Company Overview

Shopify Inc. operates as a leading e-commerce platform provider, enabling businesses of all sizes to create and manage online stores. The company serves merchants across various verticals through its subscription solutions and merchant services, including payment processing capabilities that form a core part of its ecosystem.

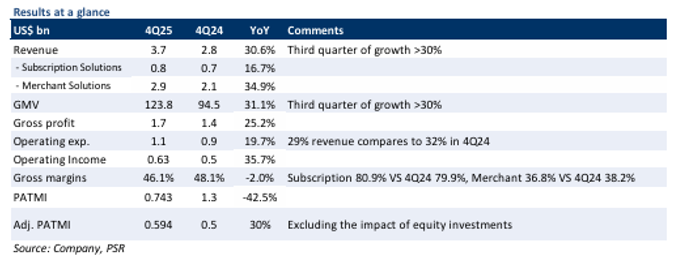

Financial Performance Analysis

Shopify delivered robust fourth-quarter 2025 results with revenue growing 31% year-on-year, marking the third consecutive quarter of growth exceeding 30%. Revenue performance met expectations at 102% of full-year 2025 forecasts, though adjusted profit after tax and minority interests underperformed at 92% of projections. The shortfall was primarily attributed to payment-mix-driven margin pressure, including lower high-margin third-party referral fees and higher PayPal processing costs as more transaction volume flowed through Shopify’s payment infrastructure.

Both business segments contributed to growth, with subscription solutions advancing 17% year-on-year and merchant solutions expanding 35%. However, margins declined by 2% due to a mix shift toward lower-margin payment revenue.

Key Growth Drivers -The Positives

Shopify’s upmarket and global momentum continues to broaden its growth foundation. The company secured notable enterprise clients including GM, Sonos, L’Oréal, Keurig Dr. Pepper, and Amer Sports during the quarter, demonstrating success across diverse verticals. North American revenue remained strong at 28% year-on-year growth, with Shopify now commanding over 14% of US e-commerce market share, up from over 12% in the fourth quarter of 2024.

International expansion accelerated with 36% year-on-year revenue growth, and half of merchants now operating outside North America. Europe showed particular strength with gross merchandise value growing 45% year-on-year. Nearly half of incremental gross merchandise value dollars originated from outside North America during the fourth quarter.

Shopify Plus, the company’s enterprise-level, upmarket segment tailored for high-growth, high-volume merchants continues scaling effectively, accounting for 34% of monthly recurring revenue compared to 33% in the fourth quarter of 2024, with management noting rising average gross merchandise value per Plus merchant.

Shopify’s ecosystem flywheel strategy centres on payments integration and AI-powered commerce capabilities. Shopify Payments penetration increased to 68% of gross merchandise value from 64% previously, processing US$84 billion in the fourth quarter with 38% year-on-year growth. This enhanced checkout conversion rates and repeat purchase behaviour.

The company is expanding demand surfaces through AI-commerce initiatives, including Agentic Storefronts and Universal Commerce Protocol integrations across major AI platforms. AI-originated orders have increased 15-fold since January 2025, positioning Shopify advantageously as transactions continue routing through its checkout and payment infrastructure, creating a structural growth loop where broader discovery leads to higher gross merchandise value, greater payment capture, and deeper ecosystem integration.

Phillip Securities Research Recommendation

Phillip Securities Research has upgraded Shopify from NEUTRAL to BUY rating, raising the target price to US$160 from the previous US$155. The upgrade reflects recent price performance and the company’s strong positioning to capture growth in Agentic Commerce, with analysts maintaining a positive long-term outlook.

Frequently Asked Questions

Q: What is Phillip Securities Research’s current recommendation for Shopify?

A: Phillip Securities Research upgraded Shopify from NEUTRAL to BUY rating with a target price of US$160, increased from the previous US$155.

Q: How did Shopify perform financially in the fourth quarter of 2025?

A: Revenue grew 31% year-on-year, marking the third consecutive quarter of growth exceeding 30%. However, adjusted profit margins declined by 2% due to payment-mix pressures.

Q: What drove the margin pressure in Shopify’s recent results?

A: Margin pressure resulted from lower high-margin third-party referral fees and higher PayPal processing costs as more transaction volume flowed through Shopify’s payment rails, creating a mix shift toward lower-margin payment revenue.

Q: How is Shopify performing in international markets?

A: International revenue grew 36% year-on-year, with half of merchants now outside North America. Europe showed particular strength with gross merchandise value growing 45% year-on-year, and nearly half of incremental gross merchandise value dollars came from outside North America.

Q: What is the significance of Shopify’s AI-commerce initiatives?

A: AI-originated orders increased 15-fold since January 2025 through Agentic Storefronts and Universal Commerce Protocol integrations. This creates a structural growth loop as transactions still route through Shopify’s checkout and payment systems.

Q: How is Shopify’s upmarket strategy progressing?

A: Shopify’s Plus segment accounted for 34% of monthly recurring revenue, up from 33% in the fourth quarter of 2024, with management noting rising average gross merchandise value per Plus merchant and continued enterprise client wins.

Q: What is Shopify’s current market position in US e-commerce?

A: Shopify now commands over 14% of US e-commerce market share, increased from over 12% in the fourth quarter of 2024, demonstrating continued market share gains.

Q: How important are Shopify Payments to the company’s strategy?

A: Shopify Payments penetration increased to 68% of gross merchandise value, processing US$84 billion in the fourth quarter with 38% year-on-year growth, strengthening checkout conversion and repeat purchases while deepening ecosystem integration.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.