Company at a Glance

What the company does:

Ho Bee Land is a Singapore-listed real estate group with exposure across investment properties and development projects in Singapore, the United Kingdom, Australia and China. As at FY25, the group had a property portfolio of about S$6.5bn, with asset exposure concentrated in Singapore (46%) and the UK (45%). By sector, the portfolio is mainly commercial, accounting for 79% of assets, followed by residential at 15%.

Main income source:

Ho Bee’s credit profile is primarily supported by recurring rental income from its Singapore and London investment property portfolio, which contributed 55% of FY25 revenue and provides a more stable and higher-margin cash flow base than development property sales.

What Supports the Credit Profile

Softer FY25 revenue, but underlying profit improved

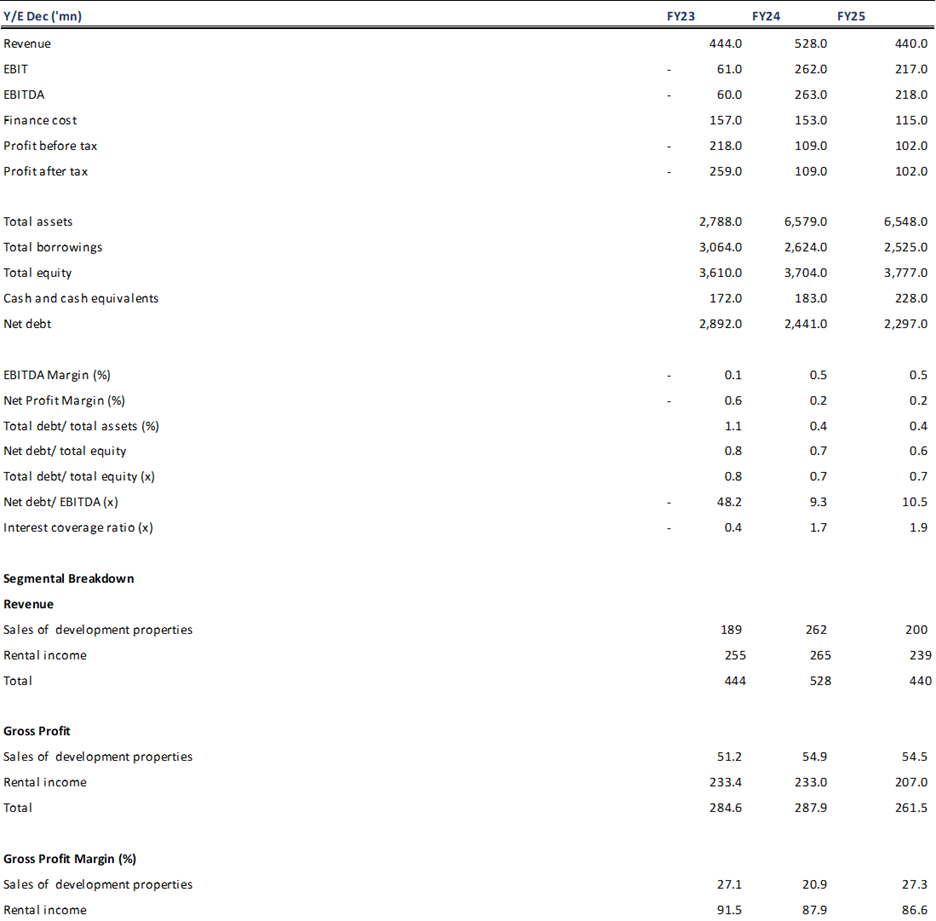

Ho Bee’s FY25 revenue declined 17% YoY to S$440.1mn, driven by lower rental and development revenue. Rental income fell by 10% to S$239.9mn in FY25 (FY24: S$265.7mn) mainly due to Elementum’s reclassification as a jointly controlled asset and planned vacancies at 1 St Martin’s Le Grand ahead of asset enhancement works. Separately, development revenue declined by 24% to S$200.1mn (FY24: 262.3mn) due to fewer settlements from Australia projects. Despite the weaker top line, net profit rose 37% YoY to S$102.4mn after excluding FY24’s one-off Elementum divestment gain, mainly supported by lower financing costs.

Source: Company

Source: Company

Recurring income base remains supported by Singapore and UK investment assets

Ho Bee’s recurring income base remains anchored by Singapore and London investment properties. The Metropolis and Elementum maintained healthy occupancies of above 90% in FY25, while the UK portfolio recorded occupancy of above 95% with positive rental reversion in office assets. Key assets such as The Metropolis, Elementum, Ropemaker Place and The Scalpel reported FY25 occupancy rates of 94%, 93%, 100% and 96%, respectively.

Credit metrics improved on lower borrowings and reduced gearing

Ho Bee’s balance sheet improved in FY25. Net gearing declined to 0.61x as at end-FY25 from 0.66x in FY24. Ho Bee disclosed >S$200mn cash and >S$400mn undrawn committed facilities, which broadly cover the S$492mn debt maturity in 2026.

Improving UK financing conditions is credit supportive

Management disclosed that banks are offering UK loan margins at sub-2%, which we view as a positive signal that lenders remain comfortable with the quality and bankability of Ho Bee’s London assets. Together with the decline in SONIA from peak levels, this should lower all-in refinancing costs and ease pressure on interest expense. Management also indicated that a 25–50 bps cap rate movement remains manageable, suggesting a sufficient valuation buffer against moderate yield expansion.

Key Assets and Development Pipeline

| Category | Asset / Project | Country/ City | Key Details |

| Investment Asset | The Metropolis | Singapore | FY25 occupancy 94% |

| Investment Asset | Elementum | Singapore | FY25 occupancy 93%; jointly controlled asset after 49% stake sale |

| Investment Asset | The Scalpel | UK / London | FY25 occupancy 96% |

| Investment Asset | Ropemaker Place | UK / London | FY25 occupancy 100%; freehold asset |

| Investment Asset | 1 St Martin’s Le Grand | UK / London | Planning permission secured in mid-2025; under redevelopment |

| Investment Asset | 67 Lombard Street | UK / London | Planned asset enhancement works |

| Development Project | Elimbah, Pumicestone Road & Clinker Road | Australia/ Queensland | ~1,400 residential lots and 64 industrial lots; planned launch in 2027 |

| Development Project | Donnybrook/ Larkwood | Australia/ Victoria | 111 residential lots; planned launch in 2026 |

| Development Project | Batesford, Ballan Road | Australia/ Victoria | ~374 residential lots; planning phase |

Main Areas to Monitor:

Key risks to monitor include the S$1.05bn debt maturity in 2028, execution timeline for asset enhancement works at 1 St Martin’s Le Grand and 67 Lombard Street, and settlement momentum from Australia projects. While AEI may create near-term rental drag, successful execution should improve asset quality and rental potential over the medium term.

Financial Position

Source: Company

Source: Company

Our Credit View

We are positive on Ho Bee’s credit profile, supported by improved gearing metrics and recurring rental income from its Singapore and London assets. Rental income remained the key revenue contributor in FY25 and is a higher-margin, more stable source of cash flow than development sales. While asset enhancement works at 1 St Martin’s Le Grand and 67 Lombard Street may create some near-term rental drag, these initiatives should enhance asset quality and rental potential over the medium term. Improving UK financing conditions should also help lower funding cost pressure going forward. Near-term debt maturities of S$492mn in 2026 are covered by S$400mn undrawn facilities and S$200mn cash.

Bonds Available

Source: Company

Source: Company

* For bond pricing and further information on available offerings, please contact bonds@phillip.com.sg

Relative Value

Source: Bloomberg

Source: Bloomberg

HOBEE 2031 offers better relative value on the issuer curve, with a 29bps pickup over HOBEE 2029 for a two-year tenor extension. Given Ho Bee’s improving leverage, lower borrowings and adequate liquidity, we think the additional spread is reasonable compensation for the longer tenor.

Against peers, Ho Bee trades around 48bps wider than Wing Tai’s 2032s (102bps). which we believe reflects its higher leverage. However, we think that Ho Bee’s improving leverage, lower borrowings and recurring rental income base will support potential spread compression over time. Overall, we view HOBEE 2029 as fair, and HOBEE 2031 as relatively more attractive.