Company at a Glance

What the company does:

CITSP is a diversified real estate groups, with operations spanning property development, investment properties and hotel management across key global markets. As of FY25, the group had total assets of S$27bn, with portfolio exposure primarily concentrated in Singapore (41%) and the UK (20%). Business exposure remains largely anchored by property development (39%), investment properties (30%) and hotel operations (25%). The major shareholder is Hong Leong Investment Holdings (18.9%)

Main income source:

CITSP derives earnings from property development, investment properties and hotel operations. In FY25, hotel operations contributed S$1.65bn of revenue, followed by property development (S$1.16bn) and investment properties (S$513mn). While recurring cash flow is primarily supported by the hotel and investment property segments, FY25 earnings growth was driven mainly by stronger profit recognition from Singapore residential properties and capital recycling gains.

What Supports the Credit Profile

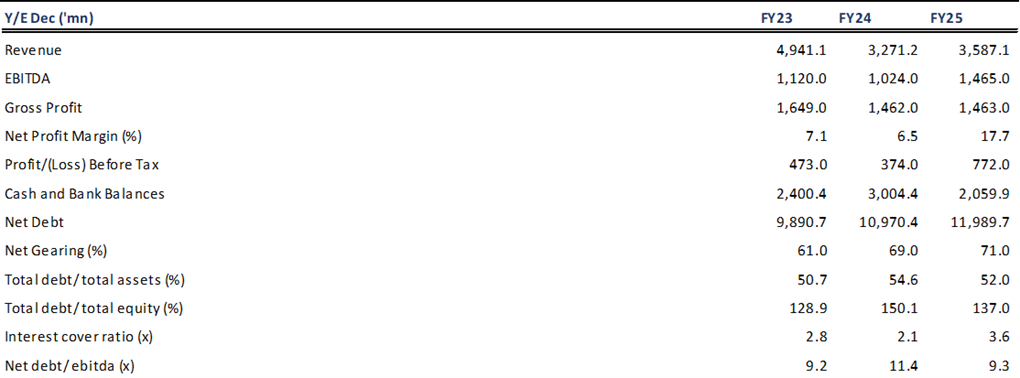

Strong earnings recorded in FY25. PATMI rose sharply by 212.8% YoY to S$629.7mn (FY24: S$201.3mn), while EBITDA increased 43.1% YoY to S$1.47bn from S$1.02bn in FY24. The improvement was driven primarily by stronger profit recognition from Singapore residential developments (The Myst, Norwood Grand and Union Square Residences) and capital recycling gains, particularly the South Beach disposal. Meanwhile, recurring contributions from the hotel and investment property segments remained stable, supported by office and retail occupancy of 96.8% and 97.8%, respectively, as at 31 March 2026. The group also secured approximately 184,000 sq ft of office leasing transactions during Q1 2026 with positive rental reversions.

Residential sales remain resilient. Legacy contracts inherited from former Sembcorp Marine now account for only ~1% of Seatrium’s backlog, as most major lower-margin US projects have largely been delivered. These contracts had previously weighed on earnings through weaker pricing, COVID-related delays and cost overruns that drove sizeable provisions. With legacy exposure now largely phased out, provision risk is expected to decline from FY26 onward, supporting improved earnings stability.

Source: CITSP presentation deck

Source: CITSP presentation deck

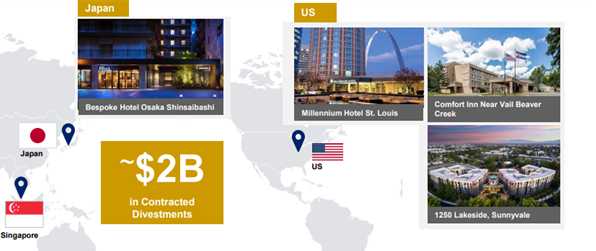

Ongoing divestment plans are expected to strengthen liquidity. CITSP recorded approximately S$2bn of contracted divestments in FY25, exceeding S$1.7bn of investments undertaken during the year, mainly comprising three Singapore GLS acquisitions and a London hotel acquisition. Management continues to position capital recycling as a core strategic priority, with ongoing efforts to monetise mature and non-core assets. This includes the divestment of its legacy UK development platform, which carried an estimated book value of S$800mn as at FY25.

More recently, the group completed the sale of substantially all 27 commercial strata units at Fortune Centre, with the remaining units expected to completed by June 2026. We expect continued asset sales to support liquidity and gradual deleveraging, partially offsetting leverage arising from recent land acquisitions.

Credit metric remains stable. Net gearing increased marginally to 72% as at 1Q 26 from 71% at FY25 following the Tanjong Rhu land acquisition, while liquidity remained robust at S$4.3bn of cash and undrawn committed facilities. We expect leverage to gradually moderate as ongoing divestments are executed in line with management’s active capital recycling strategy. In addition, CITSP’s investment property portfolio carries a fair value of S$13bn, providing monetisation flexibility.

Financial Position

Source: CITSP, Bloomberg

Source: CITSP, Bloomberg

Our Credit View

We maintain a positive view on CITSP’s credit profile, supported by ongoing capital recycling initiatives and resilient Singapore residential demand. Newport Residences has achieved a strong 78% sell-through as at May 2026, while The Myst, Zyon Grand and Norwood Grand are each more than 88% sold. This is expected to support cash flow generation and earnings visibility. While leverage remains elevated following recent land acquisitions, overall credit metrics remain stable and should gradually improve as ongoing divestments are executed.