Company Overview

Yoma Strategic Holdings Ltd is a Myanmar-focused conglomerate with diversified operations spanning property development, motor distribution, financial services through Wave Money, and food & beverage operations. The company serves as a key player in Myanmar’s economic development, capitalising on urbanisation trends and growing consumer demand.

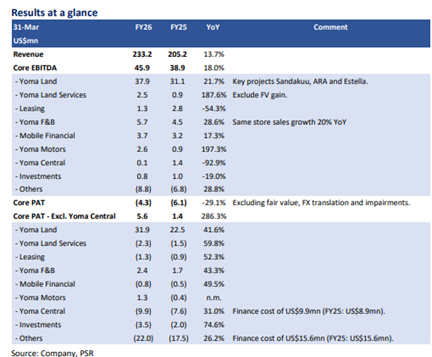

Strong Financial Performance Amid Currency Headwinds

Yoma Strategic delivered robust growth in FY26, with EBITDA rising 18% year-on-year to US$45.9 million despite facing a 5% currency depreciation. This performance demonstrates the company’s operational resilience and ability to generate growth across multiple business segments.

Property development remained as the primary earnings driver, contributing US$38 million with a 22% increase from the previous year. The division’s strength is underpinned by Myanmar’s continued urbanisation and migration patterns, with residential property serving as a preferred store of wealth for local consumers.

Operational Recovery Gaining Momentum

The recovery is notably broadening across all business divisions. Motor distribution has returned to profitability through the strategic restocking of third-party brands, Volkswagen passenger vehicles, and Hino trucks. Passenger vehicle sales surged to 152 units in FY26 from just 7 units in FY25, whilst Hino truck sales more than doubled to 98 units.

The financial services division, Wave Money, is successfully transitioning from reliance on remittance fee towards interest income, with float income jumping approximately 80% in FY26. Meanwhile, the food & beveragesegment continues steady growth through store expansion and pricing power, achieving strong same-store sales growth of 20%.

Challenges and Risk Factors

The company faces ongoing challenges at Yoma Central, a mixed-use development in Yangon, which incurred finance costs of US$10 million in FY26 pending its phased restart. However, this was partially offset by a US$14.7 million fair value gain from rising land prices in central Yangon.

Looking ahead, potential cost pressures from Middle East conflicts may impact operations, although management’s demonstrated ability to implement price increases across all products provides defensive capabilities.

The company maintains a stable financial position, with net debt, excluding cash in trust, declining to US$132 million from US$136 million in FY25, and book value standing at S$0.193 per share.

Frequently Asked Questions

Q: What drove Yoma Strategic's earnings growth in FY26?

A: Property development was the core earnings driver, rising 22% to US$38 million, supported by strong demand from urbanisation and migration trends. All divisions showed recovery, with motor and financial services returning to growth.

Q: How significant is the property development pipeline?

A: The company has an unrecognised revenue backlog of US$90.3 million and an estimated robust pipeline of launches worth US$110 million to –US$120 million for FY27.

Q: What caused the improvement in motor sales?

A: Yoma Motor returned to profitability by restocking third-party brands, Volkswagen passenger vehicles, and Hino trucks. Passenger vehicle sales rose sharply to 152 units from just 7 units in the previous year.

Q: How is Wave Money's business model evolving?

A: The financial services division is transitioning away from remittance fees towards interest income, with float income jumping approximately 80% in FY26.

Q: What are the main risks facing the company?

A: Key challenges include ongoing finance costs of US$10 million at the Yoma Central project and potential cost pressures from Middle East conflicts, although the company has demonstrated pricing power across all products.

Q: What was the impact of currency depreciation?

A: Despite a 5% currency depreciation, the company achieved 18% EBITDA growth, demonstrating operational resilience and the strength of its underlying business performance.

Q: How strong is the food & beverage division's performance?

A: The food & beverage segment delivered steady earnings growth, with strong 20% same-store sales growth of 20% and continued store expansion, supported by the company's ability to implement price increases.

This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst.

Disclaimer

These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products.

Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance.

Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries.

The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries.

Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned.

This advertisement has not been reviewed by the Monetary Authority of Singapore.