Strong First Half Performance Drives Confidence

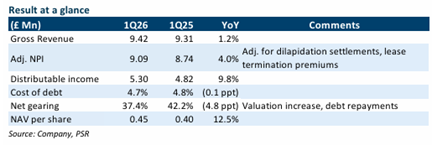

Frasers Centrepoint Trust (FCT) has demonstrated resilience in challenging market conditions, delivering a solid first half performance that reinforces its position as a defensive suburban retail specialist. The trust reported a 1.4% year-on-year increase in distribution per unit to 6.14 Singapore cents for 1H26, meeting expectations and representing 49% of the full-year forecast. Net property income surged 20.2% to S$160.8 million, primarily driven by the acquisition of Northpoint City South Wing and higher passing rents, though this was partially offset by the divestment of Yishun 10 Retail Podium and asset enhancement initiative disruptions at Hougang Mall.

The Positives: Operational Excellence and Financial Stability

FCT’s operational metrics showcase the strength of its defensive suburban mall portfolio. Portfolio occupancy improved significantly by 1.7 percentage points quarter-on-quarter to an impressive 99.8%, driven by successful backfilling of cinema spaces at Causeway Point and Century Square. The trust has also secured Xventure, a new indoor sports and adventure park concept, to replace Golden Village at Tiong Bahru Plaza, demonstrating proactive tenant management.

Despite broader economic uncertainties, FCT’s portfolio anchored by essential services continues to attract shoppers, with traffic rising 2.4% year-on-year whilst tenant sales increased 3.6% in the second quarter. This performance underscores the resilience of suburban malls that cater to everyday needs rather than discretionary spending.

The trust has also maintained disciplined capital management, with the average all-in cost of debt improving by 30 basis points quarter-on-quarter to 3.2%. With 66% of borrowings hedged to fixed rates and aggregate leverage improving slightly to 40%, FCT has positioned itself well for continued stability. Having successfully refinanced all maturities due in the current financial year, the trust expects its all-in cost of debt to remain around 3.3% for the full year.

Investment Outlook

Phillip Securities Research maintains a BUY recommendation with a revised target price of S$2.70, down from S$2.74, reflecting a 1% trim to the distribution forecast to account for partial downtime from the NEX asset enhancement initiative. The trust remains the top pick in the retail sub-sector, supported by expectations of healthy rental reversions of 5% and limited new retail supply. Trading at a forward yield of 5.4%, FCT offers attractive income potential whilst benefiting from organic growth through successful asset enhancement completions.

Frequently Asked Questions

Q: What drove FCT's strong net property income growth in 1H26?

A: Net property income increased 20.2% to S$160.8 million, primarily driven by the acquisition of Northpoint City South Wing and higher passing rents, partially offset by the divestment of Yishun 10 Retail Podium and disruption from asset enhancement initiatives at Hougang Mall.

Q: How has FCT's portfolio occupancy performed?

A: Portfolio occupancy improved significantly by 1.7 percentage points quarter-on-quarter to 99.8%, driven by successful backfilling of cinema spaces at Causeway Point and Century Square.

Q: What is FCT's current financial position regarding debt management?

A: FCT's average all-in cost of debt improved by 30 basis points to 3.2% in 2Q26, with 66% of borrowings hedged to fixed rates and aggregate leverage at 40%. The trust has refinanced all maturities due in the current financial year.

Q: What is Phillip Securities Research's recommendation and target price?

A: Phillip Securities Research maintains a BUY rating with a target price of S$2.70, reduced from the previous S$2.74, whilst trimming the distribution forecast by 1% to account for NEX asset enhancement downtime.

Q: How resilient has FCT's portfolio been amid economic uncertainty?

A: Despite macro uncertainty, shopper traffic rose 2.4% year-on-year and tenant sales increased 3.6% in 2Q26, demonstrating the defensive nature of FCT's suburban mall portfolio anchored by essential services.

Q: What are the key growth drivers for FCT going forward?

A: Expected rental reversions of 5% supported by limited new retail supply, successful asset enhancement initiative completions driving higher yields, and the defensive nature of suburban malls serving essential services are key growth drivers.

Q: What forward yield does FCT currently offer investors?

A: FCT is trading at a forward yield of 5.4% for the financial year, providing attractive income potential for investors seeking defensive retail exposure.

Q: How have rental reversions performed for FCT?

A: Rental reversions remained healthy at +6.5% in 1H26, compared to +7.8% for the previous full financial year, indicating continued pricing power despite market challenges.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.