Company Overview

Centurion Corporation Ltd operates purpose-built worker accommodation (PBWA) and purpose-built student accommodation (PBSA) across Singapore, Malaysia, the UK, and Australia. The company has recently spun off its real estate investment trust, CAREIT, positioning itself to benefit from scalable property management fee income.

Financial Performance Highlights

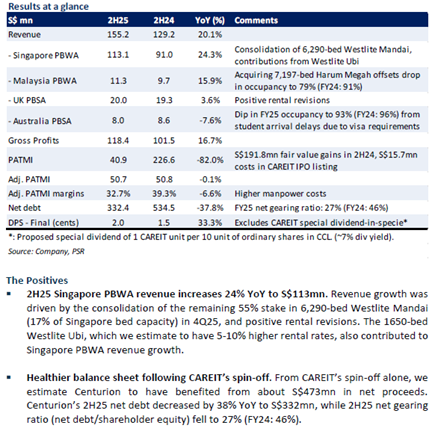

Centurion delivered mixed results in 2H25, with revenue exceeding expectations at 105% of full-year forecasts, reaching S$155.2 million. This strong revenue performance was primarily driven by the consolidation of the remaining 55% stake in the 6,290-bed Westlite Mandai facility, which represents 17% of Singapore’s bed capacity. However, adjusted profit after tax and minority interests (PATMI) fell short of expectations at 91% of forecasts, impacted by a 33% year-on-year increase in administrative fees due to higher manpower costs.

Key Positive Developments

Singapore PBWA operations demonstrated robust growth, with 2H25 revenue increasing 24% year-on-year to S$113 million. Beyond the Westlite Mandai consolidation, positive rental revisions contributed to this growth. The newly operational 1,650-bed Westlite Ubi facility, featuring rental rates estimated to be 5-10% higher than existing properties, further supported Singapore revenue expansion.

The company’s balance sheet has strengthened significantly following CAREIT’s spin-off, generating approximately S$473 million in net proceeds. Net debt decreased 38% year-on-year to S$332 million, whilst the net gearing ratio improved substantially to 27% from 46% in FY24.

CAREIT’s property management fees present a promising revenue stream, with Centurion recognising S$6.5 million in revenue and S$3.2 million in PATMI during 4Q25, achieving a healthy 49% profit margin. Analysts estimate CAREIT’s revenue will grow 25% year-on-year in FY26, potentially generating approximately S$16 million in property management fees for Centurion.

Challenges

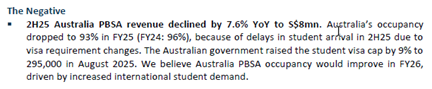

Australia PBSA operations faced headwinds, with revenue declining 7.6% year-on-year to S$9 million. Occupancy rates dropped to 93% from 96% in FY24, primarily due to student arrival delays caused by visa requirement changes. However, the Australian government’s decision to raise the student visa cap by 9% to 295,000 in August 2025 suggests potential recovery ahead.

Investment Outlook

Phillip Securities Research maintains a BUY recommendation with an unchanged target price of S$1.81. The firm expects FY26 consolidated adjusted PATMI to decline approximately 14% year-on-year due to increased profit attributable to minority interests from CAREIT’s inclusion. Centurion has proposed a special dividend-in-specie distribution of one CAREIT unit for every ten Centurion shares, estimated to yield shareholders approximately 7%.

Frequently Asked Questions

Q: What drove Centurion’s strong revenue performance in 2H25?

A: Revenue exceeded expectations primarily due to the consolidation of the remaining 55% stake in the 6,290-bed Westlite Mandai facility and positive rental revisions across the Singapore PBWA portfolio.

Q: Why did adjusted PATMI fall below expectations despite strong revenue?

A: Adjusted PATMI was impacted by a 33% year-on-year increase in administrative fees, excluding CAREIT IPO fees, primarily due to higher manpower costs.

Q: How significant is the CAREIT property management fee income?

A: In 4Q25, Centurion recognised S$6.5 million in revenue and S$3.2 million in PATMI from CAREIT property management fees, with a healthy 49% profit margin. This income stream is estimated to grow 25% year-on-year in FY26.

Q: What challenges did the Australia PBSA segment face?

A: Australia PBSA revenue declined 7.6% year-on-year due to occupancy dropping to 93% from 96%, caused by delays in student arrivals due to visa requirement changes.

Q: How has Centurion’s balance sheet improved?

A: Following CAREIT’s spin-off, net debt decreased 38% year-on-year to S$332 million, and the net gearing ratio improved to 27% from 46% in FY24, benefiting from approximately S$473 million in net proceeds.

Q: What is Phillip Securities Research’s recommendation?

A: Phillip Securities Research maintains a BUY recommendation with an unchanged target price of S$1.81, before the dividend-in-specie distribution.

Q: What special dividend is Centurion proposing?

A: Centurion has proposed a special dividend-in-specie distribution of one CAREIT unit for every ten Centurion shares, estimated to yield shareholders approximately 7%.

Q: What is the outlook for Australia PBSA operations?

A: The Australian government raised the student visa cap by 9% to 295,000 in August 2025, which is expected to improve Australia PBSA occupancy in FY26 through increased international student demand.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.