Company Overview

ST Engineering Ltd is a diversified technology and engineering conglomerate operating across three key segments: Commercial Aerospace (CA), Defence & Public Security (DPS), and Urban Solutions & Satcom (USS). The company provides maintenance, repair and overhaul services, manufacturing capabilities, and engineering solutions to both commercial and defence markets globally.

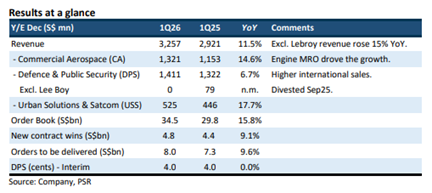

Strong First Quarter Performance

ST Engineering delivered a solid first quarter performance in FY26, with revenue reaching expectations at 24% of full-year forecasts. Revenue grew 15% year-on-year when excluding the divested LeeBoy operations, demonstrating underlying business strength. The company reported that net profit exceeded 15% year-on-year growth, keeping ST Engineering on track to meet its ambitious 2025-29 target of growing earnings 5 percentage points faster than revenue.

Robust Orderbook Growth Driven by Defence Wins

The company’s orderbook surged approximately 16% year-on-year to S$34.5 billion, with defence operations leading the charge in new contract wins. Two significant orders bolstered the portfolio: a S$470 million contract for Qatar land platform maintenance, repair and overhaul services, and a substantial S$600 million deal to supply eight gunboats for the Kuwait Naval Force. These wins highlight ST Engineering’s strong positioning in international defence markets.

Commercial Aerospace Segment Shows Positive Momentum

The Commercial Aerospace division demonstrated continued strength, with revenue expanding 15% year-on-year to S$1.32 billion in the first quarter. Growth was primarily driven by engine MRO services and increased nacelle deliveries. Extended flight times have increased engine life expectancy, consequently boosting MRO requirements. ST Engineering has strengthened its partnership with engine principal CFM-LEAP in Asia, providing enhanced access to spare parts and technical expertise.

Satellite Operations Improving

The Satcom division, operating under the Urban Solutions & Satcom segment, showed promising signs with revenue growing 30% year-on-year in the first quarter. This growth stemmed from increased demand in government and defence sectors. Management has identified planned cost savings of S$50 million to transform the division into profitability.

Investment Outlook

Despite ongoing Middle East conflicts, ST Engineering has experienced no significant project delays or supply chain disruptions. The Middle East can represents less than 3% of total revenue, limiting exposure risks. The company’s largest growth opportunity lies in international defence, with US$11 billion in opportunities to pursue over the next two years. Notably, international defence orders secured this year have already doubled those achieved in 2025, demonstrating accelerating momentum in this key growth area.

Frequently Asked Questions

Q: What is ST Engineering's financial performance target for 2025-29?

A: ST Engineering aims to grow earnings 5 percentage points faster than revenue during the 2025-29 period, and the company is currently on track to meet this target.

Q: How large is ST Engineering's current orderbook?

A: The company's orderbook has grown approximately 16% year-on-year to S$34.5 billion, with defence operations leading the new contract wins.

Q: What were the major defence contracts won recently?

A: ST Engineering secured two significant contracts: S$470 million for Qatar land platform MRO services and S$600 million for eight gunboats for the Kuwait Naval Force.

Q: How is the Commercial Aerospace segment performing?

A: Commercial Aerospace revenue grew 15% year-on-year to S$1.32 billion, driven by engine MRO services and higher nacelle deliveries, supported by extended flight times increasing MRO requirements.

Q: What is the growth outlook for international defence?

A: International defence represents the largest growth opportunity, with US$11 billion in opportunities to pursue over the next two years. International defence orders secured this year have already doubled those from 2025.

Q: How is the Satcom division performing?

A: Satcom revenue grew 30% year-on-year in the first quarter, driven by government and defence sector demand. Management has planned S$50 million in cost savings to turn the division profitable.

Q: What is the analyst recommendation and target price?

A: The analyst maintains a BUY recommendation with an unchanged DCF target price of S$13.00.

Q: Has the Middle East conflict affected ST Engineering's operations?

A: No significant project delays or supply chain disruptions have occurred in the near-term. The Middle East accounts for less than 3% of total revenue, limiting exposure risks.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.