Company Overview

OUE REIT is a Singapore-listed real estate investment trust with a diversified portfolio spanning hospitality and office segments. The REIT owns premium properties including hotels and commercial office buildings, positioning itself as a key player in Singapore’s property investment landscape.

Strong Q1 Performance Driven by Hospitality Recovery

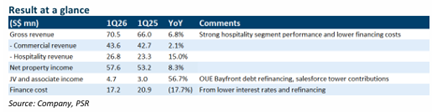

OUE REIT delivered robust first-quarter results, with gross revenue rising 6.7% year-on-year to S$70.5 million and net property income increasing 8.4% to S$57.6 million. These figures represent 26% of full-year forecasts, indicating solid momentum. The performance was underpinned by exceptional growth in the hospitality segment and declining financing costs due to reduced interest rates and strategic loan repayments.

Hospitality Segment Powers Growth

The hospitality division emerged as the standout performer, with revenue surging 15.1% year-on-year to S$26.8 million and net property income climbing 16.8% to S$24.3 million. Revenue per available room (RevPAR) increased 11.7% to S$277, driven by strong meetings, incentives, conferences and exhibitions pipeline activity and strategic focus on corporate travellers with flexible pricing strategies.

Hilton Orchard achieved 11.2% RevPAR growth to S$277 through improved business traveller segment performance, whilst Crowne Plaza recorded 11.7% RevPAR growth to S$276, benefiting from resilient transient demand and hosting Disney Cruise crew members. Tourist recovery was led by visitors from the United States, Australia and China, though Indonesian demand faced headwinds due to rupiah weakness.

Office Portfolio Maintains Momentum

The Singapore office portfolio sustained 95.2% committed occupancy with 6.0% rental reversion, supported by flight-to-quality trends. With 26.8% of office gross rental income expiring in 2026 at average passing rent of S$9.77 per square foot against market rent of S$12.40 per square foot, mid-to-high single-digit reversion is expected to continue.

Key opportunities include Deloitte’s 150,000 square foot lease at OUE Downtown expiring end-2026, currently contributing approximately 5% of portfolio revenue at sub-S$8 per square foot rent. Additionally, OUE Bayfront received planning approval to convert their level 17 into 22,600 square feet of prime office space, representing an estimated 6% net lettable area increase and potential S$4.3 million annual gross revenue uplift.

Financing Costs Decline Significantly

Interest expenses fell 17.7% to S$17.2 million, with cost of debt dropping 50 basis points year-on-year to 3.7%. This improvement resulted from repaying a S$100 million highest-cost loan and replacing it with lower-cost facilities maturing in 2029. Further relief is anticipated from refinancing the S$150 million medium-term note due in 2026 with facilities of at least five years maturity.

Investment Recommendation

Phillip Securities Research maintains a BUY rating with an unchanged dividend discount model-based target price of S$0.45. The REIT trades at a forward dividend yield of 6.2% and price-to-net asset value of 0.65 times. Upside catalysts include OUE Bayfront chiller space conversion, Deloitte rent reversion to at least S$9 per square foot upon contract renewal, and potential capital redeployment from One Raffles Place divestment to acquire additional stake in Salesforce Tower Sydney.

Frequently Asked Questions

Q: What drove OUE REIT's strong Q1 performance?

A: The results were driven by strong hospitality segment performance and declining financing costs due to reduced interest rates and loan repayments, with gross revenue rising 6.7% and net property income increasing 8.4% year-on-year.

Q: How did the hospitality segment perform in Q1?

A: The hospitality segment delivered exceptional results with revenue increasing 15.1% to S$26.8 million and net property income rising 16.8% to S$24.3 million, whilst RevPAR grew 11.7% to S$277.

Q: What is the outlook for office rental reversions?

A: With 26.8% of office gross rental income expiring in 2026 at average passing rent of S$9.77 per square foot against market rent of S$12.40 per square foot, mid-to-high single-digit reversion is expected to persist.

Q: What are the key upside catalysts for OUE REIT?

A: Key catalysts include conversion of OUE Bayfront chiller space into office space, Deloitte's below-market rent reverting to at least S$9 per square foot if renewed, and potential capital redeployment from One Raffles Place divestment.

Q: How significantly did financing costs decline?

A: Financing costs fell 17.7% to S$17.2 million, with cost of debt dropping 50 basis points year-on-year to 3.7%, mainly due to repaying a S$100 million highest-cost loan and replacing it with lower-cost facilities.

Q: What is Phillip Securities Research's recommendation and target price?

A: Phillip Securities Research maintains a BUY rating with an unchanged dividend discount model-based target price of S$0.45, representing a forward dividend yield of 6.2%.

Q: What impact does the Iran conflict have on OUE REIT?

A: There is limited first-order impact from the ongoing Iran conflict, as the majority of utility costs are on fixed contracts, providing protection against energy price volatility.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.