Company Overview

Lendlease Global Commercial REIT (LREIT) is a Singapore-listed real estate investment trust that owns a diversified portfolio of commercial properties, including retail malls and office buildings across Singapore and Milan. The REIT’s key Singapore retail assets include Jem, 313@somerset, and the recently acquired PLQ Mall, alongside Milan office properties.

Strong Retail Fundamentals Drive Performance

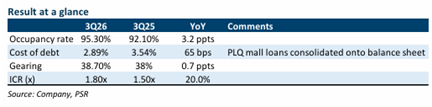

LREIT’s Singapore retail portfolio continues to demonstrate robust fundamentals, with rental reversion for year-to-date renewed leases increasing by an impressive 12.2%. This strong performance was driven by resilient demand from Chinese food and beverage operators, gold and jewellery retailers, sporting goods stores, and athleisure tenants. The portfolio maintained healthy occupancy levels at 95.3%, representing a 0.4 percentage point improvement quarter-on-quarter.

Jem and 313@somerset both delivered mid- to high-single-digit rental reversions, whilst PLQ Mall is expected to achieve even higher reversions compared to legacy assets. Management expects this positive momentum to continue, with high-single to low-double-digit reversion anticipated to persist into the fourth quarter of 2026.

PLQ Mall Integration Progressing Well

The integration of PLQ Mall, which was fully acquired as of March 2026, is proceeding according to plan. Asset enhancement initiatives covering approximately 16,000 square feet across levels 1 and 2 are underway, with level 1 space already pre-leased and level 2 leasing currently in progress. Income contribution from these reconfigured spaces is expected to commence in the second half of 2027, with peak downtime anticipated during October and November 2027.

The PLQ Mall acquisition has strengthened LREIT’s financial position through successful loan refinancing, securing approximately S$2 million in annual all-in debt cost savings. The conversion to a limited liability partnership structure is targeted for completion by end June 2026, with the overall acquisition expected to deliver 2% distribution per unit accretion.

Enhanced Capital Structure

LREIT’s capital structure has strengthened significantly, with the interest coverage ratio improving to 1.8 times from 1.5 times in the third quarter of 2025. This improvement was supported by the divestment of Jem office in November 2025, PLQ Mall loan refinancing, and the replacement of S$200 million perpetual securities with cheaper funding alternatives. Consequently, the weighted average cost of debt decreased to 2.89% per annum from approximately 3.5% a year ago.

Investment Outlook

Phillip Securities Research maintains its BUY recommendation for LREIT, with the trust trading at a financial year 2026 estimated price-to-net asset value of 0.70 times and offering a dividend yield of approximately 5.86%. The strengthening capital structure and PLQ Mall reconfiguration are identified as key positive drivers, though these are partially offset by challenges from Milan Building 3.

Frequently Asked Questions

Q: What was LREIT's retail rental reversion performance?

A: Singapore retail rental reversion for year-to-date renewed leases increased by 12.2%, with Jem and 313@somerset delivering mid- to high-single-digit reversions.

Q: What is the current occupancy rate of LREIT's portfolio?

A: Portfolio occupancy stands at 95.3%, representing a 0.4 percentage point improvement quarter-on-quarter.

Q: When will the PLQ Mall enhancement works generate income?

A: Income contribution from the reconfigured spaces is expected to begin in the second half of 2027, with peak downtime anticipated in October and November 2027.

Q: What is the expected impact of the PLQ Mall acquisition?

A: The PLQ Mall acquisition is expected to deliver 2% distribution per unit accretion to LREIT.

Q: How has LREIT's cost of debt changed?

A: The weighted average cost of debt fell to 2.89% per annum from approximately 3.5% a year ago, following various refinancing initiatives.

Q: What is Phillip Securities Research's recommendation and target metrics?

A: Phillip Securities Research maintains a BUY recommendation, with LREIT trading at a financial year 2026 estimated price-to-net asset value of 0.70 times and a dividend yield of approximately 5.86%.

Q: What are the key positive drivers for LREIT?

A: Key drivers include the strengthening capital structure and PLQ Mall reconfiguration, though these are partially offset by the drag from Milan Building 3.

Q: How did LREIT's interest coverage ratio improve?

A: The interest coverage ratio improved to 1.8 times from 1.5 times in the third quarter of 2025, supported by asset divestment, loan refinancing, and replacement of perpetual securities with cheaper funding.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.