Company Overview

Q&M Dental Group Ltd operates as a dental services provider with a current network of more than 150 standalone clinics in Singapore and Malaysia. The company is positioning itself to become a major dental franchise platform through strategic acquisitions and organic growth initiatives.

Ambitious Acquisition Strategy

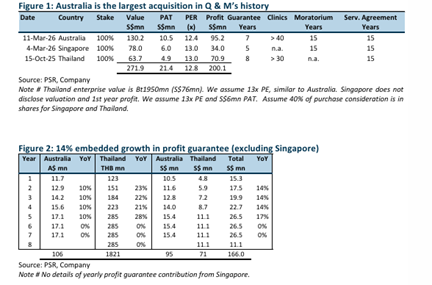

The company has announced three significant proposed acquisitions totalling approximately S$272 million, which could potentially double its earnings upon completion. These acquisitions span across Australia, Singapore, and Thailand, backed by robust profit guarantees totalling S$200 million over five to eight years.

The largest acquisition involves an Australian dental network valued at A$144.5 million (approximately S$130 million), comprising more than 40 clinics and 120 dentists. This will be complemented by additional Singapore clinic acquisitions and a Thai operation focused on cosmetic and aesthetic dentistry with over 30 clinics.

Financing Structure and Growth Projections

The acquisitions will be financed through a combination of cash and shares, following the Australian acquisition template where 40% of the purchase consideration will be satisfied through shares issued at S$0.70. Notably, the structure includes a 15-year moratorium on shares and service agreements to ensure vendor alignment with long-term objectives.

The profit guarantees provide embedded earnings growth of approximately 14% per annum over the next three years. These acquisitions are expected to boost FY26 estimated earnings per share by 80% to 3.5 cents.

Operational Synergies and Network Expansion

The expanded network will create opportunities for revenue and cost synergies, alongside the implementation of best practices in marketing, advanced dentistry, and operations. The company aims to aggressively grow the Australian network towards 400 clinics over five years, whilst targeting 300 dental clinics across Singapore over the same period. The broader network will also serve as a platform for rolling out EM2AI solutions.

Financial Performance and Outlook

FY25 revenue exceeded expectations at 105% with the consolidation of Aoxin Q&M, though net profit came in at 68% due to S$2.4 million in interest expenses and S$2 million in one-off costs. Additional government subsidies for restorative dental procedures introduced in October contributed a 3% boost to Singapore revenue in the second half of FY25.

Phillip Securities Research Recommendation

Phillip Securities Research maintains a BUY recommendation with a raised target price of S$0.71 (previously S$0.545). The fair value post-acquisition is estimated at S$0.95, though a 50% discount has been applied pending completion of the acquisitions. The valuation is pegged at 25x PE FY26, in line with the Singapore healthcare sector.

Frequently Asked Questions

Q: What is the total value of Q&M Dental’s proposed acquisitions?

A: The three proposed acquisitions have an estimated total value of S$272 million, covering dental operations in Australia, Singapore, and Thailand.

Q: How will these acquisitions be financed?

A: The acquisitions will be satisfied through a combination of cash and shares, with 40% of the purchase consideration in shares issued at S$0.70, following the Australian acquisition template.

Q: What are the profit guarantees associated with these acquisitions?

A: The acquisitions are backed by profit guarantees totalling S$200 million over five to eight years, providing embedded earnings growth of approximately 14% per annum for the next three years.

Q: What is Phillip Securities Research’s recommendation and target price?

A: Phillip Securities Research maintains a BUY recommendation with a raised target price of S$0.71, up from the previous target of S$0.545.

Q: How many clinics does Q&M currently operate and what are its expansion plans?

A: Q&M currently operates more than 150 clinics in Singapore and Malaysia and aims to grow towards 300 dental clinics in Singapore and 400 clinics in Australia over the next five years.

Q: What impact will the acquisitions have on earnings?

A: The acquisitions are estimated to boost FY26 earnings per share by 80% to 3.5 cents, with the potential to double the company’s overall earnings upon completion.

Q: What operational benefits are expected from the acquisitions?

A: The expanded network will create opportunities for revenue and cost synergies, implementation of best practices in marketing and operations, and serve as a platform for rolling out EM2AI solutions across the broader clinic network.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.