Company Overview

Ever Glory United Holdings Ltd is a prominent mechanical and electrical (M&E) services provider in Singapore. Following its strategic acquisition of Guthrie, the company has positioned itself as one of the largest M&E players in the Singapore market, specialising in complex infrastructure projects including airport facilities, hospitals, and transportation systems.

Strong Financial Performance Driven by Strategic Acquisition

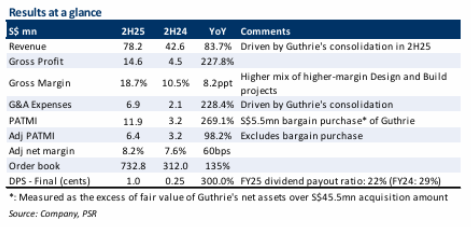

Ever Glory delivered exceptional results in 2H25, with revenue and adjusted profit after tax and minority interests (PATMI) exceeding expectations at 128% and 122% of forecasts respectively. The company’s adjusted PATMI surged 98% year-on-year to S$6.4 million, primarily driven by the consolidation of Guthrie’s operations. Additionally, Ever Glory realised a S$5.5 million bargain purchase gain from the Guthrie acquisition, representing the excess of net assets’ fair value over the acquisition amount.

Record Order Book and Growth Prospects

The company’s order book experienced remarkable growth, surging 135% year-on-year to S$733 million in 2H25. This substantial increase was fuelled by S$508 million in new contracts secured during 2025, including a significant approximately S$200 million electrical contract for the Alexandra Integrated Hospital redevelopment, alongside maintenance contracts for street lighting and bus depot facility upgrades.

Key Strengths and Market Position

Guthrie brings considerable expertise and a proven track record to Ever Glory’s operations. At the time of acquisition, Guthrie contributed an order book worth S$312 million, representing approximately 43% of Ever Glory’s current total order book. The acquired company has successfully completed major M&E projects, including air-conditioning and mechanical ventilation works for prestigious developments such as Jewel Changi Airport and Funan CapitaLand, as well as lighting services for Changi Airport Runway 3.

The enhanced capabilities position Ever Glory to compete for high-value future contracts, including potential projects such as Changi Airport Terminal 5 building and airfield electrical works, LTA MRT tunnel lighting systems, and additional hospital infrastructure contracts.

Research Recommendation and Outlook

Phillip Securities Research has upgraded Ever Glory to BUY from ACCUMULATE, raising the target price to S$1.05 from S$0.81. The revised valuation is based on 18x FY27e price-to-earnings ratio, representing a 10% discount to its peers’ two-year forward PE of 20x. The research fim forecasts revenue and adjusted PATMI to grow at compound annual growth rates of 25% and 36% respectively over the next two years, supported by the record S$733 million order book, which is estimated to provide work for 4-5 years with significant revenue recognition expected towards the latter part of this period.

Frequently Asked Questions

Q: What was the key driver behind Ever Glory’s strong 2H25 performance?

A: The primary driver was the consolidation of Guthrie’s results following the acquisition. Adjusted PATMI spiked 98% year-on-year to S$6.4 million, excluding the S$5.5 million bargain purchase gain.

Q: How significant was the growth in Ever Glory’s order book?

A: The order book surged 135% year-on-year to S$733 million in 2H25, driven by S$508 million in new contracts secured during 2025, including a major electrical contract worth approximately S$200 million for Alexandra Integrated Hospital redevelopment.

Q: What is Guthrie’s contribution to Ever Glory’s business?

A: Guthrie brought an order book of S$312 million at acquisition (43% of Ever Glory’s current total) and has a strong track record of completing major M&E projects, including work at Jewel Changi Airport, Funan CapitaLand, and Changi Airport Runway 3 lighting services.

Q: What is Phillip Securities Research’s current recommendation and target price?

A: The research house upgraded Ever Glory to BUY from ACCUMULATE with a higher target price of S$1.05, up from the previous S$0.81.

Q: What growth prospects does the research identify for Ever Glory?

A: The research forecasts revenue and adjusted PATMI to grow at CAGRs of 25% and 36% respectively over the next two years, with potential to secure high-value contracts such as Changi Airport T5 projects, LTA MRT tunnel lighting, and hospital contracts.

Q: How long is the current order book expected to last?

A: The S$733 million order book is estimated to provide work for 4-5 years, with significant revenue recognition expected towards the back end of this period.

Q: Were there any negative factors identified in the research?

A: No significant concerns were identified in the research firm’s analysis.

This article has been auto-generated using AI tools. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.