Company at a Glance

What the company does:

Genting Berhad is a diversified gaming, hospitality and leisure group with operations across Malaysia, Singapore, the UK, the US, Egypt and the Bahamas. Key assets include Resorts World Genting (“RWG”), Resorts World Sentosa (“RWS”), Resorts World Las Vegas (“RWLV”), Resorts World New York City (“RWNYC”), Resorts World Bimini (“RWB”) and a portfolio of casinos in the UK and Egypt. Beyond gaming and integrated resorts, the group also operates oil palm plantations, power generation assets and oil & gas assets.

Major Shareholders: Kien Huat Realty Sdn Berhad (43.8%), a prominent Malaysian investment holding company. It primarily functions as the private investment and wealth vehicle for the founding Lim family of the Genting Group.

Main income source:

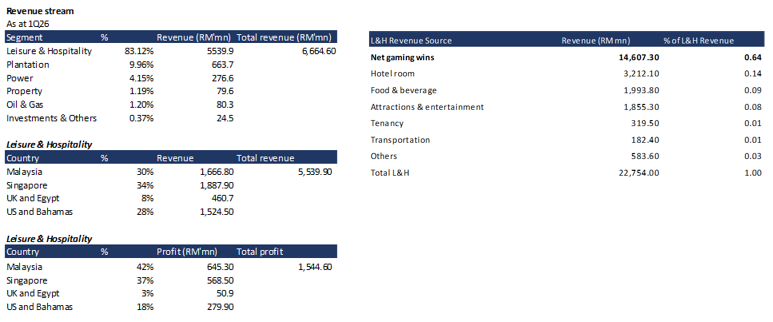

Leisure & hospitality remains Genting’s core earnings driver, contributing 83.12% of FY25 revenue, followed by plantations at 9.96%. Malaysia and Singapore remain the group’s key operating markets and primary contributors to earnings and cash flow generation.

What Supports the Credit Profile

EBITDA weakened despite revenue growth

1Q26 revenue +2% YoY to RM6.7bn, supported by stronger contributions from the US & Bahamas and Malaysia operations. However, adjusted EBITDA declined 8% YoY to RM1.83bn as higher payroll and operating costs, RWS transformation spending and RWNYC transition-related expenses more than offset revenue growth. A stronger RM against USD, SGD and GBP also reduced the translation of earnings from overseas operations.

Source: Resort World Las Vegas

Source: Resort World Las Vegas

RWLV shows signs of recovery

RWLV benefited from stronger convention-driven demand following the expansion of the Las Vegas Convention Centre, with hotel occupancy improving to 91.5% from 82.3% and ADR increasing to USD287 from USD274.

Source: RWS

Source: RWS

Singapore remains the key earnings watchpoint

Singapore remained the largest contributor to leisure & hospitality revenue at 34%, but profit declined 29% YoY to RM569mn. While non-gaming revenue improved by 8% YoY due to stronger visitation to Universal Studios Singapore and the Singapore Oceanarium, gaming revenue remained softer, and earnings continued to be diluted by redevelopment spending and elevated operating costs. Given RWS’s scale within the group, recovery in Singapore profitability remains a key driver of future EBITDA growth.

Earnings pressure weakened credit metrics despite stable debt levels

Net Debt/EBITDA increased to 15.1x from 12.2x, while EBITDA/Interest declined to 3.4x from 4.0x. The deterioration was driven by lower EBITDA, given higher operating costs, RWS transformation spending, RWNYC transition-related expenses and foreign exchange translation headwinds. While leverage remains elevated, the group retains a sizeable liquidity buffer of RM17.4bn.

Regulatory risk remains manageable.

RWG remains a strategically important tourism asset in Malaysia, attracting 28.6 million visitors and supporting more than 11,500 jobs in FY25. Notably, Genting Malaysia’s effective tax rate stood at 31.9% in FY25, well above Malaysia’s standard corporate tax rate of 24%. Given its significant contribution to tourism, employment and government revenue, we view materially disruptive regulatory actions as unlikely.

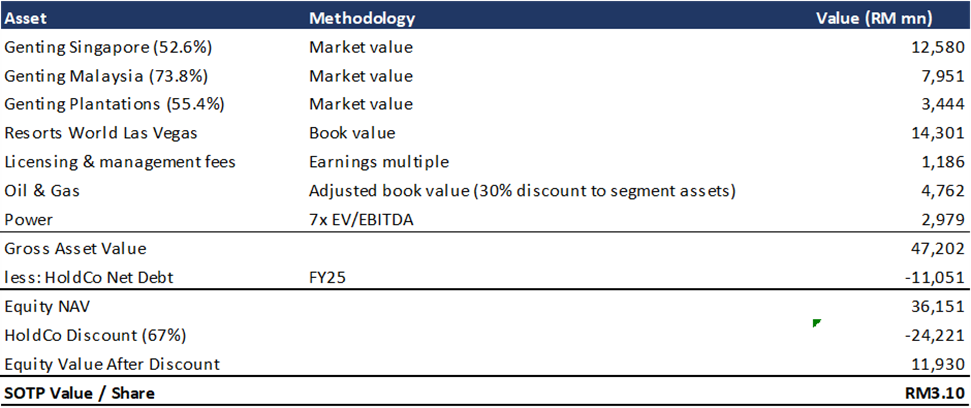

Sum-of-Parts Valuations

Financial Overview

Genting Bond Opportunities

Our Credit View

We maintain a neutral view on Genting Berhad’s credit profile. While the group continues to benefit from sizeable regional gaming assets and diversified geographical exposure, leverage remains elevated, and earnings recovery has been uneven across key operating segments. Near-term credit performance remains highly dependent on the execution of recovery at RWS.