Company Overview

TeleChoice International Ltd is a telecommunications services provider focused on personal communications systems (PCS) and network engineering services. The company operates across Southeast Asia, with significant exposure to Malaysia’s telecommunications market through its partnership with U-Mobile.

Financial Performance Exceeds Expectations

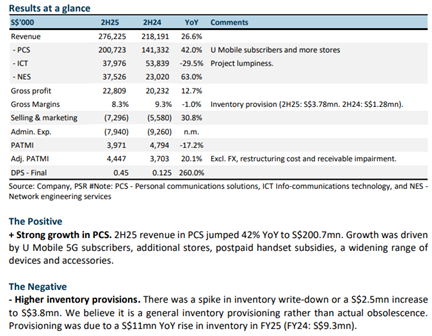

TeleChoice delivered FY25 results that met analyst forecasts, with revenue and profit after tax and minority interests (PATMI) reaching 105% and 103% of expectations respectively. Revenue expanded substantially by 27% year-on-year to S$276 million, primarily supported by U-Mobile 4PL services. However, adjusted PATMI grew at a more modest 20% year-on-year to S$4.4 million due to inventory provisioning impacts. Shareholders benefited from a significant dividend increase, with FY25 dividends more than tripling to 0.45 cents.

Personal Communications System Drives Growth

The personal communications system segment remained the company’s primary growth engine, with revenue surging 42% year-on-year to S$200 million. This impressive growth was fuelled by U-Mobile’s expanding subscriber base and the increasing adoption of higher-value postpaid plans requiring handset subsidies. TeleChoice strategically expanded its retail footprint by increasing outlet numbers, broadening its device portfolio, and introducing additional accessories to capture greater market share.

Challenges and Outlook

Despite the strong revenue performance, TeleChoice faced headwinds from higher inventory provisions. The company experienced a significant spike in inventory write-downs, with provisions increasing by S$2.5 million to S$3.8 million. This provisioning was attributed to a S$11 million year-on-year rise in inventory levels during FY25, compared to S$9.3 million in FY24.

Research Recommendation and Valuation

Phillip Securities Research maintains its BUY recommendation on TeleChoice International, raising the target price to S$0.275 from the previous S$0.215. The firm increased its FY26e PATMI forecast by 13% to S$8.3 million. The valuation is based on a 15x price-to-earnings multiple for FY26e, benchmarked against SGX-listed companies in the system integration and software sectors. The research house noted that growth momentum in PCS remains intact, with network engineering showing signs of recovery through managed services and network buildout projects in Indonesia and Malaysia. Additionally, TeleChoice is evaluating expansion opportunities into higher-growth digital infrastructure segments, including data centres.

Frequently Asked Questions

Q: What were TeleChoice’s key financial results for FY25?

A: TeleChoice achieved revenue of S$276 million, representing 27% year-on-year growth, and adjusted PATMI of S$4.4 million, up 20% year-on-year. Results were within expectations at 105% and 103% of forecasts respectively.

Q: Which business segment drove the strongest growth?

A: The personal communications system (PCS) segment was the key growth driver, with revenue jumping 42% year-on-year to S$200 million, supported by U-Mobile subscriber growth and higher postpaid plans.

Q: What challenges did the company face during FY25?

A: TeleChoice experienced higher inventory provisions, with write-downs increasing by S$2.5 million to S$3.8 million due to a S$11 million year-on-year rise in inventory levels.

Q: What is Phillip Securities Research’s recommendation and target price?

A: Phillip Securities Research maintains a BUY recommendation with a raised target price of S$0.275, up from the previous S$0.215, based on 15x P/E for FY26e.

Q: How did dividends perform in FY25?

A: FY25 dividends more than tripled to 0.45 cents, representing a 260% increase from the previous year’s 0.125 cents.

Q: What expansion opportunities is TeleChoice considering?

A: The company announced it is evaluating expansion into higher-growth segments within digital infrastructure, including data centres, whilst network engineering is recovering through managed services and projects in Indonesia and Malaysia.

Q: What factors contributed to the PCS segment’s strong performance?

A: Growth was driven by U-Mobile 5G subscribers, additional retail stores, postpaid handset subsidies, a widening range of devices, and expanded accessories offerings.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.