Company Overview

SIA Engineering Co. Ltd is a leading aviation maintenance, repair and overhaul (MRO) services provider operating across engine and component maintenance, as well as airframe and line maintenance segments. The company serves the Southeast Asian aviation market through its extensive network of facilities and strategic partnerships.

Strong Financial Performance Drives Rating Upgrade

Phillip Securities Research has upgraded SIA Engineering Co. Ltd to BUY from ACCUMULATE, setting a target price of S$4.06, down from the previous S$4.14 due to share price weakness. The research house rolled forward financials and reduced the price-to-earnings multiple from 26x to 25x to account for heightened sector-wide risks from the US-Iran conflict.

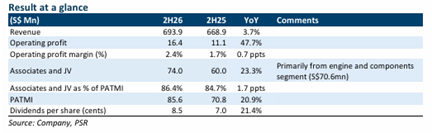

The company delivered robust results for 2H26/FY26, with profit after tax and minority interests (PATMI) rising 20.9%/21.0% year-on-year to S$85.6 million/S$168.9 million, representing 47.8%/94.4% of Phillip Securities’ FY26 estimates. This strong performance was primarily driven by a 22.5% surge in associates and joint venture income during FY26.

Key Positives Supporting Growth Trajectory

The standout performance came from associates and joint venture earnings, which rose 22.5% year-on-year to S$145.3 million. The engine and component segment was the primary driver of this growth, increasing 23.1% to S$139.2 million, supported by higher engine repair deliveries, 20% higher engine inductions, and doubled test facility capacity.

The airframe and line maintenance operations also contributed positively, generating S$6.1 million (+10.9%) supported by stronger heavy check volumes and a 3.3% increase in flights handled at Changi Airport.

Operational Challenges and Gestation Losses

Despite the strong overall performance, gestation losses in subsidiaries persist as a headwind. These losses widened significantly to S$16.1 million in FY26 from S$2.0 million in FY25, weighing on the airframe and line maintenance segment. Base Maintenance Malaysia’s Subang heavy check facility commenced operations in November 2025, with its second hangar not expected to be operational until 2H27. Additionally, TIA Engineering’s Cambodia line maintenance operations began in September 2025, with operations expected to remain below full capacity.

Future Growth Drivers

Looking ahead, Phillip Securities Research identifies several key growth catalysts: SAESL engine capacity is set to increase 33% to 400 engines per annum by 2028, new Pratt & Whitney GTF engine-related coating capabilities in 2027 to capture elevated shop visit volumes, and expansion of landing gear and airframe maintenance capacity across Southeast Asia.

Frequently Asked Questions

Q: What was SIA Engineering's PATMI performance for FY26?

A: PATMI rose 21.0% year-on-year to S$168.9 million in FY26, representing 94.4% of Phillip Securities Research's estimates.

Q: What drove the strong associates and JV performance?

A: Associates and JV income increased 22.5% to S$145.3 million, primarily driven by the engine and component segment which rose 23.1% to S$139.2 million due to higher engine repair deliveries.

Q: What is Phillip Securities' new rating and target price?

A: The research house upgraded SIA Engineering to BUY from ACCUMULATE with a target price of S$4.06, reduced from S$4.14.

Q: What are the main operational challenges facing the company?

A: Gestation losses in subsidiaries widened to S$16.1 million in FY26 from S$2.0 million in FY25, primarily affecting new facilities in Malaysia and Cambodia that are still ramping up operations.

Q: What are the key growth drivers for the future?

A: Future growth will be supported by SAESL engine capacity increasing 33% to 400 engines per annum by 2028, new Pratt & Whitney GTF coating capabilities in 2027, and expanded maintenance capacity across Southeast Asia.

Q: How did the airframe and line maintenance segment perform?

A: The segment contributed S$6.1 million (+10.9%), supported by stronger heavy check volumes and a 3.3% increase in flights handled at Changi Airport.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.