Company Overview

United Hampshire US REIT (UHREIT) is a real estate investment trust focused on grocery, necessity retail properties, and self-storage facilities in the United States. Since its IPO in 2020, the REIT has built a diversified portfolio anchored by essential retail tenants, providing defensive characteristics and steady income streams.

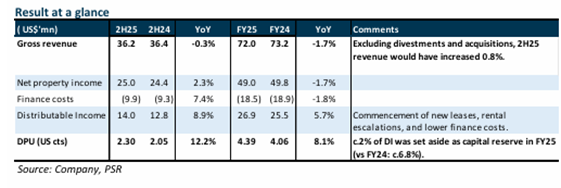

Strong Financial Performance

UHREIT reported robust results for 2H25 and FY25, with distribution per unit (DPU) reaching 2.30 US cents and 4.39 US cents respectively, which represents an impressive year-on-year growth of 12.2% and 8.1%. The performance aligned with expectations, forming 54% and 103% of full-year forecasts. This growth stemmed from new lease commencements, contributions from the newly acquired Dover Marketplace in August 2025, rental escalations on existing leases, and reduced finance costs.

Portfolio Resilience and Valuation Growth

The REIT’s grocery and necessity properties demonstrated exceptional stability with occupancy maintaining a high level of 97.7%, up from 97% in the third quarter. Portfolio valuations increased 3.8% year-on-year on a same-store basis, marking the fifth consecutive year of valuation growth since the company’s public listing. This increase was driven by stronger operating performance and marginal cap rate compression.

Key Strengths Supporting Long-term Growth

UHREIT’s financial position reflects prudent capital management with no refinancing requirements until 2028. The all-in cost of debt has declined from 5.21% in the first quarter to 5.01% in the fourth quarter of 2025. With 76% of debt on fixed rates, further interest savings are anticipated in 2026, with debt costs expected to fall to approximately 4.6%. The company maintains healthy leverage at 38.6% and an interest coverage ratio of 2.4 times.

The portfolio’s stability is underpinned by a weighted average lease expiry of 7.7 years, a 90% tenant retention rate, and minimal leasing risk in 2026, with only 2.9% of grocery and necessity leases expiring.

Operational Challenges

Self-storage properties experienced a seasonal decline in occupancy to 88.7% from 94.9% in the third quarter, attributed to the slower winter leasing period and tenant turnover. However, rental rates continue trending upwards, presenting opportunities to lease vacant units at higher rents during the upcoming spring peak leasing season.

Investment Recommendation

Phillip Securities Research maintains a BUY recommendation with an unchanged target price of US$0.69 based on dividend discount model valuation. UHREIT currently trades at an attractive FY26 dividend yield of 8.4% and price-to-net asset value of 0.76 times.

Frequently Asked Questions

Q: What drove UHREIT’s strong DPU growth in 2H25 and FY25?

A: Growth was driven by new lease commencements, contributions from Dover Marketplace acquired in August 2025, rental escalations on existing leases, and lower finance costs.

Q: How has the portfolio valuation performed since UHREIT’s IPO?

A: Portfolio valuations have grown for five consecutive years since the 2020 IPO, with the latest increase of 3.8% year-on-year driven by stronger operating performance and marginal cap rate compression.

Q: What is the current occupancy rate across different property types?

A: Grocery and necessity properties maintained high occupancy at 97.7%, while self-storage properties saw occupancy decline to 88.7% due to seasonal factors and tenant turnover.

Q: How is UHREIT managing its debt obligations?

A: The company has no refinancing requirements until 2028, with debt costs declining from 5.21% to 5.01% and expected to fall to approximately 4.6% in 2026. Aggregate leverage stands at a healthy 38.6%.

Q: What factors underpin the portfolio’s stability?

A: The portfolio benefits from strong grocery and necessity occupancy of 97.7%, a long weighted average lease expiry of 7.7 years, a 90% tenant retention rate, and minimal leasing risk in 2026 with only 2.9% of leases expiring.

Q: What is Phillip Securities Research’s recommendation and target price?

A: Phillip Securities Research maintains a BUY recommendation with an unchanged target price of US$0.69 based on dividend discount model valuation.

Q: What are the key risks facing the REIT?

A: The main operational challenge is seasonal occupancy decline in self-storage properties during winter months, though this presents opportunities to lease units at higher rents during the spring peak season.

Q: What is the current dividend yield and valuation multiple?

A: UHREIT trades at an attractive FY26 dividend yield of 8.4% and price-to-net asset value of 0.76 times.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.