Company Overview

Prime US REIT is a real estate investment trust focused on office properties across the United States. The REIT manages a diversified portfolio valued at US$1.4 billion, with properties strategically located in key American markets.

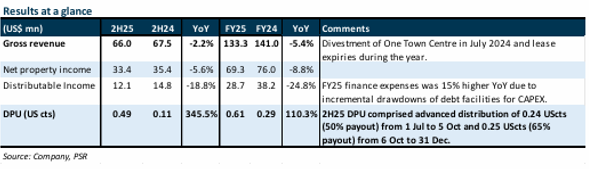

Financial Performance and Distribution Policy

Prime US REIT delivered distribution per unit (DPU) of 0.49 US cents for the second half of FY25 and 0.61 US cents for the full year, meeting expectations and representing 80% and 98% of forecasts respectively. The REIT has significantly enhanced its distribution policy by raising the payout ratio from just 10% in 1H25 to 50% in October 2025 and further to 65% in December 2025.

Despite this improved distribution framework, FY25 revenue and net property income declined 5.4% and 8.8% year-on-year respectively, primarily attributed to the July 2024 divestment of One Town Centre and various lease expiries throughout the period.

The Positive: Strengthening Portfolio Fundamentals

The REIT demonstrated notable progress in its leasing activities and portfolio stability. Management secured 680,000 square feet of new leases during FY25, representing 16% of net lettable area, at an impressive rental reversion of +5.6%. This marked a substantial improvement from FY24’s 592,000 square feet at +1.8% rental reversion, reflecting strengthening leasing momentum.

Portfolio occupancy increased from 80.7% to 82.7% quarter-on-quarter, with management targeting at least 85% occupancy by end-2026. The weighted average lease expiry extended to 5.6 years from 4.4 years previously, significantly enhancing income visibility. Only 7.2% of leases by income require renewal in 2026, providing substantial cash flow certainty.

Portfolio valuations rose 3.5% year-on-year to US$1.4 billion, with 11 of 13 assets posting gains driven by stronger contracted cash flows and 25-50 basis points of cap rate compression, indicating a turnaround in capital values.

The Negative: Selective Property Challenges

Two properties experienced valuation declines due to elevated cap and discount rates. 171 17th Street fell 6% following a comparable sale in May 2025 by a distressed seller. More significantly, Tower I at Emeryville recorded a sharp 48.7% decline after a nearby transaction in September 2025 completed at approximately 10% cap rate, which prompted valuers to increase both cap and discount rates by around 200 basis points for the asset.

Investment Recommendation

Phillip Securities Research maintains a BUY recommendation with a higher target price of US$0.32, increased from US$0.30 previously. The enhanced payout ratio is supported by improving committed occupancy and strong cash flow visibility, as new leases signed in FY24/25 are scheduled to commence cash contributions from 2026 onwards. Trading at 0.42x price-to-net asset value, Prime US REIT offers an attractive entry point with dividend growth potential as their portfolio stabilises.

Frequently Asked Questions

Q: What was Prime US REIT’s distribution performance in FY25?

A: Prime delivered DPU of 0.49 US cents for 2H25 and 0.61 US cents for FY25, representing 80% and 98% of forecasts respectively, supported by a significantly higher payout ratio.

Q: How has the payout ratio changed recently?

A: The payout ratio increased dramatically from 10% in 1H25 to 50% in October 2025 and further to 65% in December 2025, backed by improving cash flow visibility.

Q: What drove the decline in revenue and net property income?

A: FY25 revenue and net property income fell 5.4% and 8.8% year-on-year respectively, primarily due to the July 2024 divestment of One Town Centre and lease expiries during the year.

Q: How did leasing performance improve in FY25?

A: Prime secured 680,000 square feet of leases at +5.6% rental reversion, significantly improved from FY24’s 592,000 square feet at +1.8%, demonstrating strengthening leasing momentum.

Q: What is the occupancy outlook for the portfolio?

A: Portfolio occupancy increased from 80.7% to 82.7% quarter-on-quarter, with management expecting to reach at least 85% by end-2026 through continued active leasing initiatives.

Q: Which properties experienced valuation challenges?

A: Two properties recorded declines: 171 17th Street fell 6% following a distressed comparable sale, whilst Tower I at Emeryville declined 48.7% after a nearby transaction prompted significant cap and discount rate increases.

Q: What is Phillip Securities Research’s investment recommendation?

A: The firm maintains a BUY rating with a raised target price of US$0.32 (from US$0.30), citing the attractive 0.42x P/NAV valuation and dividend growth potential as the portfolio stabilises.

Q: What provides confidence in the enhanced payout ratio sustainability?

A: The higher payout ratio is supported by improving committed occupancy, strong cash flow visibility, and new leases signed in FY24/25 that will commence cash contributions from 2026 onwards.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.