DAILY MORNING NOTE | 16 February 2026

Recent Podcasts:

Advanced Micro Devices Inc. – Clear Instinct GPU roadmap, strong CPU demand

Netflix Inc. – Content, ads, and scale drive the next leg of growth

The Walt Disney Company – Streaming Turns Profitable

Trade of The Day

Roundhill Magnificent Seven ETF (CBOE: MAGS)

Analyst: Zane Aw

(Current Price: US$61.73) – TECHNICAL SELL

Sell price: US$61.73 Stop loss: US$65.35 (-5.86%)Take profit: US$55.92 (+9.41%)

Trades Initiated in Past Week

Week 8 equity strategy – There were three key highlights for us in the Singapore Budget 2026. Firstly, Singapore is undertaking a massive pivot and retraining in AI. AI can be a strategic advantage to our constraints in labour and natural resources. More funds in research, grants, tax deduction, training and a AI council chaired by the Prime Minister. Next was the importance of enhancing the vibrancy of our equities market as a destination to grow and scale. The budget injected more liquidity into the market. A $1.5bn top-up to EQDP, $1.5bn top -up of Anchor Fund for pre-IPOs and CPF contributors raising their equity exposure with life-cycle funds. Finally, the fiscal position was strong with a S$15bn surplus, and it excludes the S$21bn of land sales considered capital receipts.

In corporate news, which was not really highlighted in mainstream media, drug developer iX Biopharma’s announced a momentous deal. It was awarded a US$41mn development contract by the US Department of Defense (DoD) to fund and support the Phase 3 approval of the pain drug Wafermine. It is to support near-term and long-term military medical needs. While waiting for approval, the DoD will purchase Wafermine for emergency use. We think this is a major endorsement of iX Biopharma’s Waferix technology to deliver drugs sublingually. Wafermine could be used to serve the 80mn US non-opioid acute pain market valued at US$4bn currently. The only other non-opioid pain drug is Journavx by Vertex Pharma.

Paul Chew

Head Of Research

paulchewkl@phillip.com.sg

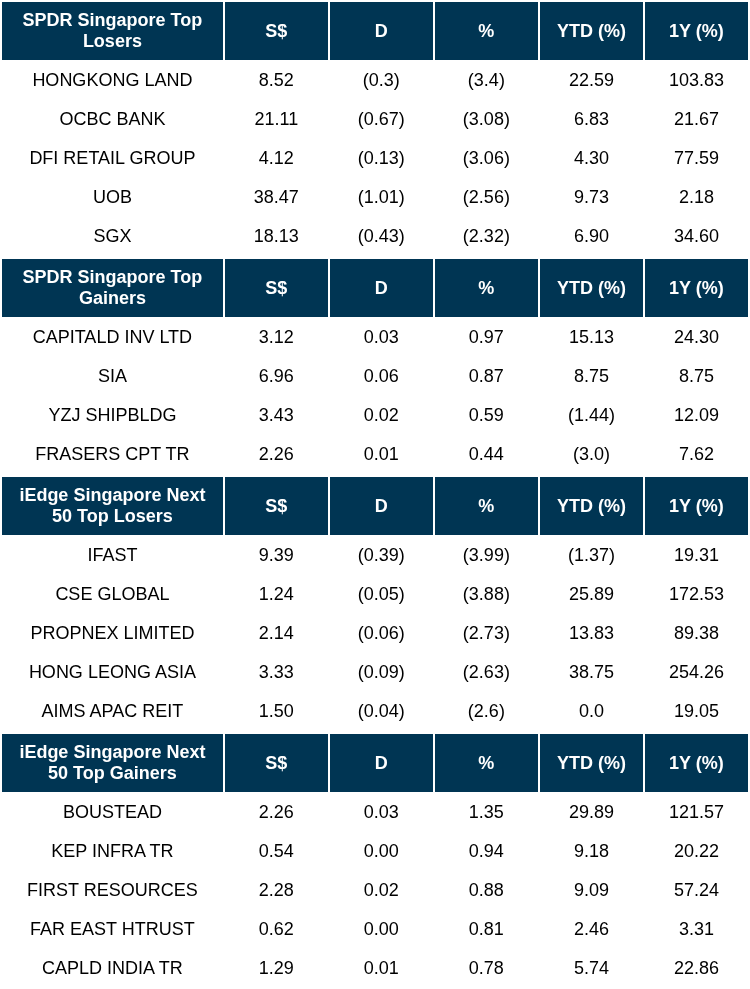

Singapore shares ended lower on Friday, tracking losses on regional indices. The benchmark Index fell 1.6% to 4,937.78. Meanwhile, the iEdge Singapore Next 50 Index nudged down 0.4% or 6.06 points to 1,513.52. Across the broader market, losers outnumbered gainers 413 to 220, after 1.6 billion securities worth S$2.6 billion changed hands.

The S&P 500 closed barely above the flatline on Friday as a key consumer inflation report that came in slightly lighter than expected failed to spark a substantial rally. The broad market index added 0.05% and ended at 6,836.17, while the Nasdaq Composite fell 0.22% and closed at 22,546.67. The Dow Jones Industrial Average gained 48.95 points, or 0.10%, and settled at 49,500.93.

Singapore Technical Highlights

TOP 5 GAINERS & LOSERS

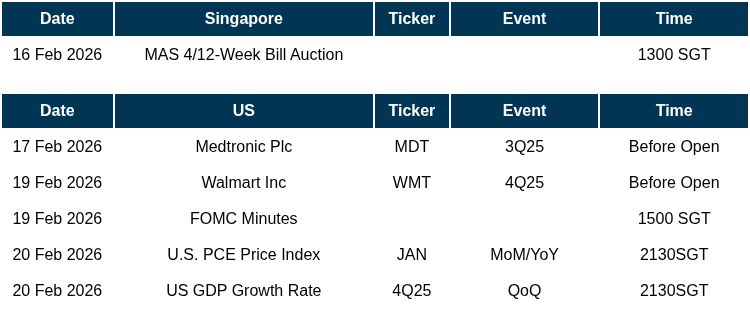

Events Of The Week

SG

Lendlease REIT 1HFY26 total DPU up 3.1% YoY to 1.85 cents (including advanced distribution of 1.3305 cents paid in December 2025). Gross revenue for the six months ended Dec 31 2025 fell by 1.6% YoY to S$101.9 million while NPI also fell by 1.2% YoY to S$74.0 million

Centurion Corporation acquires 65% stake in Manna 777 Properties for S$4.8 million. Manna 777 Properties owns a plot of freehold land at 7 Kim Chuan Lane, which spans 975.9 square metres and is near Tai Seng MRT station as well as ComfortDelGro Driving Centre.

Marco Polo Marine Q1 revenue jumps 27% to S$32.8 mn on strategic fleet additions. It was accompanied by higher profit margin of 43% for the period, up 2% YoY.

US

Spacex is weighing dual class IPO shares this year. A two-tier structure would give select shareholders stock with extra voting power that would allow them to take more control decision making.

China’s market regulator summoned major platforms such as Alibaba, and Douyin on February 13 to address price wars that were harming profitability.

Warner Bros Discovery Inc is considering reopening sale talks with rival Hollywood studio Paramount Skydance Corporation after receiving its hostile suitor’s most recent amended offer.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

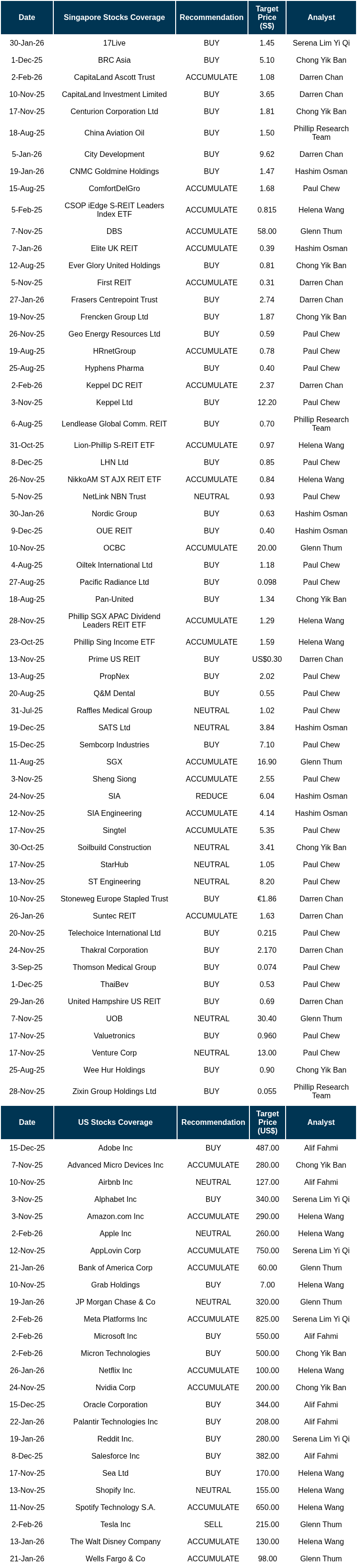

RESEARCH REPORTS

BRC Asia Ltd – Order book spike of 47% drives future growth

Recommendation: BUY; TP S$5.30; Last close: S$4.3200; Analyst Yik Ban Chong (Ben)

- BRC Asia provided 1Q26 update with limited financials. 1Q26 revenue/PATMI were within expectations, at 27%/26% of our FY26e forecasts. 1Q26 PATMI surged 30% YoY to S$27.3mn, driven by an estimated 42% YoY higher delivery volumes from stronger project offtake.

- Order book spiked 47% YoY to a record S$2.2bn in 1Q26. This was driven by order wins across HDB BTO contracts, Changi Airport T5, and healthcare projects. The Building and Construction Authority (BCA) projected total construction demand in Singapore to be S$47-53bn in 2026, 61% higher than the 20-year historical average. We believe BRC Asia can secure further contract wins in the coming quarters, including MBS Integrated Resort (IR) expansion contracts, New Tengah General & Community Hospital, and MRT LTA extension contracts.

- We maintain BUY with a higher TP of S$5.30 (prev. S$5.10). We raised our FY26e revenue/PATMI forecasts by 16%/16% respectively, on the back of stronger project offtake expected, driven by a record order book of S$2.2bn. WACC and growth rate assumptions are unchanged at 10%/2.5% respectively. BRC Asia trades at an attractive FY26e dividend yield of 5.3%.

CapitaLand Investment Limited – Sharp decline in China valuations

Recommendation: BUY; TP S$3.69; Last close: S$3.1200; Analyst Darren Chan

- FY25 PATMI of S$145mn (-70% YoY) was below our expectations, forming only 22% of our FY25e forecast due to significant S$439mn revaluation losses, mainly from China. Excluding these losses, FY25 operating PATMI of S$539mn was in line at 98% of our estimates. Operating PATMI rose 6% YoY on higher contributions from listed funds, lower finance costs, and reduced operating expenses.

- Funds Under Management (FUM) grew 7% YoY to S$125bn. CLI believes it can grow FUM to c.S$160bn organically but acknowledges that acquisitions will be necessary to reach its S$200bn target by 2028. Gross divestments fell from S$5.5bn in FY24 to S$3.1bn in FY25, due to a larger proportion of remaining assets being in China. About S$1bn was divested from China at a 10–20% discount to book value, leaving c.S$3bn of Chinese assets still on the books.

- Maintain BUY with a higher SOTP-TP of S$3.69 (prev. S$3.65) as we roll forward our forecasts. We lower FY26e PATMI by 12% on weaker operating performance in China and narrower margins under the FRB. Balance sheet divestments are expected to accelerate in FY26e, with the potential listing of a second C-REIT. We favour CLI for its robust, growing recurring fee income and asset-light strategy, which supports resilience amid macro uncertainty. The board has proposed a final dividend of 12 cents, implying a yield of 3.8%.

PRIME US REIT – Higher payout ratio backed by cash flow visibility

Recommendation: BUY; TP S$0.32; Last close: S$0.2150; Analyst Darren Chan

- 2H25/FY25 DPU of 0.49/0.61 US cents was in line, forming 80%/98% of our FY25e forecast, supported by a higher payout ratio (2024–1H25: 10%; Oct 2025: 50%; Dec 2025: 65%). FY25 revenue and NPI declined 5.4% and 8.8% YoY, respectively, due to the July 2024 divestment of One Town Centre and lease expiries during the year.

- 680k sqft (16% of NLA) of leases were signed in FY25 at a +5.6% rental reversion (FY24: 592k sqft; +1.8%), reflecting improved leasing momentum. Portfolio occupancy increased from 80.7% to 82.7% QoQ, and we expect it to reach at least 85% by end-2026. Portfolio valuations rose 3.5% YoY to US$1.4bn, indicating a turnaround in capital values.

- Maintain BUY with a higher DDM-derived TP of US$0.32 (prev. US$0.30) as we roll forward our forecasts. The payout ratio has been raised to at least 65% of distributable income, supported by improving committed occupancy and strong cash flow visibility, as new leases signed in FY24/25 (10.6% of portfolio occupancy) are staggered to commence cash contributions from 2026 onwards. Assuming a 65% payout ratio in FY26e, the current share price implies an FY26e DPU yield of 5.9%. Prime trades at a steep discount at 0.42x P/NAV, offering an attractive entry point with dividend growth as the portfolio stabilises.

SG Bonds – Week 08 : SGS yields ease across the curve

Recommendation: REDUCE; TP S$; Last close: S$; Analyst Phillip Research Team

- UST yields declined across the curve over the week, with the 2Y down 9 bps to 3.41%, the 10Y lower by 16 bps to 4.05%, and the 30Y falling 16 bps to 4.70%.

- SGS yields drifted lower in tandem, with the 2Y down 2bps WoW and the 5Y and 10Y declining by 5bps each.

- Looking ahead, markets are pricing only around a 10% probability of a 25bps cut in March, and 55% probability of a rate cut by June. Domestically, SGS yields are expected to remain broadly range-bound at current levels. Recent MAS bill auctions reflect steady liquidity and consistent investor demand, suggesting orderly funding markets with no signs of tightening pressure.

Singapore Telecommunications Ltd – Earnings momentum from associate spreads

Recommendation: ACCUMULATE; TP S$5.35; Last close: S$4.9100; Analyst Paul Chew

- 3Q26 results were within expectations. 9MFY26 Revenue and EBITDA were 73%/74% of our FY26e forecast. PATMI exceeded estimates at 81% of FY26e due to stronger than-expected performance from associate Advanced Info. Weaker India and Indonesia currencies shaved 4.6% points of the underlying net profit’s 14.2% YoY growth in 3Q26 to S$744mn.

- Singapore mobile is the weakest segment with revenue declining 10.8% YoY to S$289mn. Competition, especially in eSIM prices and roaming, continues drag revenue and earnings. Associates’ earnings rose 23% YoY to S$529mn. Earnings grew strongly in Advanced Info (+47.8%) and Airtel (+27.3%).

- Our ACCUMULATE recommendation and FY26e forecasts are maintained. The target price of S$5.35 is unchanged. Earnings growth is supported by the mobile price recovery underway in regional associates. In the medium term, the growth driver will transition to data centres following the acquisition of STT GDC.

StarHub Limited – Parents hong bao helps DARE++ déjà vu

Recommendation: NEUTRAL; TP S$1.01; Last close: S$1.1300; Analyst Paul Chew

- Results were within expectations. FY25 revenue and EBITDA were 102% and 97%, respectively, of our forecast. Adjusted PATMI declined 29% YoY to S$100.5mn in FY25. StarHub is guiding a 15-20% YoY decline in FY26 EBITDA. Despite weaker earnings, the company is maintaining at least 6 cents dividend for FY26 (>100% payout).

- Mobile revenue declined 10% YoY in 4Q25 to S$129mn. The negative operating leverage will pressure margins in FY26. Despite sluggish revenue, there is a lack of cost control, and CAPEX-to-sales is expected to at least double in FY26. Dare+ (or maybe minus) transformation started in 2022 to rein in costs and improve technology. The utopia of $280mn cumulative cost savings was not apparent. Fixed costs are higher since 2022. The company is now positioning a new Dare++ with S$70mn identified cost savings and higher CAPEX.

- We lower FY26e EBITDA forecast by 8% to S$377mn. There is a downside to our forecast as mobile competition remains intense. We expected the share price to be supported by StarHub’s use of its balance sheet to maintain dividends. Our NEUTRAL recommendation is maintained with a lower target price of $1.01 (prev. S$1.05). A potential special dividend or deleveraging event is expected from disposing of ~17% of Ensign’s assigned rights under a put/call option with its parent. After seven years, Ensign’s core operating profit is est.S$800k.

Thomson Medical Group Ltd – Revenue intensity and an ecosystem being built

Recommendation: ACCUMULATE; TP S$0.07; Last close: S$0.0590; Analyst Paul Chew

- Results were below expectations. 1H26 revenue met expectations at 49% of our forecast. However, margins were worse than expected with EBITDA at 38% of our FY26e forecast. Net loss narrowed by 21% to S$10.2mn due to lower interest expenses.

- Singapore EBITDA declined 15% YoY to S$19mn. Margins were much weaker than modelled due to higher staff and depreciation

- We lowered our FY26e EBITDA by 17% to S$84mn. A net loss of S$18.9mn is expected in FY26e, as we raised our depreciation estimates. The SOTP target price is lowered to S$0.071 (prev. S$0.074) as we lower earnings. Our recommendation is downgraded from BUY to ACCUMULATE. Development of the Johor land bank is still pending the review of multiple proposals. The turnaround in Malaysia and Singapore is underway, with case complexity and revenue intensity climbing. However, the turnaround was impacted by additional upfront costs and investments.

Airbnb Inc – Higher bookings from new initiatives in US

Recommendation: REDUCE; TP US$; Last close: US$; Analyst Alif Fahmi

- FY25 revenue met expectations at 102% of forecast, while PATMI came in slightly below at 96%. 4Q25 revenue grew 12% YoY to US$2.8bn, led by a 10% YoY surge in booking volumes. PATMI declined 26% YoY due to higher investment in new growth and policy initiatives.

- For 1Q26e, Airbnb expects revenue to grow 14–16% YoY to US$2.59–2.63bn, supported by modest ADR growth, high single-digit booking volume gains, and FX tailwinds. FY26e higher booking volume may be driven by large events i.e. Winter Olympics this quarter and 2026 FIFA World Cup across 16 North American cities from June to July.

- We upgrade to ACCUMULATE from NEUTRAL recommendation due to recent share price performance with a higher DCF target price to US$138 (prev. US$127). We rolled our valuation forward to FY26e while keeping assumptions unchanged. WACC and terminal growth are maintained at 7% and 3.5%.

AppLovin Corp. – Ad momentum continues amid market volatility

Recommendation: BUY; TP US$600.00; Last close: US$; Analyst Serena Lim Yi Qi

- 4Q25 revenue below our expectations but PATMI surpassed forecast, with revenue up 66% YoY to US$1.66bn and PATMI spiking 84% YoY to US$1.1bn, driven by model advancements to the core mobile gaming business and expansion of the e-commerce vertical. FY25 revenue/PATMI were at 94%/108% of our FY25 forecasts.

- Ad momentum remained strong, as AXON continued to enhance monetisation efficiency, enabling a 30-day advertiser payback while driving annual ad spend on the platform to over US$11bn.

- We upgrade APP to BUY from ACCUMULATE due to recent share price movement while lowering our target price to US$600. We roll our estimates into FY26e, we lower our revenue forecast by 15% as revenue from e-commerce is expected to take time to materialise, given that the segment is still in an early stage and focusing on scaling. However, we increased the PATMI forecast by 3% on improved cost optimisation. Our terminal growth rate remains unchanged, but we raised the WACC to 6.5% from 6.0% to reflect a more cautious market environment. We continue to expect growth to be supported by the expansion of the e-commerce vertical, the self-service programme, and strong performance in the gaming segment.

Magnificent 7 Monthly: Jan 26 – Cloud & Ads Drive Resilient 4Q25 Earnings

Analyst: Phillip Research Team

- Mag-7 stocks rose by 0.2% in Jan26 (Dec25: 0.2%), slightly underperforming the S&P500 (1.4%) but outperforming the NASDAQ (flat). Investors rotated funds out of mega-cap technology and into small-caps, value, and cyclical sectors, driven by profit-taking and concerns about high valuations in technology.

- Mag-7 (ex-NVDA) companies broadly beat CY4Q25 expectations, delivering their highest revenue growth in four years (+15% YoY) and accelerating earnings growth (+23% YoY) driven by robust cloud momentum, strong ad efficiency, and resilient hardware demand. Jan26 saw mixed results as TSLA (+10.9%) gained after 4Q25 earnings beat estimates and META (+10.6%) rose from AI monetisation. AI infrastructure stocks GOOG (+7.3%), MSFT (-9.1%), and AMZN (+5.7%) showed mixed results as investors prioritized AI ROI, rewarding AMZN and GOOG for accelerating cloud fundamentals while punishing MSFT for slowing Azure growth and delayed Copilot monetization.

- We maintain OVERWEIGHT on the Mag-7. Mag-7’s performance in Jan25 was supported by resilient institutional flows into AI infrastructure plays ahead of the 4Q24 reporting season, as investors bet on sustained hyperscaler Capex growth to offset broader concerns regarding valuations and the Federal Reserve’s rate-cut timeline. Except for TSLA, we believe the Mag-7’s earnings growth will continue to outperform both the S&P 500 and Nasdaq 100. Tailwinds include greater demand for AI from sovereign nations, the US government’s AI Action Plan unveiled in Jul25, and more rate cuts expected in 2026.

Palantir Technologies Inc – New high of Commercial growth

Recommendation: BUY; TP US$190.00; Last close: US$; Analyst Alif Fahmi

- FY25 group revenue and PATMI came in above our expectations at 106%/121% of our forecasts, respectively, driven by stronger-than-expected US commercial momentum and continued strength in US government contract execution and new awards.

- For 1Q26e, Palantir Technologies expects group revenue to grow 74% YoY to US$1.53bn, supported by expanding deal sizes and accelerating customer conversions from AIP bootcamps, especially from the US Commercial. Adj. operating income is projected to rise 123% YoY to US$872mn, driven by operating leverage.

- We maintain a BUY recommendation with a lower DCF-based target price of US$190 (prev. US$208). We rolled over for FY26e and lowered our terminal growth to 7.5% from 8%, reflecting normalized long-term revenue growth and rising competitive pressure from analytic AI providers. We remain positive on Palantir as its Ontology moat and AIP tools drive faster enterprise AI adoption beyond defence to other industries (Commercial revenue: +73% YoY in FY26e).

Spotify Technology S.A.- Record MAU addition

Recommendation: BUY; TP US$650.00; Last close: US$; Analyst Helena Wang

- 4Q25 revenue grew 7% and was within expectations. 4Q25 PATMI exceeded our estimates and jumped 220% YoY, driven by favorable content costs and a €67mn benefit from social charges. FY25 revenue/PATMI were at 99%/130% of our FY25 forecasts.

- User metrics ramped up to 751mn MAUs (+11% YoY), the highest quarter for MAU net additions. Premium subscribers grew in double digits to 290mn (+10% YoY).

- We upgrade our rating from ACCUMULATE to BUY rating due to recent price performance while maintaining a DCF target price of US$650 as we roll over our valuations to FY26e. Our FY26e forecast, terminal growth, and WACC assumptions remain unchanged. SPOT has demonstrated strong pricing power and monetization. AI-driven personalization should further deepen user attachment.

Market Journal articles powered by PhillipGPT

Magnificent 7 Stocks Remain Resilient Amid AI Financing Concerns

Netflix Upgraded to Accumulate on Content Strategy and Ad Growth

Palantir Technologies: Strong Growth Prospects Drive BUY Recommendation

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Stoneweg Europe Stapled Trust (SERT) [NEW]

Date & Time: 27 February 26 | 12PM-1PM

Register: poems-20260227-138685

Corporate Insights by OUE REIT

Date & Time: 5 March 26 | 12PM-1PM

Register: poems-20260212-138119

Corporate Insights by Lendlease REIT [NEW]

Date & Time: 10 March 26 | 12:30PM-1:30PM

Register: poems-20260310-138683

POEMS Podcast:

Research Videos

Weekly Market Outlook: AMD, DIS, GOOG, SGX, OUE REIT, Keppel, First REIT, CICT, SG Weekly & More!

Date: 9 Feb 2026Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials