Company Overview

17LIVE Group Limited operates as a live-streaming platform company, focusing on interactive entertainment services that connect content creators with audiences through real-time streaming technology. The company generates revenue primarily through its live-streaming platform whilst exploring diversification opportunities to strengthen its market position.

Financial Performance and Earnings Turnaround

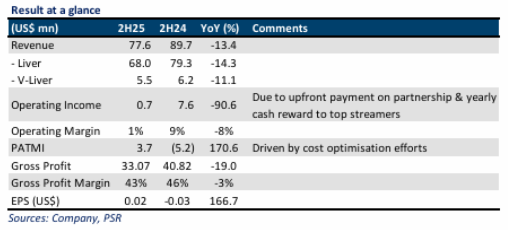

17LIVE demonstrated resilience in its latest results, with 2H25 earnings showing a significant turnaround despite revenue challenges. Revenue declined 13.4% year-on-year to US$77.6 million, primarily attributed to foreign exchange headwinds and flat growth in the broader live-streaming market. However, the company achieved a notable profit improvement, with PATMI turning positive to US$3.7 million from a loss of US$5.2 million in 2H24.

For the full financial year, FY25 revenue reached 91% of forecasts, though PATMI missed expectations with a net loss of US$0.9 million compared to the anticipated US$5.48 million profit forecast.

Key Positives Driving Recovery

The profit improvement reflects 17LIVE’s successful cost optimisation initiatives implemented since 2024. These efforts targeted IT infrastructure, marketing expenses, and organisational efficiency, resulting in operating expenses declining by approximately 2.5% year-on-year to US$32.4 million from US$33.2 million.

17LIVE has enhanced shareholder value through its dividend policy, declaring a final dividend of 0.5 Singapore cents per share for 2H25, bringing the total FY2025 dividend to 2.0 Singapore cents per share. This distribution is supported by the company’s robust cash position of US$73.4 million. Operating cash flow turned positive in FY25 to US$4.35 million, compared to negative US$16.7 million in FY24.

The company continues executing its share buyback programme launched in 2024, with authority to repurchase up to 10% of issued share capital. As of 2H25, 9 million shares worth US$6.8 million have been repurchased, representing approximately 53% of the authorised limit.

Strategic Outlook and Research Recommendation

17LIVE plans to monetise existing assets and diversify revenue streams through initiatives including V-Liver IP, sports collaborations, and short-form drama content, expected to gradually drive user engagement and revenue growth.

Phillip Securities Research maintains its BUY rating whilst reducing the target price from S$1.45 to S$1.18, reflecting softer growth assumptions for the live-streaming market and slower monetisation trends. At current levels, 17LIVE trades at an FY26e P/E of 33x.

Frequently Asked Questions

Q: What was 17LIVE’s revenue performance in 2H25?

A: Revenue declined 13.4% year-on-year to US$77.6 million, mainly due to foreign exchange headwinds and flat growth in the live-streaming market.

Q: How did the company’s profitability change in 2H25?

A: PATMI turned positive to US$3.7 million from a loss of US$5.2 million in 2H24, driven by ongoing cost-optimisation efforts.

Q: What dividend is 17LIVE paying for FY2025?

A: The company declared a total dividend of 2.0 Singapore cents per share for FY2025, including a final dividend of 0.5 Singapore cents per share for 2H25.

Q: What is Phillip Securities Research’s current recommendation?

A: They maintain a BUY rating but reduced the target price from S$1.45 to S$1.18, with 17LIVE trading at an FY26e P/E of 33x.

Q: How is 17LIVE planning to diversify its revenue streams?

A: The company plans to monetise existing assets through initiatives including V-Liver IP, sports collaborations, and short-form drama content.

Q: What is the company’s cash position?

A: 17LIVE maintains a strong cash position of US$73.4 million, with operating cash flow turning positive to US$4.35 million in FY25.

Q: How much has the company spent on share buybacks?

A: As of 2H25, 9 million shares worth US$6.8 million have been repurchased, representing approximately 53% of the authorised limit under the current mandate.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.