Company Overview

China Aviation Oil (CAO) operates as a leading jet fuel supplier and trader, serving as a critical link in China’s aviation fuel supply chain. The company’s business model centres on jet fuel supply and trading activities, with significant exposure to China’s aviation recovery through its associate Shanghai Pudong International Airport.

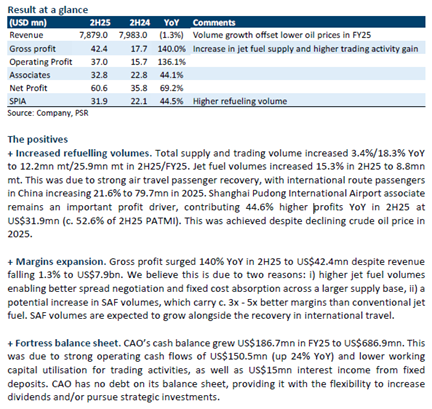

Exceptional Financial Performance

CAO delivered impressive results in the second half of 2025, with profit after tax and minority interests (PATMI) exceeding expectations at 55% and 77% of full-year forecasts respectively. The company demonstrated remarkable operational efficiency as gross profit surged 140% year-on-year to US$42.4 million in 2H25, despite revenue declining 1.3% to US$7.9 billion due to lower oil prices.

Strong Volume Growth Drives Recovery

The company’s operational metrics reflect China’s robust aviation recovery. Total supply and trading volumes increased 3.4% year-on-year to 12.15 million metric tonnes in 2H25, whilst jet fuel volumes rose significantly by 15.3% to 8.8 million metric tonnes. This growth was underpinned by China’s passenger volume recovery, which increased 5.5% to 770 million passengers, with international route passengers surging 21.6% to 79.7 million.

Shanghai Pudong International Airport (SPIA) remained a cornerstone of profitability, contributing US$31.9 million in 2H25 profits—44.6% higher year-on-year and representing 52.6% of total PATMI.

Key Positives Driving Performance

The margin expansion story reflects two critical factors: enhanced negotiating power from higher jet fuel volumes enabling better spread negotiations and improved fixed cost absorption across a larger supply base. Additionally, potential increases in sustainable aviation fuel (SAF) volumes, which carry margins three to five times higher than conventional jet fuel, contributed to profitability improvements.

CAO maintains a fortress balance sheet with US$686.9 million in cash and no debt, providing strategic flexibility for dividend increases and investments.

Research Outlook

Phillip Securities Research maintains a BUY rating with an upgraded target price of S$2.53, previously S$1.50. The research house increased FY26 PATMI forecasts by 32% to account for continued air travel recovery and SPIA’s Terminal 3 expansion, which will increase passenger handling capacity by approximately 62.5%.

Frequently Asked Questions

Q: What drove CAO’s strong financial performance in 2H25?

A: Jet fuel volumes increased 15.3% year-on-year to 8.8 million metric tonnes, whilst gross profit surged 140% to US$42.4 million due to margin expansion and higher refuelling volumes supported by China’s passenger volume recovery.

Q: How significant is Shanghai Pudong International Airport to CAO’s profitability?

A: SPIA contributed US$31.9 million in 2H25 profits, representing 44.6% higher year-on-year growth and accounting for 52.6% of CAO’s total PATMI in the period.

Q: What is Phillip Securities Research’s recommendation and target price?

A: Phillip Securities Research maintains a BUY rating with an upgraded target price of S$2.53, increased from the previous S$1.50, representing a 32% increase in FY26 PATMI forecasts.

Q: Why did margins expand despite lower oil prices?

A: Margin expansion resulted from higher jet fuel volumes enabling better spread negotiation and fixed cost absorption, plus potential increases in sustainable aviation fuel volumes, which carry margins three to five times higher than conventional jet fuel.

Q: What is CAO’s financial position?

A: CAO maintains a strong net cash position of US$686.9 million with no debt, providing flexibility for dividend increases and strategic investments. Cash balance grew US$186.7 million in FY25 due to strong operating cash flows of US$150.5 million.

Q: What growth drivers support the upgraded forecasts?

A: Growth will arise from higher passenger volumes following SPIA’s Terminal 3 expansion, which increases passenger handling capacity by approximately 62.5%, and strategic investments supporting the growing SAF business.

Q: How did passenger recovery impact CAO’s operations??

A: China’s passenger volumes increased 5.5% to 770 million, with international route passengers surging 21.6% to 79.7 million, directly supporting the 15.3% increase in jet fuel volumes.

Q: What role does sustainable aviation fuel play in CAO’s strategy?

A: SAF volumes are expected to grow alongside international travel recovery and carry margins three to five times better than conventional jet fuel, contributing to the company’s profitability expansion.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.