Keppel DC REIT has delivered a solid first quarter performance for FY26, with distribution per unit (DPU) reaching 2.833 Singapore cents, representing a 13.2% year-on-year increase. The REIT, which operates a portfolio of data centre properties across key markets, demonstrated resilient fundamentals despite some operational challenges.

Strong Financial Performance Driven by Strategic Acquisitions

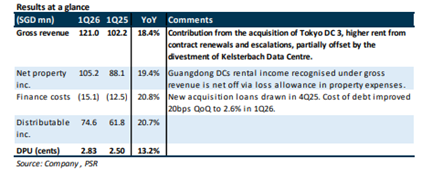

The quarterly results were in line with expectations, forming 26% of full-year estimates. Growth was primarily attributed to the acquisitions of Tokyo Data Centre 3 and the remaining interests in Keppel DC Singapore 3 & 4, alongside stronger contributions from contract renewals and escalations. These gains were partially offset by the divestment of Kaltenbach Data Centre.

Portfolio rental reversion remained robust at 51% during the quarter, an improvement from the full-year FY25 figure of 45%. However, this strong performance was based on a very small percentage of total leases, approximately 0.3% of the portfolio. Portfolio occupancy eased slightly by 0.2 percentage points to 95.6%, primarily due to client downsizing of non-data centre space, whilst the portfolio weighted average lease expiry (WALE) remained healthy at 6.5 years.

Positive Financial Metrics Support Growth Strategy

The REIT’s financial position showed continued strength with the average cost of debt declining 20 basis points quarter-on-quarter to 2.6%, with 84.8% of loans secured on fixed rates. Aggregate leverage stood at 35.1%, providing approximately S$550 million of debt headroom against the 40% internal cap to support future acquisitions. Management expects the cost of debt to remain stable at 2.6% through FY26, with only 8.5% of debt due for refinancing during the year.

Ongoing Challenges in Guangdong Operations

The primary concern remains the ongoing weakness at the Guangdong Data Centres, where KDCREIT continues to recognise loss allowances for overdue rent. Bluesea, the master lessee, has accumulated over S$55 million in unpaid rent to date, with chip availability continuing to present bottlenecks in China.

Phillip Securities Research maintains an ACCUMULATE recommendation with an unchanged dividend discount model-derived target price of S$2.37. The potential recovery of overdue rent from Bluesea remains a key catalyst, though this issue remains unresolved. The stock currently trades at an FY26 DPU yield of 4.6%.

Frequently Asked Questions

Q: What was Keppel DC REIT's DPU performance in Q1 FY26?

A: The REIT achieved a DPU of 2.833 Singapore cents, representing a 13.2% year-on-year increase and forming 26% of full-year estimates.

Q: What drove the growth in Q1 FY26 results?

A: Growth was primarily driven by acquisitions of Tokyo Data Centre 3 and remaining interests in Keppel DC Singapore 3 & 4, plus stronger contributions from contract renewals and escalations, partially offset by the Kaltenbach Data Centre divestment.

Q: How strong were the rental reversions during the quarter?

A: Portfolio rental reversion remained robust at 51%, improving from the FY25 level of 45%, though this was based on approximately 0.3% of total leases.

Q: What is the current financial position regarding debt?

A: The average cost of debt declined to 2.6% with 84.8% of loans on fixed rates. Aggregate leverage stands at 35.1%, providing around S$550 million debt headroom against the 40% internal cap.

Q: What are the main challenges facing the REIT?

A: The primary concern is the ongoing weakness at Guangdong Data Centres, where master lessee Bluesea has accumulated over S$55 million in unpaid rent, with chip availability continuing as a bottleneck in China.

Q: What is Phillip Securities Research's recommendation?

A: Phillip Securities Research maintains an ACCUMULATE rating with an unchanged target price of S$2.37 derived from their dividend discount model.

Q: What is the current portfolio occupancy rate?

A: Portfolio occupancy eased slightly by 0.2 percentage points to 95.6%, primarily due to client downsizing of non-data centre space, whilst WALE remained healthy at 6.5 years.

Q: What potential catalyst could impact future performance?

A: The potential recovery of over S$55 million in overdue rent from Bluesea remains a key catalyst, though this issue currently remains unresolved.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.