DAILY MORNING NOTE | 13 March 2026

Recent Podcasts:

Advanced Micro Devices Inc. – Clear Instinct GPU roadmap, strong CPU demand

Netflix Inc. – Content, ads, and scale drive the next leg of growth

The Walt Disney Company – Streaming Turns Profitable

Singapore blue-chip stocks declined after oil surged above US$100 a barrel. Benchmark Index closed 8.48 points or 0.2% lower at 4,855.33, while the iEdge Singapore Next 50 Index rose 8 points or 0.6% to 1,445.12.

The Dow Jones Industrial Average fell 739.42 points, or 1.56%, closing at 46,677.85. The S&P 500 lost 1.52% and settled at 6,672.62, while the Nasdaq Composite shed 1.78% to end at 22,311.98. All three indexes posted closing lows for 2026, and the 30-stock Dow ended the session below the 47,000 threshold for the first time this year.

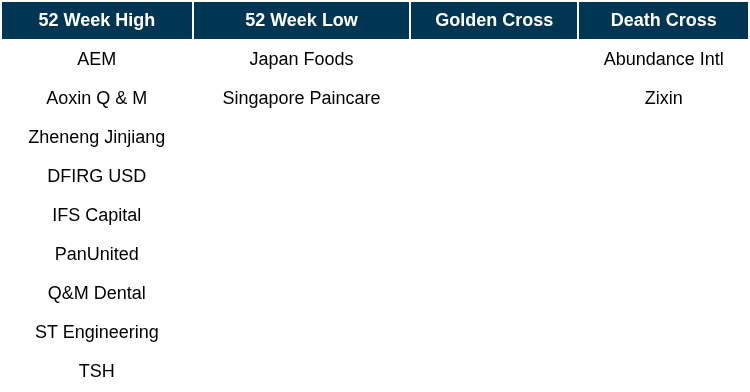

Singapore Technical Highlights

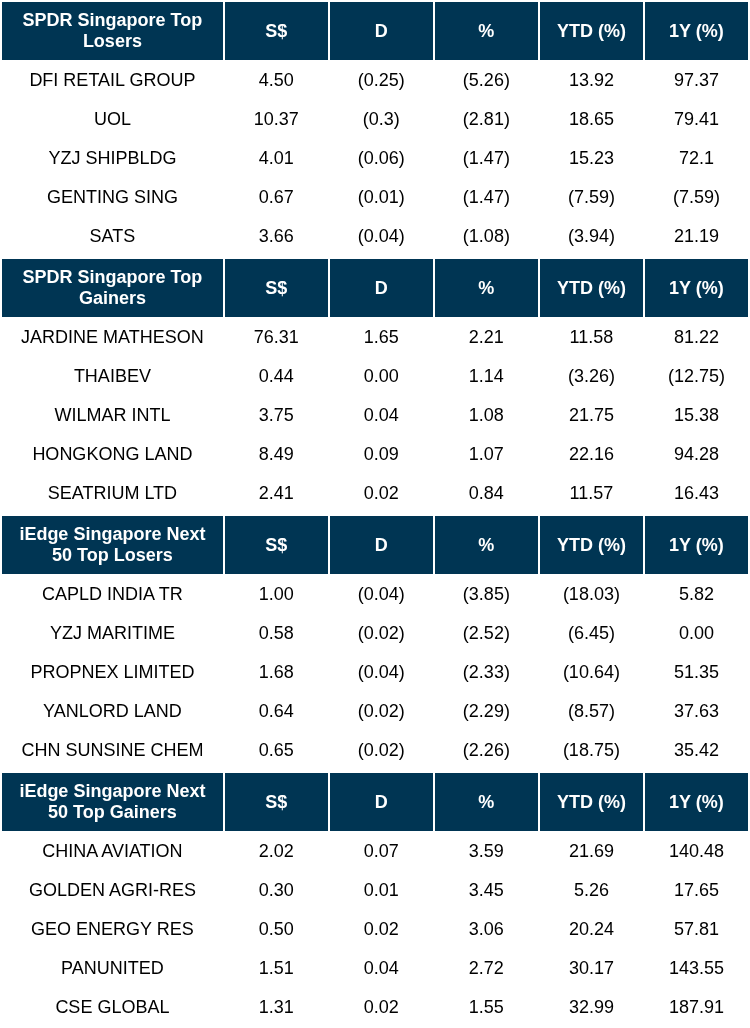

TOP 5 GAINERS & LOSERS

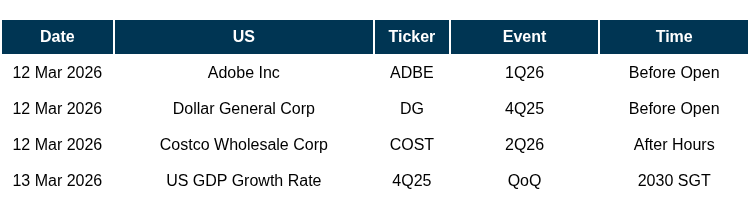

Events Of The Week

SG

MetaOptics has shipped its Automatic Metalens Tester to a partner in Taoyuan, Taiwan, contributing to its efforts in establishing end-to-end metalens manufacturing capabilities in the region.

KSH Holdings secured a new contract worth over S$32mn, bringing its total order book to approximately S$1bn with earnings visibility through FY2030.

Seatrium’s Petrobras P-78 FPSO achieved first gas injection 61 days after first oil at the Búzios field in Brazil’s Santos Basin. The vessel, one of the largest FPSOs ever delivered to Brazil, can produce up to 180,000 barrels of oil and 7.2mn cubic metres of gas per day.

US

Bain Capital’s Bridge Data Centres plans to invest up to US$5bn in AI infrastructure in Singapore, targeting advanced power architectures, next-generation cooling and AI-enabled operations.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Oiltek International Ltd – Becoming an oil price proxy

Recommendation: BUY; TP S$1.18; Last close: S$0.8000; Analyst Paul Chew

- FY25 adj.PATMI was within our expectations at 101% of our FY25e forecast. Revenue was below expectations at 83% of our FY25e. Gross margins rose on project completions and procurement savings. FY25 dividend per share jumped 33% to 1.2 cents.

- New orders secured in FY25 were softer at RM152mn (FY24: RM207mn). We believe the change in palm oil policies in Indonesia and the pivot towards recurrent income projects were key drivers of the lower order book. Our expectations are for a significant rebound in orders in FY26e, led by both refining and renewables projects.

- We lowered our FY25e PATMI by 7% to RM44.5m and raised our FX assumptions for the ringgit. Our target price of S$1.18 is unchanged. We peg Oiltek to 35x PE FY26e, a premium to listed peers in Malaysia due to its strong earnings growth profile. Global sustainable aviation fuel oil (SAF) demand is expected to spike from 1.9mn tons in 2025 to 7.8mn in 2030. We believe the demand for SAF and biodiesel will further accelerate with the recent spike in oil prices and the need for energy self-sufficiency. The opportunities ahead for Oiltek are EPCC contracts and ownership stakes in SAF plants, plus contracts in refinery and biodiesel plants. Oiltek is asset-light with a 35% ROE despite the RM100mn net cash balance sheet.

Singapore Banking Monthly – Earnings supported by fee income

Analyst: Glenn Thum

- February’s 3M-SORA was down 2bps MoM to 1.16%, the smallest MoM decline in 20 months, and fell by 168bps YoY. Singapore loan growth has continued to climb (Jan26: +6.1%). Banks are guiding low to mid-single digit. CASA rose 12% YoY and CASA ratio to deposits at 19.8% (Dec25: 19.6%), a tailwind for banks, lowering funding costs and cushioning NIM compression.

- 4Q25 bank earnings were slightly below expectations. Earnings dipped 5% YoY, from lower NII (-5%) as NIMs fell by 22bps YoY. Fee income growth (+13%) partially offset the lower NII. The banks are guiding for NIM compression to ease in FY26e as deposit rate cuts begin to flow through and interest rates stabilise. We expect FY26e PATMI to increase by 7% YoY, as fee income growth will be partially offset by the decline in NII. All three banks have committed to complete their previously announced capital return plans.

- Maintain NEUTRAL. Declining interest rates will continue to compress FY26e NIMs and NII. However, the increased volatility and jump in SDAV is boosting capital markets and fee income, helping offset these headwinds. Furthermore, spiking oil prices raise inflation risks, potentially delaying further rate cuts and supporting margins. Despite asset quality concerns at UOB, we view their pre-emptive provisioning as prudent and overall risks as contained. Banks’ dividend yields remain attractive at 5.1%, with ongoing buybacks improving ROE. We prefer DBS (fixed-dividend policy) and OCBC (wealth management growth and excess capital).

TeleChoice International Ltd – Growth intact

Recommendation: BUY; TP S$0.275; Last close: S$0.1870; Analyst Paul Chew

- FY25 results were within expectations. Revenue/PATMI were 105%/103% of our forecast. Revenue expanded 27% YoY to S$276mn, supported by U-Mobile 4PL services. Adj. PATMI grew at a slower 20% YoY to S$4.4mn due to lumpy inventory provisioning. FY25 dividends more than tripled to 0.45 cents.

- Personal communications system (PCS) remains the key growth driver. Revenue grew 42% YoY to S$200mn, driven by U-Mobile subscriber growth and higher postpaid plans that require handset subsidies. TeleChoice also increased outlets, widened the range of phones and introduced more accessories.

- We raise our FY26e PATMI by 13% to S$8.3mn and maintain our BUY recommendation. The target price is raised to S$0.275 (prev. S$0.215). Our valuation of 15x P/E for FY26e is based on SGX-listed proxies in the system integration and software sectors. The growth momentum in PCS is intact. Network engineering is turning around from managed services and network buildout projects in Indonesia and Malaysia. TeleChoice announced that it is evaluating an expansion into higher-growth segments within digital infrastructure, including data centres.

Market Journal articles powered by PhillipGPT

SIA Engineering Posts Strong Q3 Results on Associate Earnings Growth

Raffles Medical Group Faces Sluggish Growth on Mixed Results

Grab Holdings Achieves First Full Year of Net Profit with Strong Revenue Growth

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Ever Glory

Date & Time: 13 March 26 | 12PM-1PM

Register: poems-20260313-140475

Corporate Insights by Lum Chang Creations Limited [NEW]

Date & Time: 27 March 26 | 12PM-1PM

Register: poems-20260327-141688

Corporate Insights by Thakral Corporation Ltd [NEW]

Date & Time: 31 March 26 | 12PM-1PM

Register: poems-20260331-141690

Corporate Insights by Thakral Corporation Ltd [NEW]

Date & Time: 31 March 26 | 6PM-9PM

Register: poems-20260331-141692

POEMS Podcast:

Research Videos

Weekly Market Outlook: SEA, CDL, SSG, CNMC, Ever Glory, CDG, PropNex, SG Weekly & More!

Date: 9 March 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials