Company Overview

Wee Hur Holdings Ltd is a Singapore-based company operating across three key business segments: worker dormitory operations, building construction, and property development. The company has established itself as a significant player in Singapore’s infrastructure and accommodation sectors, with substantial dormitory assets and a growing construction order book.

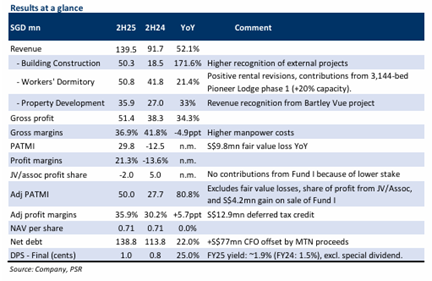

Strong Financial Performance Drives Upgrade

Phillip Securities Research has upgraded Wee Hur Holdings to BUY from NEUTRAL, raising the target price to S$1.08 from S$0.90 previously. This upgrade follows exceptional 2H25 results that significantly exceeded expectations, with revenue and adjusted PATMI reaching 114% and 138% of full-year forecasts respectively.

The company’s adjusted PATMI surged 81% year-on-year to S$50 million in 2H25, driven by multiple growth catalysts across its business segments. The strong performance reflects successful execution of the company’s diversified business model and strategic positioning in Singapore’s infrastructure development.

Worker Dormitory Business Anchors Growth

The worker dormitory segment delivered robust performance, with Tuas View Dormitory achieving 95% occupancy compared to 93% in FY24, alongside positive rental revisions of approximately 5% year-on-year. The segment benefited significantly from Pioneer Lodge’s Phase 1 operations, which added 3,088 beds representing a 20% capacity increase since May 2025. This expansion drove dormitory revenue up 21% year-on-year to S$50.8 million in 2H25.

Pioneer Lodge’s Phase 2, comprising 7,412 beds and representing a 39% capacity increase, received its temporary occupancy permit in 4Q25 and is expected to contribute to occupancy ramp-up in FY26.

Construction Segment Shows Marked Improvement

The building construction segment demonstrated remarkable turnaround, with revenue spiking 172% year-on-year to S$50 million in 2H25. Operating margins improved substantially by 10 percentage points year-on-year to -7% in FY25, compared to -17% in FY24. This improvement was driven by higher recognition of external projects, which now comprise 99% of the company’s S$673 million order book, up from 59% previously. The expanded order book, growing from S$263 million in FY24, is expected to support construction segment growth through 4Q29.

Strategic Portfolio Adjustments

The research firm’s sum-of-the-parts valuation model reflects strategic portfolio changes, including the removal of Mega@Woodlands property development and the addition of Wee Hur’s 50% stake in the S$614 million Upper Thomson Road GLS site. The model also incorporates the company’s estimated 20% stake in the 344-key DoubleTree by Hilton hotel and Fund III, backed by a 708-bed Australia PBSA.

Future Outlook

With major construction projects including Changi Airport Terminal 5 and Marina Bay Sands Integrated Resort on the horizon, analysts expect Wee Hur’s 15,744-bed Tuas View Dormitory lease to be extended beyond November 2026, providing continued revenue visibility for the dormitory business.

Frequently Asked Questions

Q: What is Phillip Securities Research’s current recommendation and target price for Wee Hur Holdings?

A: Phillip Securities Research has upgraded Wee Hur Holdings to BUY from NEUTRAL, with a higher target price of S$1.08, increased from the previous target of S$0.90.

Q: How did Wee Hur’s 2H25 results compare to expectations?

A: The company’s 2H25 revenue and adjusted PATMI significantly exceeded expectations, reaching 114% and 138% of full-year forecasts respectively, with adjusted PATMI surging 81% year-on-year to S$50 million.

Q: What drove the strong performance in the worker dormitory segment?

A: The dormitory segment benefited from Tuas View Dormitory’s improved occupancy rate of 95% and positive rental revisions of about 5% year-on-year, plus contributions from Pioneer Lodge Phase 1’s additional 3,088 beds, driving dormitory revenue up 21% year-on-year to S$50.8 million.

Q: How has the building construction segment’s profitability changed?

A: The building construction segment’s operating margins improved significantly by 10 percentage points year-on-year to -7% in FY25, compared to -17% in FY24, driven by higher recognition of external projects and an expanded order book.

Q: What is the current size and composition of Wee Hur’s construction order book?

A: The company’s construction order book stands at S$673 million, up from S$263 million in FY24, with external projects now comprising 99% of the order book compared to 59% previously. This order book is expected to support growth through 4Q29.

Q: When will Pioneer Lodge Phase 2 contribute to operations?

A: Pioneer Lodge Phase 2, comprising 7,412 beds and representing a 39% capacity increase, received its temporary occupancy permit in 4Q25 and is expected to ramp up occupancy in FY26.

Q: What major construction projects could benefit Wee Hur’s dormitory business?

A: Major upcoming construction projects including Changi Airport Terminal 5 and Marina Bay Sands Integrated Resort are expected to support the extension of Wee Hur’s 15,744-bed Tuas View Dormitory lease beyond November 2026.

Q: What changes were made to the valuation model?

A: The sum-of-the-parts model removed Mega@Woodlands property development and included Wee Hur’s 50% stake in the S$614 million Upper Thomson Road GLS site, plus the company’s estimated 20% stake in the 344-key DoubleTree by Hilton hotel and Fund III backed by a 708-bed Australia PBSA.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.