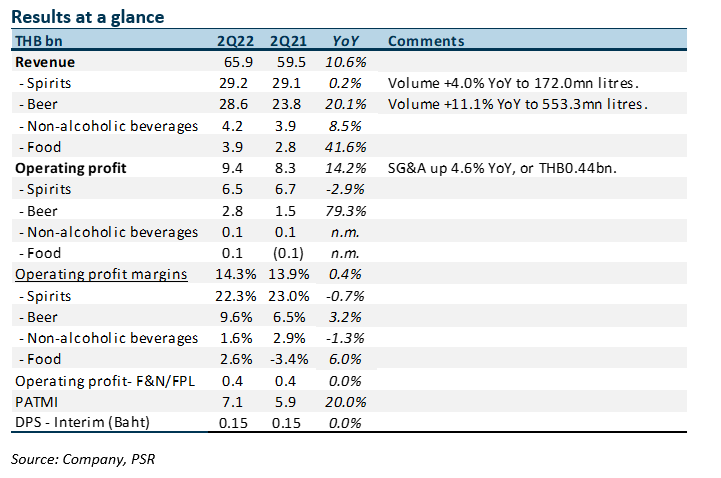

17 May 2022- 1H22 revenue and PATMI beat our expectations, at 55%/62% of our FY22e forecasts. 2Q22 PATMI rose 20% YoY to THB7.1bn. Interim dividend was unchanged at THB0.15.

- Driving earnings growth was a 3-fold recovery in beer and associates PATMI. Spirits earnings were down 3% YoY to THB5.4bn due to a higher mix of white spirits. Spirits accounted for 75% of group PATMI.

- We maintain our ACCUMULATE recommendation. Our FY22e earnings is raised 5% to THB27.6bn. The target price is raised from S$0.765 to S$0.80. Valuation is based on 18x earnings, its 5-year average. FY22e will be a recovery from pandemic lockdowns last year. The pace of the recovery will depend on entertainment outlets reopening in Thailand.

The Positives

+ Beer bounces back. Beer earnings surged as volumes jumped 11% YoY to 553mn litres. Volumes remain 24% below pre-pandemic levels in 2Q19. Another driver of revenue growth was the low (Thailand) to high (Vietnam) single-digit price increases on beer during the quarter. Sabeco raised prices in December 2021 and April 2022.

+ Margins stable despite cost pressure. THBEV continues to keep a lid on operating expenses. 2Q22 administration expenses declined 2.6% YoY to THB3.8bn or 5.8% revenue (2Q21: 6.5%). This is below the pre-pandemic run-rate of around 11%. Despite the raw material cost pressures, gross margins were stable at around 29.7%. The price increase and higher volumes supported margins.

The Negative

– Weaker spirits revenue. 2Q22 spirit volumes expanded for the second consecutive quarter, rising 4% YoY to 172mn litres (1Q22: +8.6% YoY). Volume this quarter jumped from forward loading by distributors ahead of a price increase of white spirits in February. Consequently, revenue was flat YoY due to a higher mix of white spirit sales.

Outlook

The re-opening of entertainment outlets in Thailand will determine the pace of recovery for THBEV. A complete re-opening will boost beer and brown spirits consumption for the company. Sabeco beer volumes will rebound from the lockdowns a year ago.

We expect spirits earnings to grow modestly in 2H22, supported by price increases in November 2021 and February 2022 of 4-6%. Margins could creep up from lower molasses cost. The sugar cane crop in Thailand is up around 40% from a year ago, helping to lower prices.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

JPMorgan Chase & Co - NII continues to rise, guidance maintained

JPMorgan Chase & Co - NII continues to rise, guidance maintained Trade of the Day - NVIDIA Corporation (NASDAQ: NVDA)

Trade of the Day - NVIDIA Corporation (NASDAQ: NVDA) Trade of the Day - Applied Materials, Inc. (NASDAQ: AMAT)

Trade of the Day - Applied Materials, Inc. (NASDAQ: AMAT) CapitaLand Ascott Trust - Occupancy to improve with ADRs stabilising

CapitaLand Ascott Trust - Occupancy to improve with ADRs stabilising