Company Overview

Elite UK REIT is a real estate investment trust focused on UK commercial properties, with a significant portfolio concentration in assets leased to the Department for Work and Pensions (DWP). The REIT manages a diversified property portfolio valued at £424.6 million, comprising large, medium, and smaller-sized commercial assets across the United Kingdom.

Strong Financial Performance Driven by Strategic Initiatives

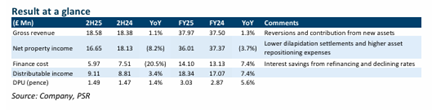

Elite UK REIT delivered impressive results for the second half and full year 2025, with distribution per unit (DPU) reaching 1.49 pence for 2H25 and 3.03 pence for FY25, representing year-over-year growth of 1.4% and 5.6% respectively.The full-year DPU met Phillip Securities Research’s FY25 forecast, while the 2H25 contribution accounted for 49% of the projected total. The growth was primarily attributed to interest savings from a reduced cost of debt, which decreased from 4.9% in FY24 to 4.7% in FY25, alongside contributions from newly acquired assets. These factors contributed to a substantial 7.4% year-over-year increase in distributable income, reaching £18.3 million in FY25.

Major Lease Regearing Success Addresses Key Risk

The REIT achieved a significant milestone by successfully regearing approximately 70% of its DWP portfolio, representing £24.3 million in rent, well ahead of the 2028 lease expiry deadline. This strategic accomplishment increased the weighted average lease expiry (WALE) dramatically from 2.4 years to 7.2 years, with leases primarily regeared for longer tenors of 7 and 10 years. The regeared leases feature CPI-linked rent reviews scheduled for 2033, with compounded annual rent increases ranging between 1% and 5% and notably contain no lease break clauses. Additionally, the Peel Park asset received planning approval for data centre facility use, potentially unlocking significant divestment value.

Investment Recommendation and Outlook

Phillip Securities Research upgraded Elite UK REIT to BUY with a higher target price of S$0.41, increased from the previous S$0.39, based on a dividend discount model approach. The REIT offers an attractive FY26 dividend yield of approximately 8.9%, considerably higher than the broader S-REITs market distribution yield of around 6% in 2025. A potential upside catalyst includes a DPU-accretive divestment of Peel Park, which currently represents approximately 10% of the total portfolio value and stands as the largest asset by value.

Key Takeaways

Q: What drove Elite UK REIT’s improved financial performance in FY25?

A: The 5.6% year-over-year growth in FY25 DPU was driven by interest savings from a lower cost of debt (decreasing from 4.9% to 4.7%) and contributions from newly acquired assets, resulting in 7.4% growth in distributable income to £18.3 million.

Q: How successful was the lease regearing with DWP?

A: Elite successfully regeared around 70% of the DWP portfolio representing £24.3 million in rent, significantly ahead of the 2028 lease expiry. This increased WALE from 2.4 years to 7.2 years with leases regeared for 7 and 10-year tenors.

Q: What is Phillip Securities Research’s recommendation and target price?

A: Phillip Securities Research upgraded Elite UK REIT to BUY with a target price of S$0.41, increased from the previous S$0.39, based on a dividend discount model approach.

Q: How does Elite’s dividend yield compare to the broader market?

A: Elite offers an FY26 dividend yield of approximately 8.9%, which is considerably higher than the S-REITs market distribution yield of around 6% in 2025.

Q: What are the key features of the regeared leases?

A: The regeared leases have no break clauses, feature CPI-linked rent reviews in 2033 with compounded annual rent increases of 1-5% and include renewal options for DWP extending leases by five years for 2035 expiries and three years for earlier expiries.

Q: What potential upside catalyst exists for the REIT?

A: A potential DPU-accretive divestment of Peel Park, which represents approximately 10% of total portfolio value and is the largest asset by value, especially after receiving planning approval for data centre facility use.

Q: How did the portfolio valuation perform?

A: The latest portfolio valuation showed an uplift of approximately 2% year-over-year to £424.6 million, with 72% of large assets appreciating in value and 43% delivering double-digit valuation gains, offsetting declines in smaller assets.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.