DAILY MORNING NOTE | 15 June 2026

Recent Podcasts:

Salesforce Inc – Share buyback cuts outstanding shares by 11%

Nordic Group – Multi-year project upcycle intact

SATS Ltd – Strong cargo volumes, new contract wins drive growth

Week 25 equity strategy: SpaceX is now valued at US$2.1tr. The company is losing annualised US$10bn and has negative FCF of at least US$30bn. 1Q26 revenue growth was only 15% YoY. Without earnings and a lack of visibility to positive cash flows, the relative valuation is price to sales of 112x (annualised). There is the Musk premium, but even at Tesla’s peak, price to sales was 24x (monthly basis). I guess with space, the addressable market is intergalactic with optionality on Mars. However, the largest market opportunity targeted by SpaceX is the US$22.7tr enterprise AI. This is where it has to compete with other frontier models such as OpenAI, Anthropic and Gemini. It is also becoming a neo-cloud or financing business by selling GPU compute capacity to Anthropic. The wrapper may be space, but most of the resources are deployed for frontier AI model cum neo cloud operations. Nevertheless, there is a trading opportunity by “front-running” the passive funds that have to buy SpaceX. All major indexes will be adding SpaceX – FTSE (5 days), MSCI (10 days), Nasdaq 100 fast (15 days) and S&P 500 (12 months). The first shareholder lock-up period to end is 20% of 12.2 bn shares after the first earnings (or Jun26 quarter) release date.

The bull case for AI infrastructure is anchored on the revenue growth of LLMs OpenAI and Anthropic. Coatue estimate for Anthropic and OpenAI combined revenue is US$85bn in 2026 and reaching almost US$300bn by end 2027 (and larger than Microsoft). We think such growth is possible when the product is underpriced and sold at a loss. Also arguable is that most enterprises are still testing AI. The problem of hallucination remains an issue. The technology is sound, but maybe not the economics. The US$85bn revenue is now the foundation of roughly US$800bn annual spend on data centres and rising. We think semiconductors (esp. equipment) are still the best way to capture the growth in AI. There is no choice but to invest in compute capacity to compete. Mag 7 has yet to feel the earnings pressure on all this capex. For instance, Alphabet’s expected capex in 2026 is US$185bn. This will double depreciation to around US$40bn, a 14% drag on earnings that is yet to materialise.

Paul Chew

Head Of Research

Paulchewkl@phillip.com.sg

Singapore stocks ended higher on Friday (Jun 12). The local benchmark gained 0.8 per cent or 37.7 points to finish at 5,025.80. Across the broader market, gainers outnumbered losers 376 to 194, after 1.4 billion securities worth S$2 billion changed hands.

U.S. stocks rose on Friday as SpaceX’s opening pop bolstered sentiment, with investors hoping for the arrival of a potential peace deal between the U.S. and Iran. The S&P 500 closed up 0.5% at 7,431.46, while the Nasdaq Composite added 0.31% to finish at 25,888.84. The Dow Jones Industrial Average advanced 353.51 points, or 0.7%, to settle at 51,202.26.

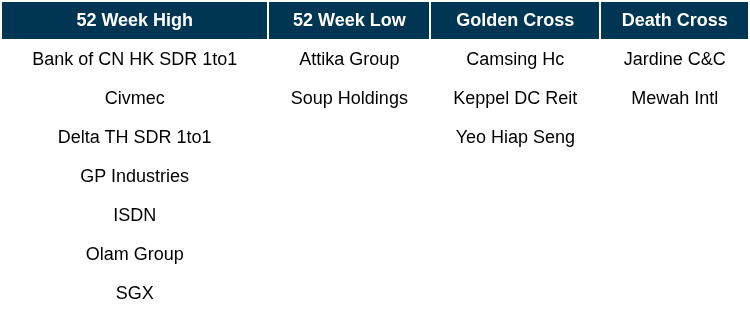

Singapore Technical Highlights

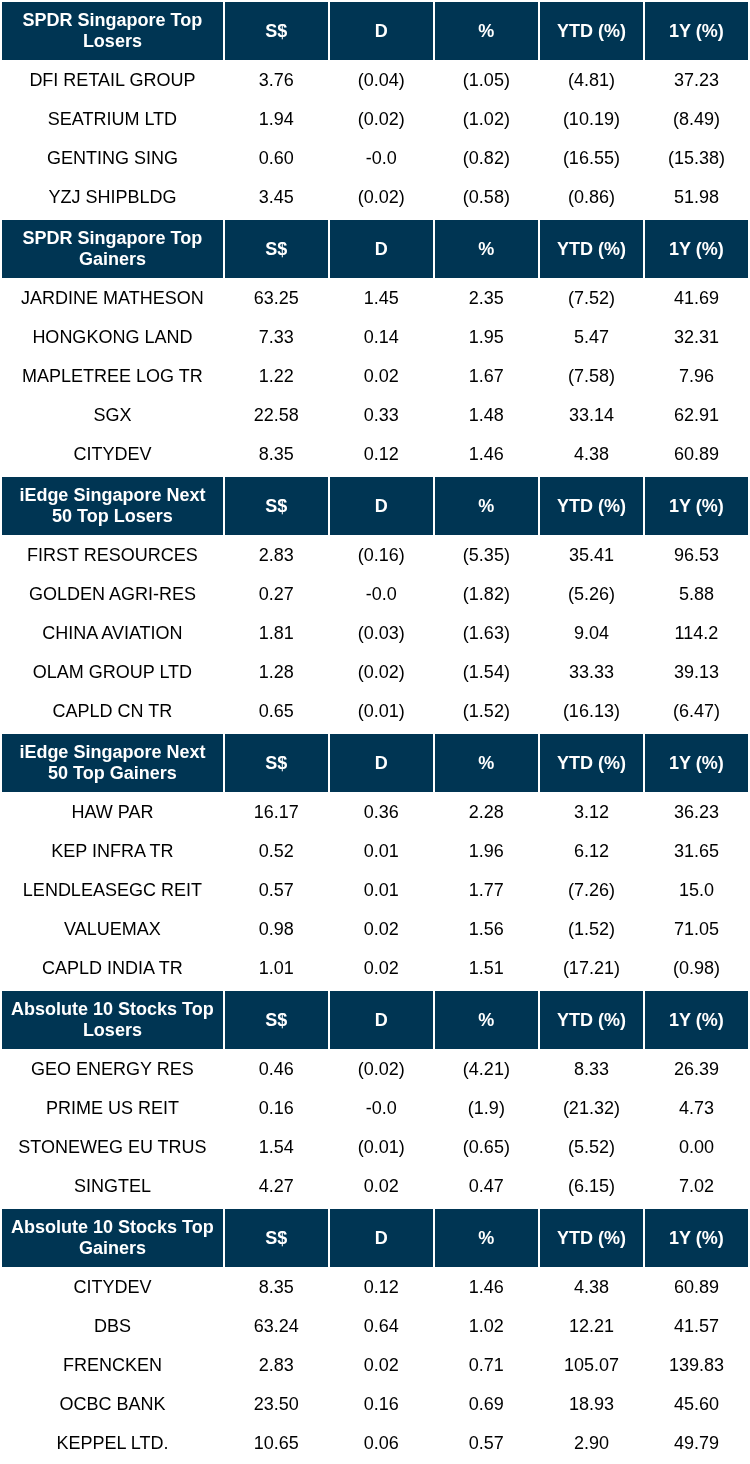

TOP 5 GAINERS & LOSERS

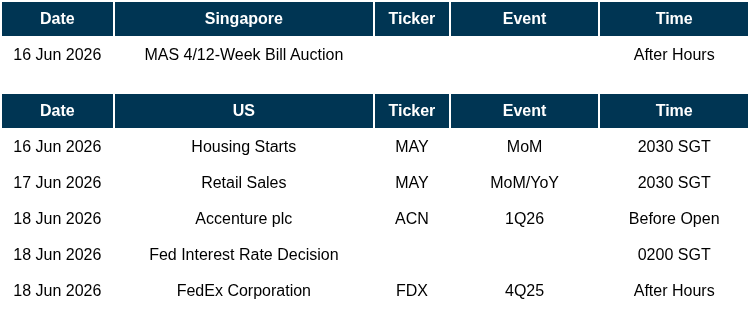

EVENTS OF THE WEEK

SG

Transport operator ComfortDelGro expects China and Singapore to be its prime markets for autonomous vehicles (AVs) in the near future. At a media briefing on the company’s AV strategy on Friday (Jun 12), Michael Huang, CDG’s head of its Singapore point-to-point mobility business, called China “ground zero” for AVs, describing Singapore as one of the places in the Asia-Pacific most ready for adoption.

Singapore Kitchen Equipment said on Thursday (Jun 11) that two executives, including its CEO, have been kept in their positions despite being charged with fraud and falsifying accounts because the criminal case has yet to be concluded. They are accused of falsifying 102 payment vouchers to fraudulently represent that a bonus payment of S$741,721.55 had been paid in January 2020, instead of the actual payment date of January 2019.

US

The U.S. Department of Justice has signed off on Paramount Skydance’s proposed acquisition of Warner Bros. Discovery, clearing the merger of federal antitrust concerns. The $110 billion deal could still face challenges from state attorneys general. Paramount Skydance CEO David Ellison has told investors that the merger is on track to be completed by September.

JetBlue Airways is setting its sights on a big expansion in Fort Lauderdale, Florida, with even more space opening up in Spirit Airlines’ wake. Fort Lauderdale’s major competitor in South Florida is Miami International Airport, an American Airlines stronghold.

Nvidia has told Chinese clients that its new “Vera” central processors for AI data centres could be available as soon as August and that they can begin placing orders.

SPACEX’s historic US$75 billion IPO drew more than US$350 billion in demand from institutions and retail investors. The largest ever initial public offering saw institutional investors place orders for more than US$250 billion of stock. The company sold 555.6 million shares at US$135 each in a deal that values it at roughly US$1.8 trillion.

Adobe said that its chief financial officer would depart, leaving the company without a top tier of veteran leadership after CEO Shantanu Narayen announced in March that he would step aside.

Anthropic PBC said it is complying with a Trump administration directive to suspend foreign nationals from access to its Fable 5 and Mythos 5 artificial intelligence models, and is subsequently disabling the tools for all users including those in the US.

United States and Iranian officials said on Sunday (Jun 14) they have agreed on a peace framework for a deal to end their war, halt the US blockade of Iran and reopen the Strait of Hormuz, possibly leading to lower energy prices once oil shipments resume through the critical waterway.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

SG Bonds – Week 25: SGS yields moved lower WoW

Analyst: Phillip Research Team

- UST yields moved lower over the week, supported by optimism over geopolitical de-escalation and positioning ahead of the FOMC meeting. The 2Y fell 7bps to 4.08%, while the 10Y and 30Y ended lower at 4.48% and 4.97%.

- SGS yields also moved lower over the week, broadly tracking the decline in UST yields. The 2Y, 5Y and 10Y SGS yields ended at 1.58%, 1.73% and 2.07%, respectively.

- Looking ahead, the key event will be the FOMC meeting on 18 June (SGT time). We expect the Fed to keep policy rates unchanged. Markets are still pricing in one rate hike by year-end. With this being Fed Chair Kevin Warsh’s first FOMC meeting, investors will likely focus on main two areas: first, whether he views the energy shock as temporary or persistent; second, what conditions would be required for the Fed to resume tightening. Domestically, we expect SGS yields to remain range-bound, barring any major surprise in economic data. Focus will be on Singapore’s May NODX data, with markets watching whether export momentum can sustain April’s strong AI-led growth.

Oracle Corp – CAPEX raised to US$70bn in FY27e

Recommendation: BUY (Maintained), Last done: US$184, TP: US$237, Analyst: Alif Fahmi

- 4Q26 revenue met our expectations while PATMI exceeded, FY26 revenue and PATMI at 101%/115% of our forecasts. Revenue rose 21% YoY, led by Oracle Cloud revenue growth (+47% YoY).

- Strong revenue visibility with RPO contracted rose 4.6x to US$638bn. Revenue to accelerate to 34% YoY in FY27e (FY26: 16%), driven by Cloud Infrastructure business surging 109% (1Q27e additions are nearing 1GW, close to FY26’s full year 1.2GW). OpenAI’s five year US$300bn OCI commitment starts in 2027, with its IPO expected to bolster capital for FY27e obligations. The five largest Stargate sites are on track, with the Abilene, Texas campus 42% complete and set for 1.2 GW by end 2026. Four more sites across Texas, New Mexico, Michigan, and Wisconsin are under construction, with deliveries starting in 2027, scaling total capacity to 7 GW toward a 10 GW target.

- We maintain a BUY rating with a lower DCF target of US$237 (prev. US$275), as we raised CAPEX to US$70bn in FY27e as guided (net of US$20–25bn in customer prepayments), from our initial estimates of US$47bn. Our WACC and g remain unchanged. Customers likely continue to favour Oracle’s end-to-end stack (infrastructure to cloud). US$75bn in bookings under the new funding model over two quarters (12% of RPO) underscores strong customer preferability for Oracle despite prepayments and bring-your-own-hardware requirements.

Market Journal articles powered by PhillipGPT

Geo Energy Resources Maintains Growth Trajectory Despite Q1 Challenges, S$0.75 Target Price Upheld

Salesforce Inc Maintains Strong Growth Trajectory with BUY Rating and US$270 Target Price

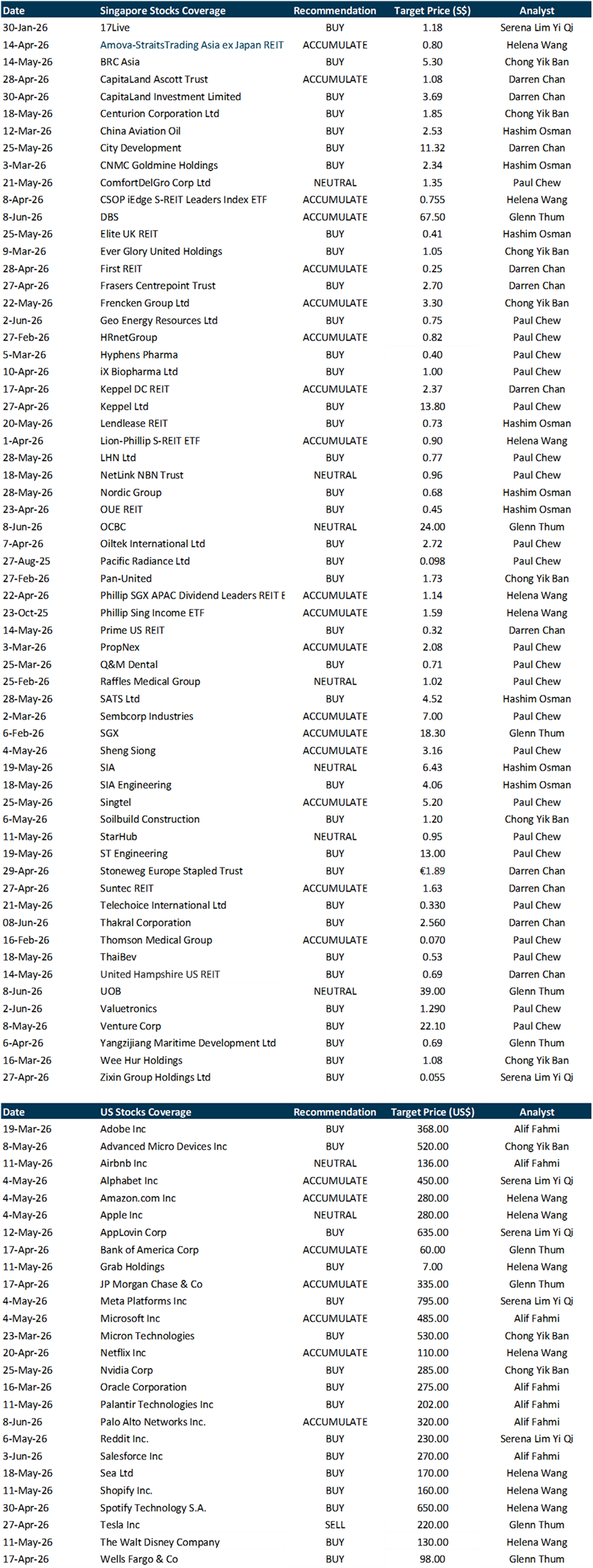

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by AIMS APAC REIT

Date & Time: 17 June 26 | 12.30PM-1.30PM

Register: poems-20260528-145702

Corporate Insights by LHN Limited

Date & Time: 1 July 26 | 12PM-1PM

Register: poems-20260701-149539

Corporate Insights by iX Biopharma Ltd

Date & Time: 2 July 26 | 12PM-1PM

Register: poems-20260702-149541

Corporate Insights by Coliwoo [NEW]

Date & Time: 8 July 26 | 12PM-1PM

Register: poems-20260708-149543

POEMS Podcast:

Research Videos

Weekly Market Outlook: Salesforce, Palo Alto, Thakral, SATS, SGBanking, SG Weekly & More!

Date: 8 June 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials