Company Overview

CapitaLand Investment Limited (CLI) is a leading real estate investment manager operating across multiple asset classes and geographical markets. The company focuses on an asset-light strategy, generating recurring fee income through fund management services across listed and private funds, alongside lodging and commercial management.

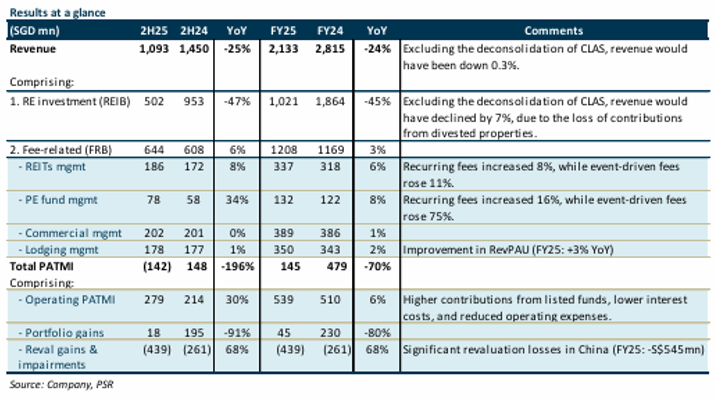

Mixed Financial Performance Amid China Headwinds

CLI reported FY25 PATMI of S$145 million, representing a steep 70% year-on-year decline that fell significantly short of expectations, forming only 22% of our FY25 forecast. This disappointing headline figure was primarily driven by substantial S$439 million revaluation losses, predominantly from Chinese assets. However, when excluding these revaluation impacts, operating PATMI of S$539 million performed more respectably at 98% of estimates, with a 6% year-on-year increase supported by higher contributions from listed funds, reduced finance costs, and lower operating expenses.

The company’s Funds Under Management expanded 7% year-on-year to S$125 billion. Management believes organic growth can drive FUM to approximately S$160 billion, though acquisitions will be necessary to achieve the ambitious S$200 billion target by 2028.

Strong Positives in Fee Income Growth

CLI demonstrated resilience in its core fee-generating businesses, with fee income delivering steady 6% year-on-year growth. All fee-related business segments recorded revenue increases, with listed funds management up 8% and private funds management surging 24%, including CLI’s 40% share of SCCP revenue. The lodging management division achieved a record year, signing 19,000 units across 102 properties, which positions the company well for long-term growth as these units become operational. CLI now manages 176,000 keys, with over 100,000 currently operational.

Significant Valuation Pressures

The major negative factor was the sharp decline in asset valuations, with S$436 million in aggregate fair value losses recorded. China bore the brunt of these losses at S$545 million, particularly affecting office and business park assets, as challenging operating conditions persist with negative rental reversions across all sectors. The UK and Europe also contributed S$62 million in losses, though these were partially offset by gains in Southeast Asia (S$59 million) and India (S$98 million).

Divestment activity slowed considerably, falling from S$5.5 billion in FY24 to S$3.1 billion in FY25, largely due to the higher proportion of remaining assets located in China. Approximately S$1 billion was divested from China at 10-20% discounts to book value, leaving roughly S$3 billion of Chinese assets still on the books.

Investment Outlook

Phillip Securities Research maintains a BUY recommendation with a higher sum-of-the-parts target price of S$3.69, up from the previous S$3.65. The firm expects balance sheet divestments to accelerate in FY26, with potential for a second C-REIT listing. The board has proposed a final dividend of 12 cents, implying a 3.8% yield.

Frequently Asked Questions

Q: What caused CapitaLand Investment’s significant earnings decline in FY25?

A: The 70% year-on-year PATMI decline was primarily due to S$439 million in revaluation losses, mainly from China assets. Excluding these losses, operating PATMI actually grew 6% year-on-year.

Q: How did CLI’s fee income business perform?

A: Fee income showed resilience with 6% year-on-year growth. Listed funds management grew 8%, private funds management surged 24%, and lodging management signed a record 19,000 units across 102 properties.

Q: What is CLI’s Funds Under Management target?

A: FUM currently stands at S$125 billion, up 7% year-on-year. CLI believes it can grow organically to approximately S$160 billion but acknowledges acquisitions will be necessary to reach the S$200 billion target by 2028.

Q: Which geographical markets are causing valuation concerns?

A: China recorded the largest losses at S$545 million, particularly in office and business parks. The UK and Europe also saw S$62 million in losses, though Southeast Asia and India posted gains of S$59 million and S$98 million respectively.

Q: How much Chinese assets does CLI still hold?

A: After divesting approximately S$1 billion from China at 10-20% discounts to book value, CLI still has roughly S$3 billion of Chinese assets remaining on its books.

Q: What is Phillip Securities Research’s recommendation?

A: Phillip Securities Research maintains a BUY recommendation with a target price of S$3.69, citing CLI’s robust recurring fee income and asset-light strategy that supports resilience amid macro uncertainty.

Q: What dividend has been proposed for FY25?

A: CLI’s board has proposed a final dividend of 12 cents, which implies a dividend yield of 3.8%.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.