Company Overview

LHN Ltd operates a diversified business portfolio encompassing industrial facilities, facilities management, co-living operations through its Coliwoo brand, and property development. The company has positioned itself as a key player in Singapore’s co-living market whilst maintaining traditional property-related revenue streams.

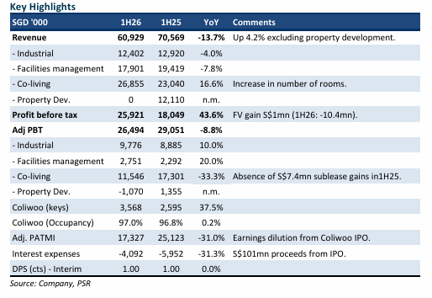

Mixed Performance in 1H26 Results

LHN Ltd delivered 1H26 results that met expectations, with revenue and adjusted profit after tax and minority interests representing 43% and 49% of full-year forecasts respectively. However, overall revenue declined 14% due to the complete absence of property development revenue during the period. The company maintained its interim dividend at 1 cent, demonstrating its commitment to shareholder returns despite the revenue headwinds.

Strong Co-Living Portfolio Expansion

The standout performer was Coliwoo, LHN’s co-living franchise, which demonstrated impressive growth metrics. The portfolio expanded significantly, with room count increasing 38% year-on-year to 3,568 units. This growth was bolstered by the March opening of Coliwoo Midtown on Middle Road, which contributed 212 rooms and achieved 55% occupancy since launch. The co-living division generated revenue of S$26.9 million, representing a robust 17% year-on-year increase driven by the substantial expansion in room inventory.

Demand fundamentals remain exceptionally strong, with average occupancy across the portfolio maintained at an impressive 97% level. The pipeline remains healthy, with another 1,021 rooms scheduled for development, representing a 29% increase to the current portfolio size.

Key Positives and Negatives

The Positive: Strong growth momentum in the Coliwoo portfolio underpinned performance, with revenue climbing 17% year-on-year to S$26.9 million supported by the 38% jump in room keys. The second half of FY26 is expected to deliver stronger performance as Coliwoo Midtown continues to ramp up occupancy levels.

The Negative: Property development operations faced significant challenges, recording zero sales from the 55 Tuas South Avenue 1 project during 1H26. Whilst two units were sold in April, only 9 of the 49 launched units have been sold to date, with the company now considering rental options for the remaining properties.

Investment Outlook and Recommendation

Phillip Securities Research maintains its BUY recommendation whilst adjusting the target price to S$0.77 from the previous S$0.85, reflecting a decline in Coliwoo’s market capitalisation. The valuation methodology applies a 20% discount to mark-to-market valuation due to price volatility, with property development valued at book value and remaining business valued at 10 times price-to-earnings ratio. The company offers an attractive dividend yield of 6.5%, with future growth expected from expanding the co-living franchise into dormitories for the services industry.

Frequently Asked Questions

Q: What were LHN Ltd's key financial results for 1H26?

A: Revenue and adjusted PATMI were 43% and 49% of full-year forecasts respectively. Overall revenue declined 14% due to the absence of property development revenue, whilst the interim dividend remained unchanged at 1 cent.

Q: How did the Coliwoo co-living business perform?

A: Coliwoo showed strong growth, with room count increasing 38% year-on-year to 3,568 units and revenue rising 17% to S$26.9 million. Average occupancy remained high at 97%.

Q: What is the growth pipeline for Coliwoo?

A: There are 1,021 rooms in the development pipeline, representing a 29% increase to the current portfolio. Coliwoo Midtown opened in March with 212 rooms and has achieved 55% occupancy since launch.

Q: What challenges did the property development division face?

A: The property development segment recorded no sales from the 55 Tuas South Avenue 1 project in 1H26. Only 9 of the 49 launched units have been sold, with the company now considering rental options for the remaining properties.

Q: What is Phillip Securities Research's investment recommendation?

A: Phillip Securities Research maintains a BUY recommendation with a target price of S$0.77, down from the previous S$0.85, reflecting a decline in Coliwoo's market capitalisation.

Q: What is LHN's dividend yield?

A: The company offers an attractive dividend yield of 6.5% to shareholders.

Q: What are the future growth prospects for LHN?

A: The next evolution of the Coliwoo franchise includes expanding into dormitories for the services industry, whilst the co-living business model captures management fees, rental income, and capital gains from assets.

Q: Why was the target price reduced despite maintaining the BUY rating?

A: The target price was lowered due to a decline in Coliwoo's market capitalisation, with a 20% discount applied to mark-to-market valuation due to price volatility.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.