DAILY MORNING NOTE | 10 February 2025

Recent Podcasts:

SGX– Dividends disappoint despite earnings surge

Tesla Inc. – Auto sales, margins and ASPs decline

Apple Inc. – All according to plan

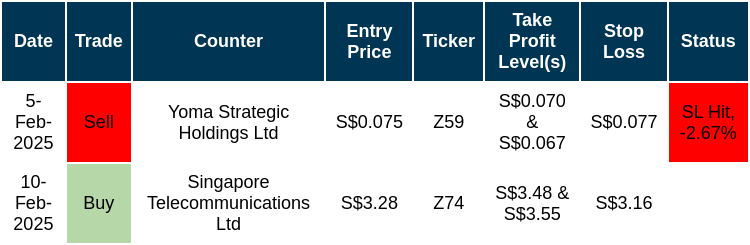

Trade Initiated in Past Week

Week 7 equity strategy: It is a daily whiplash of tariff news from the US. Tariffs on Canada and Mexico have now been postponed for a month. The 10% tariff on China was effective 4 February. After a temporary suspension of accepting parcels from China and Hong Kong, the de minimis exemption (small shipments less than $800 avoid import taxes) remains for now. Shein and Temu accounted for around 30% of the 1bn shipments into the US under de minimis. SATS would have been the most impacted as the US accounts for 30% of revenue.

The threat of tariffs on SE Asia is a clear and present danger. Trump spoke of reciprocal tariffs by early next week on countries with existing tariffs on U.S. goods. Even Japan may not be immune. The most optimistic scenario will be the tariffs are up for negotiation. US Treasury Secretary Scott Bessent said, “The tariff gun will always be loaded and on the table but rarely discharged”. We are not so optimistic. To shelter gain from tariff threats, we believe sectors in Singapore with positive momentum are construction, capital markets, property, power and telco.

Construction is on a multi-year growth expansion, following the 30% rise in 2024 to a record S$44bn. Capital markets will benefit from the surge in financial volatility. SGX is operationally leveraged to the rise in trading volumes. Bank see trading income gains from forex hedging and equity volatility. The property sector is enjoying a surge in demand from delayed new launches and rising HDB prices supporting upgrading. Singapore’s electricity demand is expected to climb from 1.4% CAGR (2018-23) to 4-6% by 2030. Keppel Ltd and SembCorp Industries new hydrogen-ready and more efficient power plants will be the beneficiaries. The 113% YoY jump in Bharti Airtel earnings will be supportive for Singtel.

On SingPost, once the Australia Foreign Investment Review Board (FIRB) approval is received, an EGM is expected in March to approve the sale of its Australian business (FMH). FMH’s offer was attractive at approx. S$900mn cash after SingPost injecting only S$90mn in equity. SingPost’s 4x gearing was too high and to grow FMH, SingPost needed more equity. Meanwhile, the sale of SingPost Centre is still pending HDB approval. Operationally, market conditions are softening and employee retention could be an issue. With a net gain of S$312mn, if we assume 50% is paid out, it implies a special dividend of 7 cents. Any announcement of the special dividend will likely be in May, after the full-year results. We think there is deep value considering SingPost Centre alone is worth S$1bn (or 45 cents). But SingPost may not have the urgency to sell because the balance sheet will be in net cash post-FMH. News on the FIRB/EGM approval and special dividend should drive the share price higher. But we are wary of holding the share price post-special dividends, where it may merely adjust downwards at a similar level because clarity over the core business will be unclear until the postal review is completed.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

Singapore shares rose on Friday (Feb 7), ahead of closely-watched United States employment data that would provide investors a gauge of the US Federal Reserve’s interest rate outlook. The benchmark, Singapore’s blue-chip barometer, rose 31 points or 0.8 per cent to 3,861.42. However, compared to last Friday’s close, the index’s performance was relatively flat, up only 0.1 per cent over the week.

Similar disappointments from Microsoft and Alphabet earlier in the week fuelled suspicions the megacap tech and tech-adjacent stocks are losing momentum.The Dow Jones Industrial Average fell 444.23 points, or 1 per cent, to 44,303.4, the S&P 500 fell 57.58 points, or 1 per cent, to 6,025.99 and the Nasdaq Composite fell 268.59 points, or 1.4 per cent, to 19,523.4.

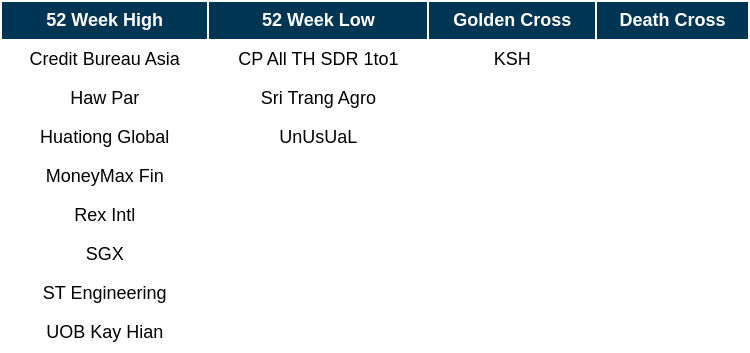

Singapore Technical Highlights

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

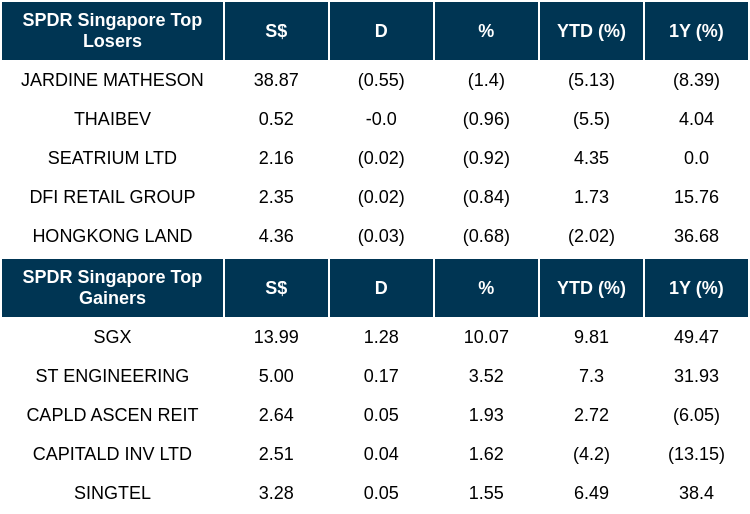

TOP 5 GAINERS & LOSERS

Events Of The Week

SG

DBS’ 4Q2024 adjusted earnings of S$2.52bn were in line with our estimates, with FY24 adjusted earnings at 100% of our FY24e forecast. 4Q24 DPS raised 22% YoY to 60 cents, full-year FY24 dividends at S$2.22 (+27% YoY). Highlights include higher net interest income of S$3.73bn (+9% YoY) as net interest margin rose to 2.15% (+2bps YoY). Fee income rose 12% YoY from continued growth in wealth management and cards fees. Credit costs rose by 9bps YoY to 20bps as SPs rose 65% YoY to S$229mn. DBS has provided FY25e guidance of PATMI growth to dip YoY due to higher taxes, PBT to be flat YoY, NII slightly higher YoY based on two rate cuts in 2H25, high single digit growth in commercial book non-interest income, cost-to-income ratio around the low-40% range and credit cost at around 17-20bps with potential for GP writebacks. Additionally, DBS will be returning additional capital in the form of 15cents dividends per quarter in 2025, with quarterly ordinary dividends at 60cents, bringing FY25 dividends to S$3.00 (+35% YoY).

Real estate investment trusts with retail assets in Singapore (S-Reits) continued to post strong committed occupancy and positive rental reversions in their latest reporting period ended December.

Frasers Property registered S$1 billion in pre-sold revenue across Singapore, Australia, Thailand and China as at Dec 31, 2024, its business update on Friday (Feb 7) showed.

GuocoLand’s top bid of S$627.8 million for River Valley Green (Parcel B) works out to S$1,420 per square foot per plot ratio (psf ppr). This is higher than the S$1,150 psf ppr to S$1,350 psf ppr. The total of five bids received for the plot is also higher than expectations of up to three bids.

SPH Media is spending a total of S$3 million in monthly subsidies this financial year to support doorstep delivery of newspapers, SPH Media chief executive Chan Yeng Kit said on Friday (Feb 7).

US

Oil prices finished with daily gains on Friday (Feb 7) after new sanctions were imposed on Iran’s crude exports, but prices were down for the week as investors worried about US President Donald Trump’s renewed trade war on China and threats of tariffs on other countries.

BP’s dramatic under-performance compared with other oil majors has reached a crunch point – a looming showdown with one of the world’s most aggressive activist investors.

Hutchison Port Holding Trust (HPH Trust : NS8U -2.48%) posted a distribution per unit (DPU) of HK$0.072 for the second half of the year ended Dec 31, 2024, down 6.5 per cent from HK$0.077 in the corresponding year-ago period, said its trustee-manager in a bourse filing on Friday (Feb 7).

Tesla shares tumbled about 11 per cent this week, weighed down by shockingly bad sales reports from around the world. In Germany, sales plunged last month to the lowest since 2021, and they tumbled in France and the UK as well. The news from China, one of Tesla’s biggest markets, is also bleak. Deliveries fell 11.5 per cent year over year – while the shares of Chinese competitor BYD Co notched their best week since 2020 as investors cheered an update to its smart-driving technology.

France is set to announce a total of 109 billion euros (S$152 billion) in investment in artificial intelligence (AI) projects in the country by companies, funds and other sources over the coming years, President Emmanuel Macron said on the eve of a two-day AI summit in Paris.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, PSR

RESEARCH REPORTS

Suntec REIT – Resilient Singapore performance sustained

Recommendation: ACCUMULATE (Maintained), Last Done: S$1.17 Target price: TP: S$ 1.33 , Analyst: Liu Miaomiao

- Gross revenue for FY24 inched up by 0.2% YoY to S$463.6mn, underperforming our forecast at 93% of full-year estimates. The improvement was supported by strong rental reversions of 22.9% for retail and 10.6% for office spaces.

- NPI slipped by 0.8% YoY to S$310.8mn due to the absence of a property tax refund, in line with our forecast and forming 100% of the FY24 estimate. DPU plummeted by 13.2% YoY to 6.19 cents, driven by higher financing costs and the exhaustion of the S$23mn capital top-up. FY24 DPU stands at 6.19 cents, which is within our expectations, at 100% of the full-year forecast.

- SUN successfully divested S$58.3mn of strata units at a price 24% above book value, reflecting the underlying value of the assets. However, it fell short of its FY24 divestment target of S$100mn. We have lowered our FY25e-26e DPU forecasts by 8%/3%, respectively, after factoring in a decelerated decline in interest rate. We maintain our ACCUMULATE rating with a lower DDM-TP of S$1.33 (prev: S$1.36) and FY25e/26e DPU of 6.10/6.48 cents. While topline growth is hobbled by overseas performance, FY25e earnings are likely supported by Singapore’s sturdier office rental reversion at high-single-digit levels and retail at the low teens.

NikkoAM-StraitsTrading Asia ex Japan REIT ETF – Dividend steady despite price drop

Recommendation: ACCUMULATE (Maintained); TP: SGD$0.82 (prev: SGD$0.845); Analyst: Helena Wang

- We value NikkoAM-StraitsTrading Asia ex Japan REIT ETF (AXJREITS) using a combination of historical dividend yield spread and price-to-book ratios. The prices are S$0.80 and S$0.84, using these two valuation methods. Applying equal weightage to both valuations, we raise our target price to S$0.82 (previously S$0.845). We maintain our ACCUMULATE recommendation.

- There were no new additions or removals during the period. AXJREITS remains well-diversified across eight different sectors, with the largest sector being retail (increases from 37.1% to 38.4%).

- Unlike Lion-Phillip S-REIT ETF (SREITS) and the CSOP iEdge S-REIT Leaders Index ETF (SRT), which saw a decline in DPU, AXJREITs’ DPU remained stable at 4.6 cents, likely due to its broader Asian market exposure. However, its price performance (-2.08% YoY) lagged due to HK REIT exposure (Hang Seng REIT Index: -14% YoY vs. Singapore REIT Index: -6% YoY). We expected an improvement in DPU following the Federal Reserve’s rate cut, but the effect seems delayed due to most loans being on fixed rates. We expect a 1% improvement in the ETF’s DPU.

Amazon.com Inc. – Strong results yet soft guidance

Recommendation : ACCUMULATE (Downgraded); TP: US$270.00, Last Close: US$229.15; Analyst: Helena Wang

- 4Q24 revenue was in line with expectations. PATMI outperformed due to increasing operating leverage and cost discipline (3.1% YoY higher operating margins). FY24 Revenue/PATMI was at 100%/112% of our FY24e forecasts.

- The primary revenue driver was AWS (+19% YoY). AWS operating margin rose 7.3% YoY to 36.9%, driven by cost control and an extended server lifespan (contributed to a 200bps expansion).

- We roll over another year of valuations. We decrease FY25e revenue and PATMI by 1% to reflect the leap-year effect, decrease in the useful life of services and increase in the useful life of heavy equipment. Due to recent share price strength, we downgrade our recommendation from BUY to ACCUMULATE and raise our DCF target price to US$270 (prev. US$240). We believe AMZN is well-positioned in generative AI and should benefit from cloud migration as it is still in early stage.

Singapore Telecommunications Ltd (SGX: Z74)

Analyst: Zane Aw

(Current Price: S$3.28) – TECHNICAL BUY

Buy price: S$3.28 Stop loss: S$3.16 (-3.66%)

Take profit 1: S$3.48 (+6.10%) Take profit 2: S$3.55 (+8.23%)

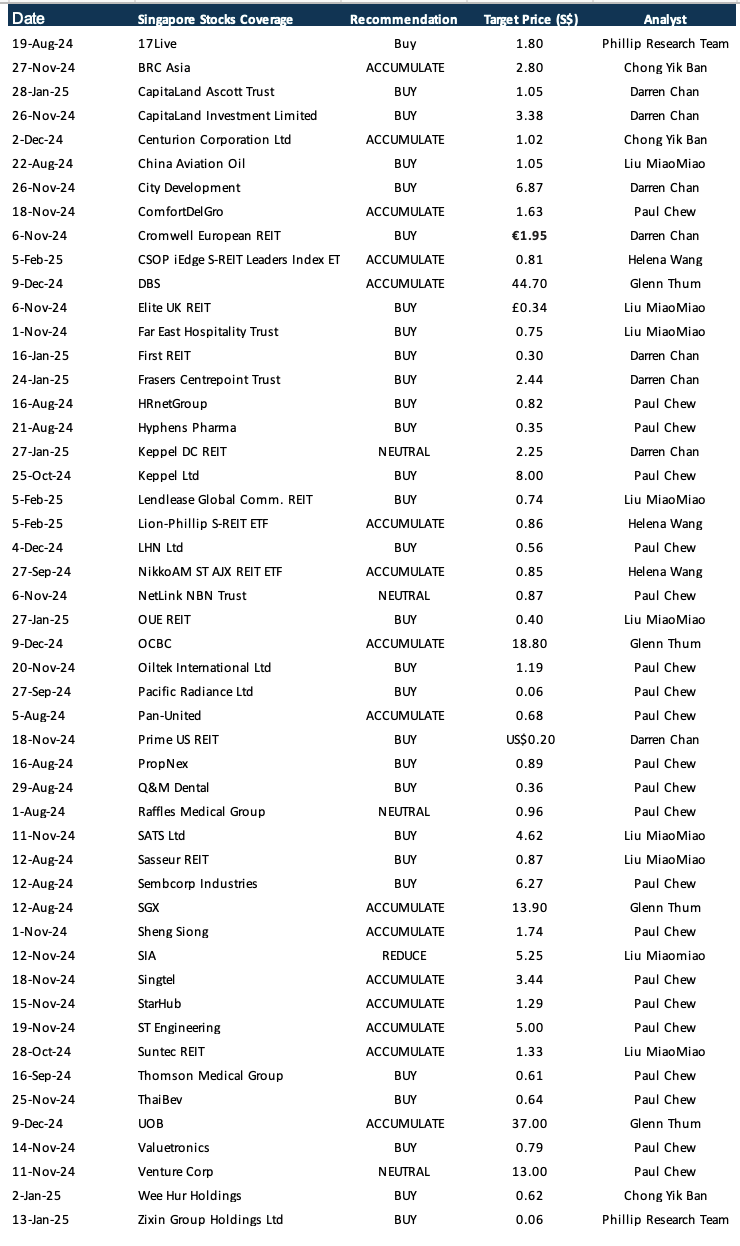

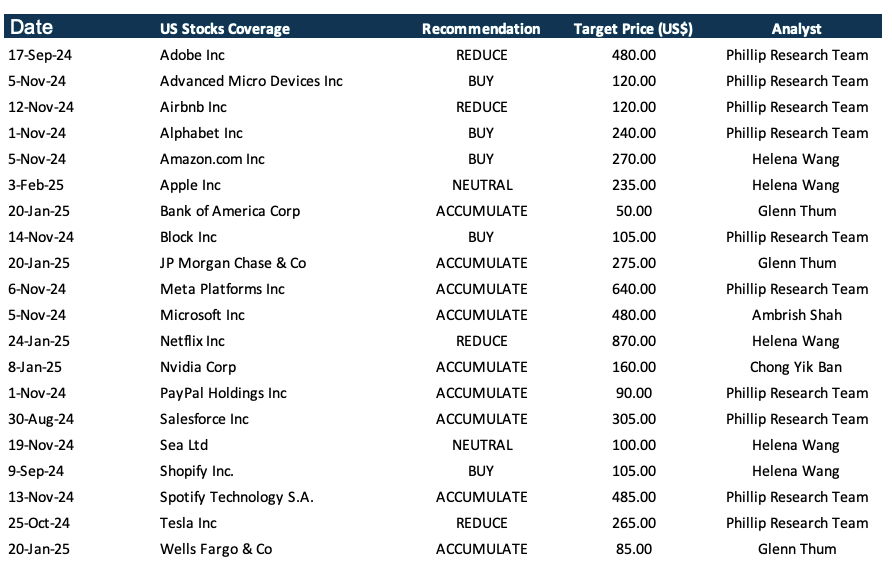

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by CapitaLand India Trust (CLINT)

Date & Time: 11 February 25 | 12PM-1PM

Register: poems-20250211-111265

Corporate Insights by Elite UK REIT

Date & Time: 13 February 25 | 12PM-1PM

Register: poems-20250213-111347

Corporate Insights by Manulife US REIT (MUST) [NEW]

Date & Time: 21 February 25 | 12PM-1PM

Register: poems-20250221-111618

Corporate Insights by Prime US REIT

Date & Time: 25 February 25 | 12PM-1PM

Register: poems-20250225-111267

Corporate Insights by IREIT Global

Date & Time: 27 February 25 | 12PM-1PM

Register: poems-20250227-110518

Corporate Insights by SunCar Technology Group Inc.

Date & Time: 5 March 25 | 12PM-1PM

Register: poems-20250305-110131

Corporate Insights by APAC Realty [NEW]

Date & Time: 7 March 25 | 12PM-1PM

Register: poems-20250307-111928

POEMS Podcast:

Research Videos

Weekly Market Outlook: Apple Inc., CLAS, Technical Analysis, SG Weekly & More!

Date: 3 February 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials