News & Research

Hear from the Experts

Market Overview

*15mins delayed

| 7 August 2026

Recent Podcasts:

Apple Inc. – Supply constraints and rising memory weigh on near term

Amazon.com Inc. -AWS growth begins to justify CapEx bet

Microsoft Corp – Efficiency gains led Azure acceleration

Singapore stocks ended higher on Thursday, with the Benchmark Index gaining 1% or 57.62 points to finish at 5,638.99. Across the broader market, gainers trailed losers 239 to 338.

US stocks finished the trading session lower on Thursday, with the Dow Jones Industrial Average falling 464.02 points, or 0.85%, to 53,885.10, the S&P 500 losing 13.52 points, or 0.18%, to 7,710.03 and the Nasdaq Composite losing 15.09 points, or 0.06%, to 26,348.35.

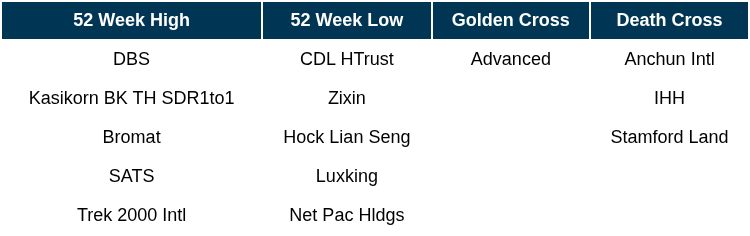

Singapore Technical Highlights

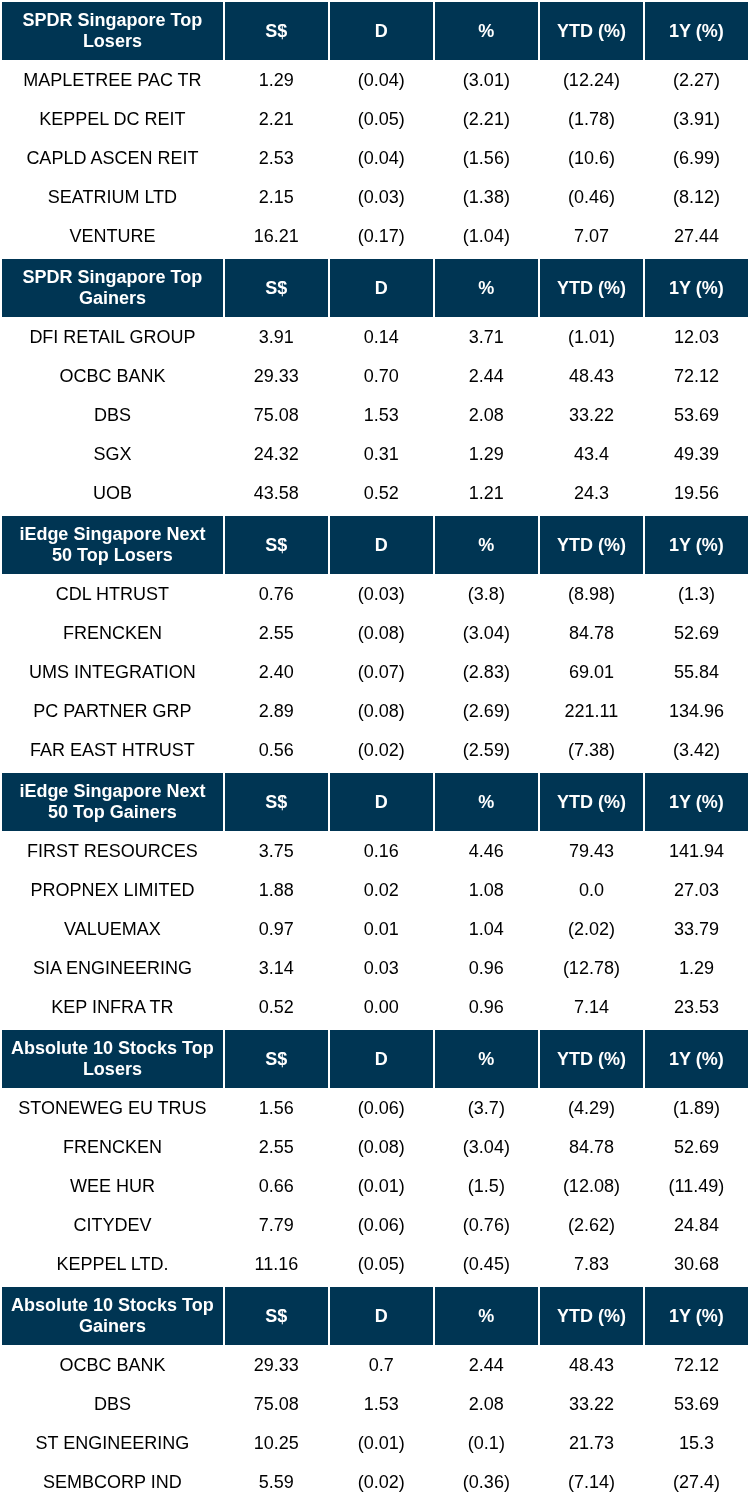

TOP 5 GAINERS & LOSERS

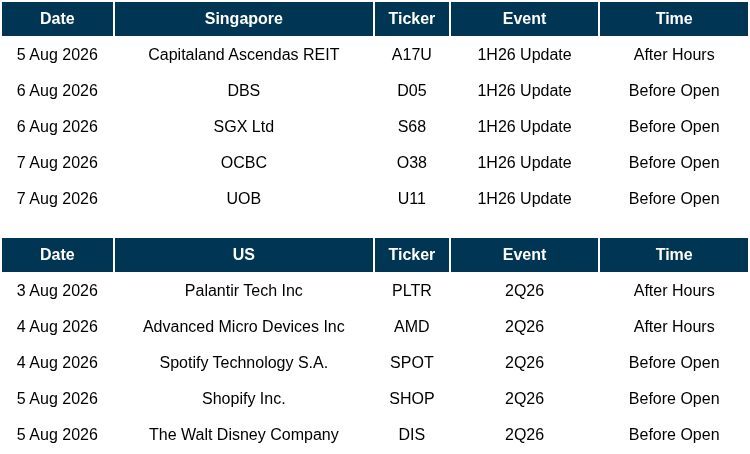

EVENTS OF THE WEEK

SG

UOB’s 2Q26 earnings of S$1,478mn (+10% YoY) were above our estimates, with 1H26 at 53% of our FY26e forecast. NII declined 2% YoY to S$2,297mn as 5% loan growth was outweighed by 17bps NIM compression to 1.74%. NIM also weakened QoQ, down 8bps (1Q26: -2bps) and the steepest among peers (DBS -2bps, OCBC -6bps), as the funding cost tailwind that cushioned 1Q26 faded to -1bp against -5bps of asset repricing. Fee income of S$665mn rose 5% YoY on record wealth fees of S$243mn (+29% YoY), while trading and investment income eased to S$379mn (-8% YoY). Allowances of S$211mn (-24% YoY) took total credit costs to 28bps, within FY26 guidance of 25-30bps. NPL ratio rose to 1.6% on the downgrade of one Greater China real estate account, with Greater China NPL jumping to 4.8% (1Q26: 3.5%) and coverage there falling to 42%. Interim DPS of 88 cents at ~50% payout. Management held FY26 NIM guidance at 1.75-1.80% despite the 2Q exit below range but cut fee income growth guidance to low-single-digit (from high-single-digit).

OCBC’s 2Q26 earnings of S$2.22bn (+22% YoY) were ahead of our estimates, with 1H26 at 53% of our FY26e forecast. NII fell 1% YoY to S$2.26bn as NIM compressed 22bps YoY to 1.70%, with the QoQ decline narrowing to 6bps from 10bps in 1Q26 and no longer the steepest among peers (UOB -8bps, DBS -2bps QoQ). The standout was again non-interest income at a record S$1.91bn (+51% YoY): fee income rose 28% YoY led by record WM fees of S$470mn (+44% YoY), trading income surged 85% YoY to a record S$695mn on record customer flow income, and insurance income rose 68% YoY. Banking WM AUM rose 13% YoY to a record S$350bn. CIR improved to 37.8% (2Q25: 39.1%). Allowances of S$156mn (+36% YoY, -28% QoQ) included S$34mn for non-impaired assets carrying overlays for Indonesian macro uncertainty; NPL stable at 0.9% for the ninth consecutive quarter, NPA coverage 163%. Interim DPS of 47 cents was raised 15% YoY at a 50% payout. Management raised FY26 loan growth guidance to high-single to low-double-digit and reaffirmed the S$2.5bn capital return by FY26.

Glenn Thum

Research Manager

glennthumjc@phillip.com.sg

Elite UK REIT posted 1H26 DPU of 1.55 pence, up 0.6% YoY, with distributable income up 3.6% to £10.1mn and adjusted NPI up 5% to £18.0mn after normalising for one-off items.

Ouhua Energy Holdings expects to swing to a net profit for 1H26 from a loss from a year earlier, driven by higher LPG prices following Middle East tensions and the Strait of Hormuz closure.

Far East Orchard‘s 1H26 revenue more than doubled YoY to S$248.5mn, driven by the consolidation of UK PBSA operator HFS and property sales including Westminster Fire Station.

Yangzijiang Shipbuilding‘s 1H26 net profit rose 28.4% to 5.4bn yuan (US$800mn), with revenue up 36.2% to 17.5bn yuan, driven by higher-margin LNG and ethane carriers.

Centurion Accommodation Reit posted 1H26 DPU of S$0.03499, beating its IPO forecast by 9.6%, with revenue up 5.1% to S$108.9mn and NPI up 4.3% to S$78.4mn on stronger PBWA rental rates and bed sales.

JustCo narrowed its 1H26 net loss 52% to US$839,000 in its first results since its May IPO, with revenue up 24% to US$80.8mn on higher revenue per workstation and network expansion.

SGX posted a FY26 adjusted net profit of S$759.5mn, up 24.6% YoY, led by equities revenue jumping to S$502.9mn from S$392.7mn on a 34.9% rise in securities daily average value.

Venture Corporation‘s 1H26 net profit rose 5.6% YoY to S$119.3mn, with revenue up 7.4% to S$1.35bn, driven by growth across AI-related infrastructure, test and measurement, networking and semiconductor equipment.

The Assembly Place and its JV partners have acquired a freehold site at 50 Jalan Harom Setangkai in Bukit Timah, District 10, to redevelop into five terrace houses for sale.

StarHub will move all of MyRepublic’s 4G and 5G mobile customers onto its own network, shifting MyRepublic’s 4G base away from M1, which it had leased since 2020.

US

Moderna‘s mFlusiva, the first mRNA-based flu vaccine, has received FDA approval for adults 50 and older.

Alphabet sold US$25bn of investment-grade bonds across 10 tranches, drawing roughly US$115bn in peak demand.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Market Journal articles powered by PhillipGPT

Raffles Medical Group Faces Challenging Operating Environment

Frasers Centrepoint Trust Maintains Strong Position Despite Minor Operational Adjustments

PSR Stocks Coverage

For more information, please visit:

https://www.stocksbnb.com/singapore-stocks-coverage/

HK Reports

Read up on our Hong Kong reports here

Upcoming Webinars

Corporate Insights by IREIT Global

Date & Time: 7 August 26 | 12PM-1PM

Register: poems-20260807-152073

Corporate Insights by BHG REIT

Date & Time: 12 August 26 | 12PM-1PM

Register: poems-20260812-152075

Corporate Insights by Manulife US REIT

Date & Time: 13 August 26 | 12PM-1PM

Register: poems-20260813-151432

Corporate Insights by JustCo

Date & Time: 14 August 26 | 12PM-1PM

Register: poems-20260814-152531

Corporate Insights by Thakral Corporation Ltd [NEW]

Date & Time: 20 August 26 | 12PM-1PM

Register: poems-20260820-152846

Corporate Insights by Keppel REIT

Date & Time: 25 August 26 | 12PM-1PM

Register: poems-20260825-152077

Corporate Insights by Micro-Mechanics [NEW]

Date & Time: 27 August 26 | 12PM-1PM

Register: poems-20260827-152848

POEMS Podcast:

Research Videos

Weekly Market Outlook: TSLA, GOOGL, AMD, OUE REIT, SIAEC, KDCREIT, Tech Analysis & More!

Date: 27 July 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.