DAILY MORNING NOTE | 10 March 2025

Recent Podcasts:

OCBC – Earnings miss from higher allowances and expenses

UOB Ltd – Higher allowances hurt earnings

Singapore Airlines – Better than expected 3Q25 performance

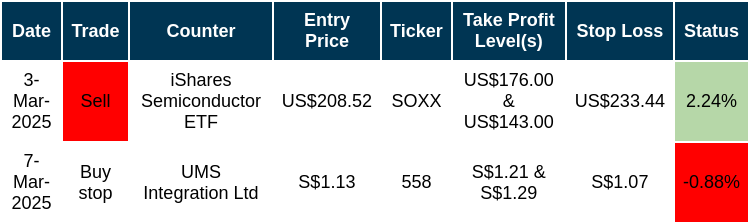

Trades Initiated in Past Week

Week 11 Equity Strategy: Despite all the negative sentiment, the S&P 500 is only down 1.7% this year with Nasdaq bearing the brunt of the weakness with a 5.8% drop. The US markets are not cheap at 28x PE, with Nasdaq a more incredible 38x PE. When the momentum falters, valuations will start to matter. Do you want to own Apple trading at 37x PE where revenue and earnings have been flat the past 3 years? The difference now is the risk of a slowing economy and the threat of a trade war. Firstly, sentiment indicators for consumption and manufacturing have started to turn down. Atlanta Fed GDP now is in QoQ contraction, the first in 135 weeks. Secondly, we worry corporates will turn cautious about spending due to tariff uncertainty. Thirdly, DOGE is freezing spending budgets and hiring plus firing employees. February payrolls show a 10k contraction in workers, the largest in almost 3 years. It is unclear if this is a trend caused by DOGE. If investing includes defence or avoiding losses, this might be the period to turn defensive.

For Asian markets, the worry is 2 April when we prepare for reciprocal tariffs from the US. We worry it could become, reliving the speech by President Roosevelt, a date which will “live in infamy” where the Rest of the World was suddenly and deliberately attacked by reciprocal tariffs. The next wave of tariffs could be on SE Asia. All countries will be impacted but we could fare better than China’s higher tariff of 20%. We believe several sectors in Singapore are better sheltered from a trade war. It includes construction, defence, finance, property, power, and telcos. Manufacturing is burdened by tariff uncertainty.

In corporate meetings, Trans China Auto which distributes BMW in China mentioned a tough operating environment. The weak economy and intense competition mean price is king. Furthermore, BMW does not have a strong product line-up in EVs to compete with Chinese operators. A new BMW EV global launch in 3Q25 with sales in 1Q26 could be the turnaround. BMW need to better distinguish itself given the quality of Chinese bands. Batteries globally are made by the same 2-3 manufacturers. Chinese consumers differentiate by the technology in the car, e.g. voice commands or FSD. BMW is still an aspirational brand that thrives in a strong economy but the price premium is still too high. Chinese consumer sentiment is weak and looking to trade down rather than upgrade. In the UMS briefing, we saw the outlook was better for 2025 with the new customer in Penang ramping up volumes. This is despite execution challenges from the lack of manpower. For their 3rd plant in 2028, the company is worried Malaysia is running out of skilled manpower or becomes too expensive. The company will invest more in automation, robots and AI in this facility.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

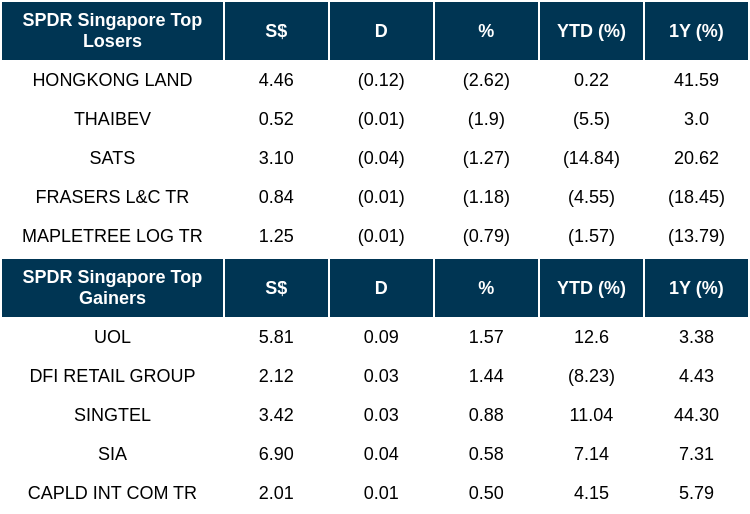

Singapore stocks finished Friday (Mar 7) lower, mirroring declines in regional indices. Stocks inched down 0.1 per cent or 2.58 points to 3,914.48. Across the broader market, decliners outnumbered advancers 287 to 247 after 1.4 billion shares worth S$1.5 billion changed hands. The trio of local banks were mixed at the close on Friday. DBS was up 0.04 per cent or S$0.02 at S$45.98, UOB rose 0.1 per cent or S$0.03 to S$38.63, while OCBC lost 0.2 per cent or S$0.03 to end at S$17.16. The top gainer was UOL, which climbed 1.6 per cent or S$0.09 to S$5.81. Meanwhile, the top loser was Hongkong Land, which fell 2.6 per cent or US$0.12 to US$4.46.

WALL Street stocks finished higher on Friday (Mar 7) after a roller-coaster session following mixed labour market data, concluding a losing week on a positive note. The broad-based S&P 500 finished at 5,770.20, up 0.6 per cent for the day but down 3.1 per cent for the week. The Dow Jones Industrial Average added 0.5 per cent at 42,801.72, while the tech-rich Nasdaq Composite Index climbed 0.7 per cent to 18,196.22. US jobs data for February showed the country’s economy added 151,000 jobs last month, up from January’s revised 125,000 figure, but fewer than analysts estimates as unemployment ticked higher.

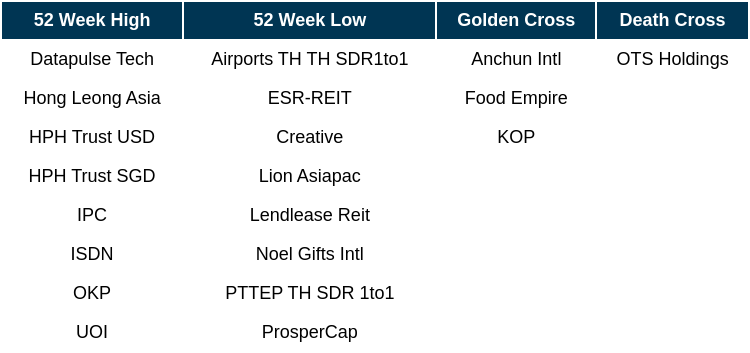

Singapore Technical Highlights

TOP 5 GAINERS & LOSERS

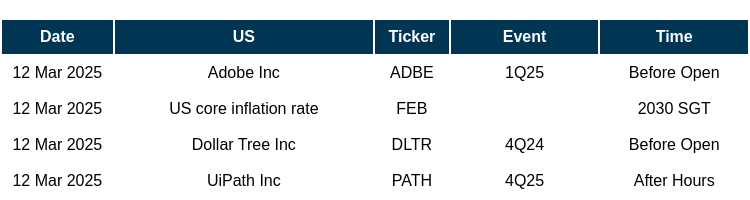

Events Of The Week

SG

Singapore logistics provider YCH Group is set to invest in at least four SuperPorts – which are multimodal logistics ports – across South-east Asia over the next five years, starting with hubs in Vietnam and Cambodia. Additional projects – including those following the model of YCH’s iconic Supply Chain City in Singapore – are also planned for Malaysia, Indonesia, the Philippines and Laos, and will enhance the region’s cargo flow.

Singapore Exchange (SGX) Group saw its securities market turnover value and securities daily average value (SDAV) grow 42% m-o-m to $29.6 billion and $1.5 billion respectively. The bellwether index grew 1% m-o-m, reaching 3,934.09 on Feb 19. It outperformed its Asean peers with a year-to-date 2.7% price return and 3.1% total return. The total number of listed securities in Feb stood at 614, down from the 615 in January.

Wee Ee Lim has received 115 million shares in UOL Group and 1.64 million shares in Haw Par Corporation from Wee Cho Yaw’s estate, according to bourse filings dated March 7. Wee is the younger son of the late banking magnate Wee Cho Yaw. He is a chairman at UOL Group and CEO of Haw Par Corporation.

Due to increased rental and occupancy rates at its dormitories, Centurion Corporation ’s revenue for the financial year ended Dec 31, 2024, rose by 22% y-o-y to $253.6 million. Boosted by fair value gains, earnings surged 125% y-o-y to $344.8 million. If this item was excluded, net profit attributed to equity holders rose by 43% y-o-y to $99.3 million. Centurion plans to pay a final dividend of 2 cents per share, bringing the FY2024 total to 3.5 cents versus 2.5 cents in FY2023.

StarHub has built Cloud Infinity, its hybrid multi-cloud platform, using Red Hat OpenShift to enhance its digital services. The platform leverages cloud-native and AI-driven technologies to deliver a vast array of digital platforms and services for both the telco and its customers.

Singapore Telecommunications (Singtel) and Palo Alto Networks have jointly developed two solutions that aim to help enterprises strengthen their cybersecurity posture. The first is the Unified Secure Access Service Edge Convergence (Unified SASE Convergence), which leverages Palo Alto Networks Prisma SASE and Precision AI solutions. It combines Software-Defined Wide Area Networking (SD-WAN) and SIM-based authentication to help enterprises verify a user’s identity and the Internet of Things (IoT) devices connected to Singtel’s network. Secondly, Singtel has expanded its 5G Security-as-a-Slice (SecaaS) capabilities with Palo Alto Networks Next Generation Firewall to protect roaming customers from foreign network vulnerabilities, surveillance risks and hacking attempts.

US

US Federal Reserve chair Jerome Powell on Friday (Mar 7) signalled potential changes for the Fed’s closely watched “dot plot” interest-rate projections as part of a broad policy framework review underway at the US central bank and expected to wrap up by the end of summer. It remains to be seen if the Trump administration’s tariff plans will prove to be inflationary, mapping out a checklist of things that could cause new import taxes to lead to more persistent price pressures.

Some artificial intelligence (AI) improvements to Apple’s voice assistant Siri will be delayed until 2026, the company said on Friday (Mar 7). In a statement, Apple said it has “been working on a more personalised Siri, giving it more awareness of your personal context, as well as the ability to take action for you within and across your apps. It’s going to take us longer than we thought to deliver on these features and we anticipate rolling them out in the coming year”. Apple did not give a reason for the delays. The iPhone maker had previously indicated the features would come in 2025.

The US Department of Justice (DOJ) on Friday (Mar 7) dropped a proposal to force Alphabet’s Google to sell its investments in artificial intelligence (AI) companies, including OpenAI competitor Anthropic, to boost competition in online search. The DOJ and a coalition of 38 state attorneys general still seek a court order requiring Google to sell its Chrome browser and take other measures aimed at addressing what a judge said was Google’s illegal search monopoly.

Microsoft has created in-house artificial intelligence (AI) models it believes can go toe-to-toe with industry leaders including partner OpenAI. A family of models Microsoft is developing recently produced test results suggesting that they were competitive with state-of-the-art rivals, including products from OpenAI and Anthropic.

Millennium Management lost about US$900 million so far this year from two teams focused on index rebalancing, a strategy recently upended by global stock market volatility. Glen Scheinberg runs the larger of the two index-rebalancing teams, a group known as SRBL, while Dubai-based Pratik Madhvani manages the other crew focused on the strategy.

A slide in Tesla on Friday (Mar 7) is capping off a round trip of epic proportions in the company’s shares. Expectations that the electric vehicle (EV) maker would benefit from CEO Elon Musk’s close relationship with US President Donald Trump made its stock one of the top gainers following the Nov 5 election. That bet, however, has been no match for growing anxiety about Tesla’s core business of selling cars. Tesla’s shares were down 4.6 per cent at 11.53 on Friday, on track to erase their entire US$700 billion post-election advance. The decline comes alongside a series of blows that have shaken investor confidence in recent weeks, from a January report showing that sales dropped for the first time in a decade last quarter to more recent evidence of Tesla losing its dominant position in Europe and China. Some investors have also grown worried that Musk’s foray into politics has become a distraction from his job as the EV giant’s CEO.

US consumers dialled back the pace of borrowing in February after a near-record increase a month earlier. Total credit increased US$18.1 billion in January after a revised US$37.1 billion jump in December, according to US Federal Reserve data on Friday (Mar 7). Outstanding credit card and other revolving debt climbed US$9 billion. Non-revolving credit, such as loans for vehicle purchases and school tuition, advanced by a similar amount. Both were decelerations from the prior month.

Robinhood Markets, the online trading platform, agreed to pay US$29.75 million to resolve several Financial Industry Regulatory Authority (Finra) probes into its supervision and compliance practices, including failure to respond to “red flags” of potential misconduct. The brokerage regulator said on Friday (Mar 7) that Robinhood will pay a US$26 million civil fine and US$3.75 million of restitution to customers. Finra accused Robinhood of violating “numerous” rules, including a failure to implement reasonable anti-money laundering programmes that caused it to miss suspicious or unauthorised trading and hackings of customer accounts.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, PSR

RESEARCH REPORTS

HRnetGroup Limited – Collecting income, no growth yet

Recommendation: ACCUMULATE; TP S$0.78; Last close: S$0.6950; Analyst Paul Chew

- Results were below our expectations. FY24 revenue and adjusted PATMI were 95%/85% of our FY24e forecast. Adding back the S$3.1mn delay in progressive wage credit scheme (PWCS) payment, the results will be 91%. Dividends were maintained at 4 cents in FY24, with a payout ratio of 85%.

- Professional recruitment remains the weakest segment, declining 16% in 2H24. It has been on a decline for the past 2.5 years. Weak and uncertain macro conditions are causing delays or hesitancy in hiring. Flexible staffing revenue is stable with 1% growth in 2H24.

- HRnet is widening its strategy to access a larger recruitment market share. The company is targeting more C-suite roles and entering the recruitment of foreign manpower in the service industry. We are lowering FY25e earnings by 14%. Recovery in recruitment has been delayed and may worsen with the current macro uncertainty. We are still forecasting modest growth in FY25e including the delayed PWCS payment and additional growth from new target segments. Our recommendation is downgraded from BUY to ACCUMULATE and the target price lowered to S$0.78 (prev. S$0.82). The company is paying an attractive dividend yield of 5.8% with planned share buyback of S$11.2mn (~16mn shares) backed by a net cash of S$258mn.

Hyphens Pharma International – Investing for future growth

Recommendation: BUY; TP S$0.35; Last close: S$0.2800; Analyst Paul Chew

- FY24 earnings were below expectations. Revenue and PATMI were 102%/94% of our FY24e forecast. 2H24 PATMI declined 4% YoY to S$4.8mn due to weaker margins in proprietary brands, a decline in Vietnam sales and higher losses from DocMed.

- The softer earnings are from Hyphens expanding the distribution of proprietary brands into more SE Asian countries and retail chains. The DocMed platform (for doctors and pharmaceutical companies) requires further development, especially with the expansion into Malaysia and Vietnam.

- Our BUY recommendation, FY25e earnings and DCF target price of S$0.35 is maintained. Hyphens’ earnings growth will be impacted in the near term from its expansion into new countries and additional investments into the DocMed platform. Hyphens’ valuations are attractive at 7x FY25e PE with a net cash balance sheet of S$23mn. It is a branded consumer healthcare company (nutraceuticals, medical aesthetics and pharmaceuticals) with a regional presence.

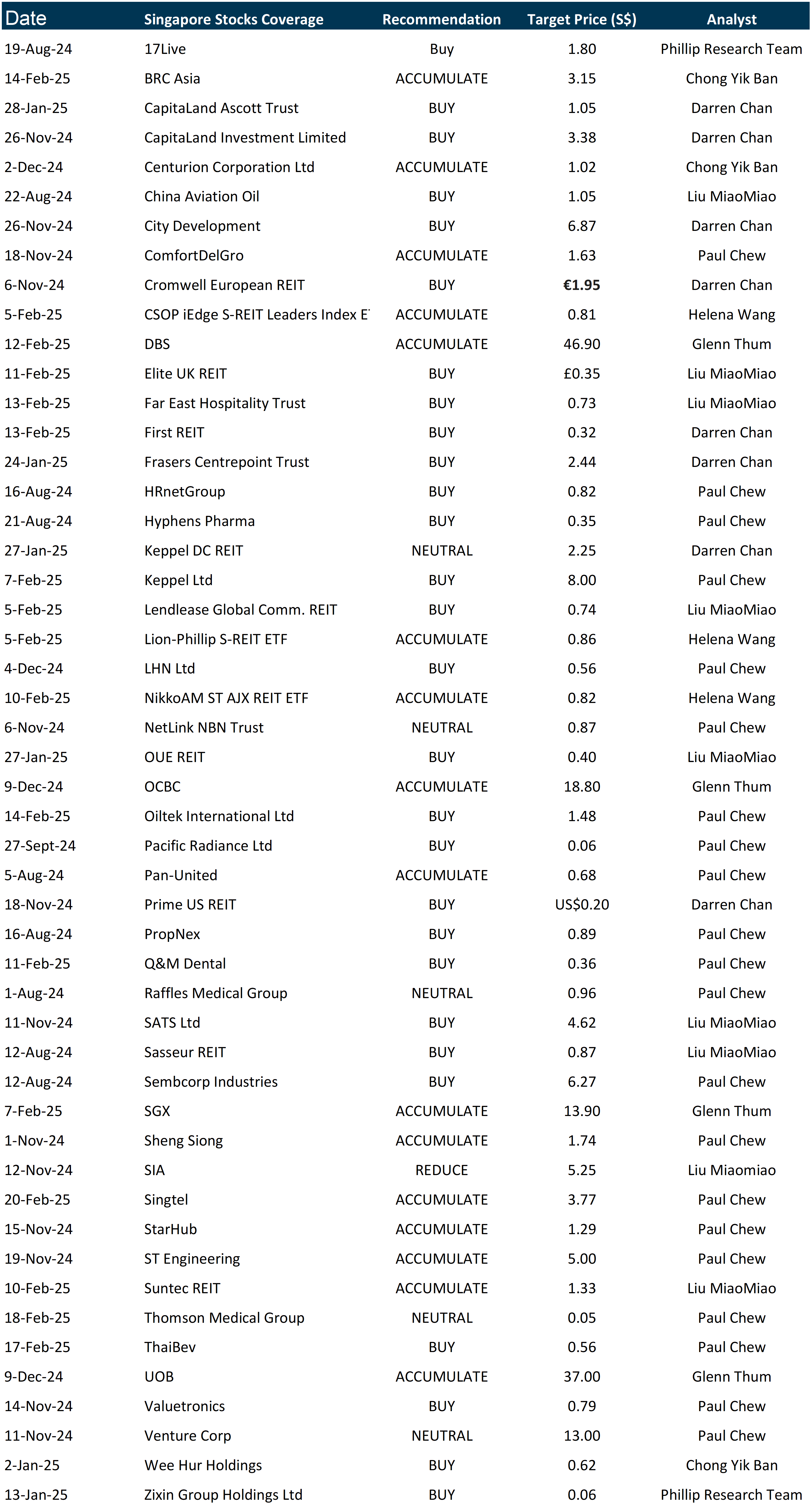

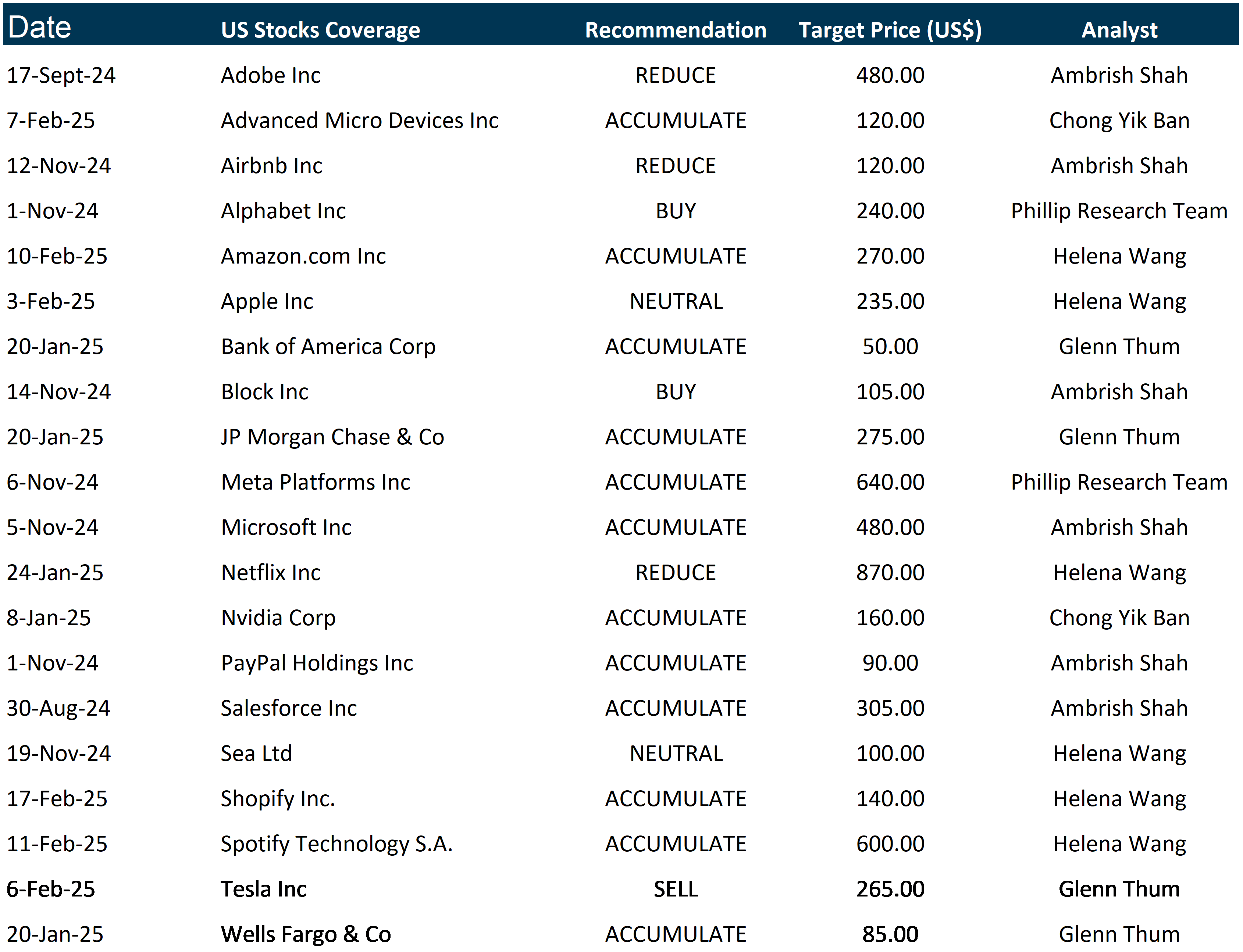

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by TeleChoice

Date & Time: 11 March 25 | 12PM-1PM

Register: poems-20250311-112959

Strategy & Stock Picks – SG Market [NEW]

Date & Time: 5 April 25 | 10AM-12PM

Register: poems-20250405-114051

Strategy & Stock Picks – US Market [NEW]

Date & Time: 10 April 25 | 7PM-9PM

Register: poems-20250410-114061

POEMS Podcast:

Research Videos

Weekly Market Outlook: Hong Leong Asia, Sheng Siong, YZJ Financial, ST Engin, Oiltek, Banks & More!

Date: 3 March 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials