Disappointing First Quarter Performance

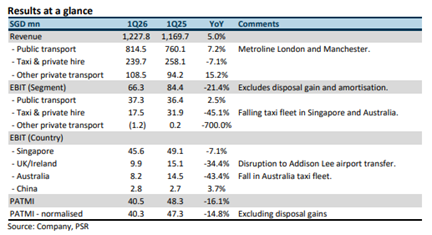

ComfortDelGro Corp Ltd delivered a challenging first quarter in FY26, with revenue and profit after tax and minority interests (PATMI) falling significantly short of expectations at just 22% and 19% of full-year forecasts respectively. The underlying PATMI declined 16% year-on-year to S$40.5 million, with the company’s taxi operations bearing the brunt of the weakness.

Company Overview

ComfortDelGro operates as a leading land transport company across multiple markets, with core businesses including taxi services in Singapore and Australia, bus operations through Metroline in London and Manchester, and airport transfer services via Addison Lee in the UK. The company is transitioning towards a hybrid peer-to-peer model in Singapore that incorporates autonomous technology.

Key Challenges Weighing on Performance

The most significant drag on earnings came from taxi operations, where operating profit plunged 45% year-on-year to S$17.5 million. This decline was driven by multiple factors, including a 7% reduction in Singapore’s taxi fleet and a 10% decrease in Australia’s fleet size year-on-year. Consumer spending on private hire services has weakened considerably, creating additional headwinds for the taxi division.

The company also faced disruption in its UK operations, particularly affecting Addison Lee’s airport transfer bookings for Middle East airlines, which contributed to the overall earnings pressure.

Limited Bright Spots

Despite the challenging operating environment, ComfortDelGro did see some improvement in its London bus contract margins through Metroline. However, this positive development was insufficient to offset the broader weakness, with UK and public transport margins declining year-on-year.

Outlook and Analyst Recommendation

Phillip Securities Research has responded to these challenges by lowering FY26 earnings forecasts by 11% to S$190.6 million. The firm has also reduced its DCF target price to S$1.35 and downgraded its recommendation from ACCUMULATE to NEUTRAL.

The research house expects continued pressure from higher fuel prices, additional surcharges, and weaker economic conditions, which are likely to soften consumer spending on premium transportation services. The taxi operations face particular challenges from intense competition and declining fleet sizes, creating a difficult operating environment for the foreseeable future.

Frequently Asked Questions

Q: How did ComfortDelGro's first quarter results compare to expectations?

A: The results were significantly below expectations, with revenue and PATMI representing only 22% and 19% of full-year forecasts respectively. Underlying PATMI fell 16% year-on-year to S$40.5 million.

Q: What were the main reasons for the poor performance?

A: The primary reasons were declining taxi fleets in Singapore and Australia, with decreases of 7% and 10% respectively , weaker consumer spending on private hire services, and disruption to Middle East airlines' airport transfer bookings in the UK.

Q: How much did taxi operating profit decline?

A: Taxi operating profit plunged 45% year-on-year to S$17.5 million, representing the largest drag on overall earnings performance.

Q: What is Phillip Securities Research's new recommendation and target price?

A: The firm downgraded ComfortDelGro from ACCUMULATE to NEUTRAL and lowered its DCF target price to S$1.35.

Q: Were there any positive developments in the results?

A: Yes, Metroline London contract margins continued to improve, although this was not particularly impactful in the first quarter results, as UK and public transport margins declined year-on-year.

Q: How much did Phillip Securities lower its earnings forecast?

A: The research house reduced its FY26 earnings forecast by 11% to S$190.6 million.

Q: What challenges does ComfortDelGro face going forward?

A: The company faces pressure from higher fuel prices, additional surcharges, weaker economic conditions, intense competition in taxi operations, and declining fleet sizes.

Q: What strategic changes is ComfortDelGro implementing?

A: The company is transitioning to a more hybrid peer-to-peer model in Singapore that includes autonomous technology.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.