DBS Group Holdings Ltd, Singapore’s largest bank, has demonstrated resilience in a challenging operating environment by maintaining its dividend policy despite facing earnings pressures.

Financial Performance and Dividend Policy

DBS reported adjusted earnings of S$2.4 billion for 4Q25, representing a slight shortfall against analyst estimates with full year FY25 earnings at 95% of full-year forecasts. Despite the earnings decline, the bank significantly increased its quarterly dividend per share by 35% year-on-year to 81 cents, comprising 66 cents ordinary dividend and 15 cents capital return dividend. The total FY25 dividend per share reached S$3.06, marking a substantial 38% increase from the previous year.

Mixed Operational Results

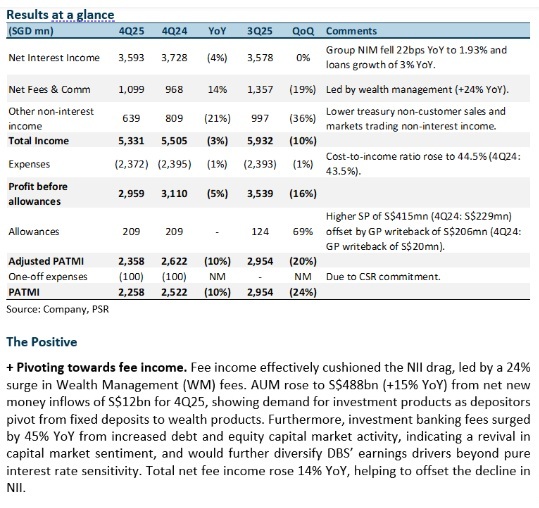

The bank faced headwinds in its core lending business, with net interest income declining 4% year-on-year despite achieving loan and deposit growth. This decline was attributed to net interest margins compressing by 22 basis points to 1.93%. However, these challenges were partially offset by strong performance in fee-generating businesses, particularly wealth management, which surged 24% year-on-year and drove overall fee income growth of 14%.

Key Positives: Strategic Pivot Toward Fee Income

The bank’s strategic pivot toward fee income generation has proven effective in cushioning the impact of declining net interest income. Wealth management fees led this transformation, supported by assets under management rising to S$488 billion, representing 15% year-on-year growth. This growth was driven by net new money inflows of S$12 billion in 4Q25, demonstrating strong demand for investment products as depositors shift from fixed deposits to wealth products. Additionally, investment banking fees surged 45% year-on-year, benefiting from increased debt and equity capital market activity, which indicates a revival in capital market sentiment and further diversifies DBS’s earnings drivers beyond pure interest rate sensitivity.

Research Recommendation and Outlook

Phillip Securities Research has upgraded DBS to Accumulate from Neutral, raising the target price to S$60.00 from the previous S$58.00. The upgrade reflects expectations that non-interest income will serve as the main growth driver, with heightened market volatility benefiting trading income and continued wealth management growth. The research firm prefers DBS among Singapore banks due to its continued capital return plans until FY27, fixed dividend per share policy, and high dividend payout ratio, offering greater stability compared to peers following floating payout ratios.

Frequently Asked Questions

Q: What was DBS’s dividend policy for FY25?

A: DBS raised its 4Q25 dividend per share by 35% year-on-year to 81 cents, comprising 66 cents ordinary dividend and 15 cents capital return dividend, bringing total FY25 dividend per share to S$3.06, up 38% year-on-year.

Q: How did DBS’s net interest income perform?

A: Net interest income fell 4% year-on-year despite loan and deposit growth, as net interest margins declined 22 basis points year-on-year to 1.93%.

Q: Which business segments showed strong growth?

A: Wealth management fees surged 24% year-on-year, driving 14% growth in fee income. Investment banking fees also increased 45% year-on-year from increased debt and equity capital market activity.

Q: What is Phillip Securities Research’s recommendation and target price?

A: Phillip Securities Research upgraded DBS to Accumulate from Neutral with a higher target price of S$60.00, up from the previous S$58.00.

Q: How did assets under management perform?

A: Assets under management rose to S$488 billion, representing 15% year-on-year growth, driven by net new money inflows of S$12 billion for 4Q25.

Q: What is DBS’s guidance for FY26?

A: DBS maintained its FY26 guidance for net interest income to be slightly below 2025 levels, non-interest income growth in the high single digits, credit costs to normalize at 17-20 basis points, and profit after tax and minority interests below 2025 levels due to the lower interest rate environment.

Q: What makes DBS attractive compared to other Singapore banks?

A: Phillip Securities Research prefers DBS due to its continued capital return plans until FY27, fixed dividend per share policy, and high dividend payout ratio, which offer greater stability compared to peers that follow floating payout ratios tied to earnings performance.

Q: What are the expected dividend yields?

A: The expected dividend yields are 5.7% for FY26e and 6.1% for FY27e, supported by DBS’s capital return dividend policy and step-up policy maintained until 3Q26.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.