Company Overview

Micron Technology, Inc. is a leading semiconductor company specializing in memory solutions, producing both DRAM and NAND flash memory products for various applications including mobile, client, and automotive markets.

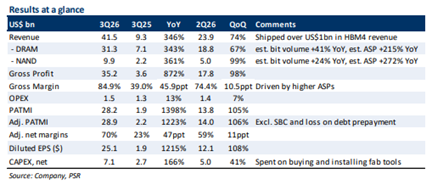

Strong Financial Performance Driven by ASP Surge

Micron delivered exceptional third-quarter FY2026 results, with adjusted profit after tax and minority interests spiking 12.2 times year-on-year to a record US$28.9 billion. This remarkable performance was underpinned by 41% year-on-year bit shipment growth and substantial average selling price (ASP) increases, estimated at 215% for DRAM and 272% for NAND products.

The nine-month FY2026 revenue and adjusted PATMI reached 73% and 72% of full-year forecasts respectively, indicating strong momentum. Revenue surged to US$42 billion whilst profit margins expanded significantly, with gross margins reaching 84.9%, driven primarily by the higher ASPs across both memory segments.

Strategic Customer Agreements Reduce Cyclicality

A key positive development is Micron’s progress in securing long-term strategic customer agreements (SCAs). The company has signed 16 such agreements to date, covering approximately 20% of DRAM volume and 30% of NAND volume from 2026 to 2030. These agreements represent US$100 billion in remaining performance obligations, equivalent to 2.7 times FY25 revenue, with US$22 billion in cash deposits and financial commitments from customers.

The SCAs include price bands with floor prices that enable higher gross margins than Micron’s historical peak of 63%. This structure provides greater revenue visibility and reduces the company’s traditional cyclical exposure, although approximately 75% of revenue remains subject to cyclical demand patterns in mobile, client, and automotive segments.

Market Dynamics Support Pricing Power

Memory supply remains constrained due to lengthy lead times for new fabrication facility expansions, which typically require 2 to 4 years, alongside persistent

cleanroom space limitations. Customers are prioritizing volume security over price considerations, leading major players including Samsung, SK Hynix, and Micron to sign longer-term contracts spanning 3 to 5 years, compared to typical one-year commitments historically.

Investment Recommendation

Phillip Securities Research maintains a BUY rating with a raised target price of US$1870, reflecting increased FY27 revenue and PATMI forecasts raised by 16% and 23% respectively. The valuation assumes a 14 times FY27 price-to-earnings ratio, representing a 52% discount to peers’ average forward P/E of 29 times, acknowledging the remaining cyclical exposure in non-SCA revenue streams.

Frequently Asked Questions

Q: What drove Micron's record financial performance in Q3 2026?

A: The record US$28.9 billion adjusted PATMI was driven by 41% year-on-year bit shipment growth and substantial ASP increases of 215% for DRAM and 272% for NAND products.

Q: How significant are Micron's strategic customer agreements?

A: Micron has signed 16 SCAs representing US$100 billion in remaining performance obligations, covering 20% of DRAM and 30% of NAND volume from 2026 to 2030, with US$22 billion in customer deposits.

Q: What is Phillip Securities' investment recommendation for Micron?

A: Phillip Securities maintains a BUY rating with a raised target price of US$1870, based on improved revenue and profit forecasts.

Q: Why are memory prices rising so dramatically?

A: ASP spikes are driven by constrained supply due to 2 to 4 year lead times for new fab expansions, cleanroom space constraints, and customers prioritizing volume security over price.

Q: How do the SCAs reduce Micron's cyclicality?

A: The SCAs provide revenue visibility through long-term contracts with price floors that enable higher margins than historical peaks, though 75% of revenue remains subject to cyclical demand.

Q: What are the key market dynamics supporting Micron's outlook?

A: Memory supply constraints are expected to persist beyond 2027, with industry players signing longer 3 to 5 year contracts compared with typical one-year commitments historically.

Q: How does Micron's valuation compare to peers?

A: The target price assumes a 52% discount to peers' 29x forward P/E ratio, reflecting remaining cyclical exposure in non-SCA revenue streams.

Q: What were Micron's gross margins in Q3 2026?

A: Gross margins reached 84.9%, driven by higher ASPs, with SCA price floors potentially enabling margins above the historical peak of 63%.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.