DAILY MORNING NOTE | 17 November 2025

Recent Podcasts:

Grab Holdings – Product-led strategy gaining momentum

Apple Inc.- Strong outlook, yet no real game changer

Amazon.com Inc. – AWS growth accelerating

Week 47 equity strategy: The record US government shutdown ended on Wednesday, but concerns remain. While the resumption of funding restores operations for most federal agencies, some gaps in official economic data are likely to persist due to delayed or cancelled reports. We view these gaps as adding uncertainty to an outlook already pressured by persistent inflation. The labour market remains generally resilient, with low unemployment and steady wage growth, though the shutdown and sector-specific slowdowns have created temporary soft spots. Market-implied odds of a Fed rate cut at the 10 December 2025 meeting have fallen sharply to 44%, down from 88% a month ago, reflecting reduced expectations for near-term policy easing. Nevertheless, we see interest rates remaining on a downtrend, with the market pricing in three cuts through the end of 2026, despite the Fed’s recent hawkish shift.

The key beneficiary of the downtrend in interest rates is S-REITs, which gain from lower financing costs and cap rate compression, supporting higher property valuations. Most S-REITs have released 3Q25 updates, with many showing year-on-year declines in interest expenses that have supported DPU growth. We see the continued rate downtrend as a tailwind for DPU growth in 2026 and believe there is still room for share price recovery, despite the S-REITs index posting an 11% YTD gain.

All eyes will be on Nvidia when it reports quarterly results on Wednesday. Key things to look for are potential early signs of moderation in the AI boom, such as slower AI-related revenue growth or margin pressure, and whether the company’s CAPEX to maintain competitiveness is supported by financial performance.

Darren Chan

Research Manager

darrenchanrx@phillip.com.sg

Singapore stocks ended lower on Friday (Nov 14), tracking regional benchmarks. Local benchmark lost 0.7 per cent or 29.84 points to finish at 4,546.07. Across the broader market, gainers trailed losers 172 to 440, after 1.5 bn securities worth S$1.8 bn changed hands. The local banks all ended lower. DBS lost 0.4 per cent or S$0.22 to finish at S$53.99, OCBC fell 0.8 per cent or S$0.14 to finish at S$18.52, and UOB was down 0.3 per cent or S$0.10 to finish at S$34.

US stocks ended the week higher, supported by a Friday rebound in mega-cap technology names and expectations for the resumption of regular economic data releases as the US government reopens. The S&P 500 finished Friday’s session little changed. Energy was the top-performing of 11 market sectors Friday given climbing oil prices. The index’s largest sector by weight, technology, bounced from being one of the worst-performing sectors to a 0.7 per cent gain. The Nasdaq Composite closed up 0.1 per cent, while the Dow Jones Industrial Average declined 0.7 per cent.

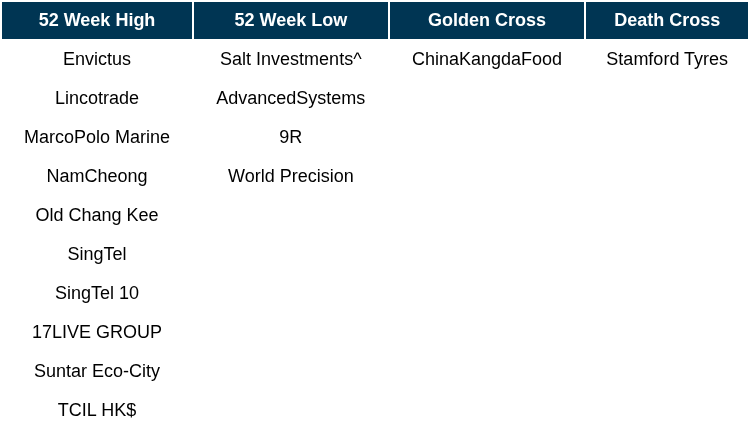

Singapore Technical Highlights

* ^ denotes companies placed on SGX Watch-list

* ^ denotes companies placed on SGX Watch-list

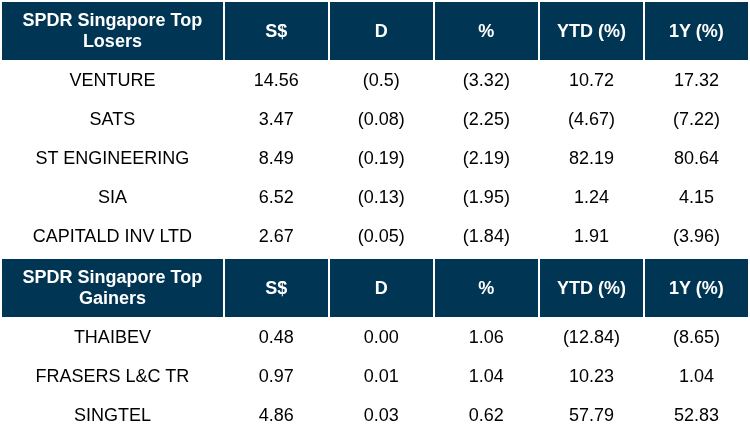

TOP 5 GAINERS & LOSERS

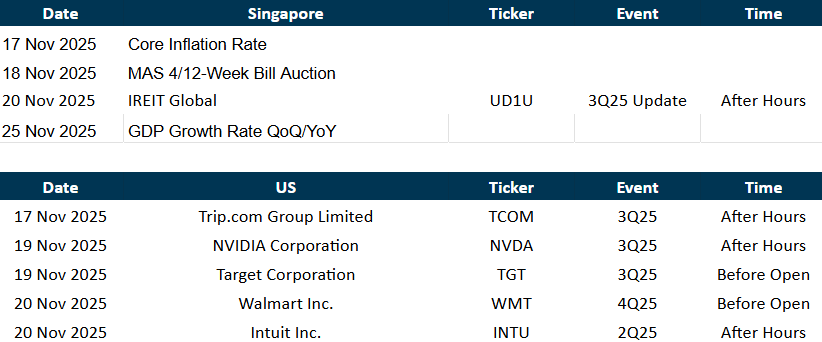

Events Of The Week

SG

Frasers Property posted a net profit of S$100.9mn for the six months ended Sep 30, a 32.2 per cent decline from S$148.9mn for the corresponding period a year earlier.

First Resources posted a 43.5 per cent jump in net profit for the third quarter, it said on Friday. The US$87.5mn figure was markedly higher than the US$61mn in the previous corresponding period, due to a combination of higher average selling prices and sales volumes. Shares of First Resources closed 1.4 per cent or S$0.03 lower at S$2.08 on Thursday.

Stamford Land reported a 4.1 per cent rise in net profit to S$15.8mn for its first half ended Sep 30, from S$15.2mn in the year-ago period. This translates to earnings per share of S$0.0106, a 5 per cent increase from the S$0.0101 in H1 FY2025.

Zixin Group Holdings has reported earnings of RMB16.06mn for its 1HFY2026, double that of the year earlier period ended Sept. Revenue jumped by 40.8 per cent YoY to RMB220.6mn.

The Hour Glass reported a 23.2 per cent rise in net profit to S$75.7mn for the six months ended Sep 30, 2025, from S$61.4mn in the year-ago period.

Sanli Environmental has reported earnings of $6.4mn for 1HFY2026 ended Sept 30, up 32.1per cent YoY. Revenue for the period however came in 3.3 per cent YoY lower at $72.1mn. The group says that the decline in revenue is due to the project completion of Pulau Tekong and the Johor River Waterworks project at Kota Tinggi, resulting in lower revenue recognition compared to the previous period when construction activities were higher.

Metech International Limited reported earnings results for the third quarter and nine months ended September 30, 2025. For the third quarter, the company reported net loss was S$ 0.291mn compared to S$ 0.377mn a year ago.

US

President Donald Trump issued an order on Friday reducing tariffs on beef, tomatoes, coffee and bananas, a move aimed at lowering costs on groceries as the administration faces pressure from voters to cut prices on everyday goods.

Alphabet Inc.’s Google plans to invest $40 bn in three new Texas data centers, ramping up its footprint as competitors such as OpenAI and Anthropic PBC map out their own multibillion-dollar bets in the state.

Google has offered to tweak its ad tech products to settle a European Union order after a near-€3 bn ($3.4 bn ) antitrust penalty, stopping short of a partial breakup watchdogs favor.

Applied Materials Inc. suffered a sales decline last quarter and predicted another drop in the current period, though the chip-equipment maker sees demand improving in the second half of 2026.

Walmart Inc. Chief Executive Officer Doug McMillon, who over a decade ushered the big-box behemoth into the Internet age, will retire in February. He’ll be replaced by US head John Furner — long viewed as the heir apparent.

Merck & Co. agreed to acquire Cidara Therapeutics Inc., a biotech company developing a flu treatment, as part of its ongoing efforts to make up for the upcoming patent loss of its blockbuster cancer drug Keytruda.

Bristol Myers Squibb Co. fell after one of its most important experimental medicines appeared unlikely to benefit patients who had suffered a heart complication, another setback for the drugmaker’s product pipeline.

Boeing Co. stands to win most of a major order from Flydubai for single-aisle aircraft, though Airbus SE still has a long-shot chance to pry some business from an airline that’s never ordered from the European plane maker.

American Tower Corp. and European buyout firm EQT AB are among parties weighing bids for French tower company TDF Infrastructure, people with knowledge of the matter said.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, The Edge Singapore, PSR

RESEARCH REPORTS

Centurion Corporation Limited – Portfolio expansion drives longer-term growth

Recommendation: BUY; TP S$1.81; Last close: S$1.4000; Analyst Yik Ban Chong (Ben)

- Centurion Corporation Limited (CCL) released 3Q25 update with limited financials. 3Q25 revenue is within our expectations, and 9M25 revenue is 74% of our FY25e forecast. Singapore purpose-built worker accommodation (PBWA) remains the main growth driver as its 3Q25 revenue increased 10% YoY to S$49mn, driven by positive rental revisions that we estimate ~5% YoY, which we believe will moderate to ~2% in 2026e.

- CCL announced several expansion pipelines over the next few years. Notably, it entered a fee-based management services contract to manage a 548-bed dormitory for another company on Jurong Island, starting from Nov 2025. We believe it is still immaterial but given Centurion’s track record in managing PBWAs, more of such contracts are likely to be won. The acquisition of Harum Megah in Sep 2025 also added 7.2k beds to CCL’s Malaysia PBWA (+25% capacity). CCL signed a letter of intent with Malaysian authorities in May 2025 to double its bed capacity in Johor in the next five years.

- We lower our TP to S$1.81 (prev. S$2.01), before dividend-in-specie distribution, and upgrade our recommendation to BUY (prev. ACCUMULATE) due to recent share price movements. We lower our TP as we lower our SOTP valuations for most of the segments to 15x P/E (prev. 17x), an 8% discount to peers’ average, to reflect ongoing regulatory headwinds in Malaysia and Australia. Our FY26e revenue/PATMI is lowered by 3%/16% as rental revisions in Singapore PBWAs are expected to moderate in 2026. Our FY25e forecast is unchanged but now reflects the consolidated revenue/PATMI for CCL and Centurion Accommodation REIT (CENT REIT). CCL currently trades at a 4% discount to its NAV per share of S$1.44. We believe CCL will own ~37.5% stake in CENT REIT after distributing dividend-in-specie following the CCL 2026 AGM, which we estimate will yield shareholders ~7.5%.

ComfortDelGro Corp Ltd – Macro and taxi headwinds

Recommendation: ACCUMULATE; TP S$1.62; Last close: S$1.4700; Analyst Paul Chew

- 9M25 revenue was within expectations, but net profit was below. Revenue/PATMI were 77%/68% of our FY25e forecast. Underlying net profit rose 2.5% YoY to S$57.2mn. Most divisions were performing weaker than expected due to soft macro conditions in the UK, driver shortages in Australia, and a sharper contraction in the Singapore taxi fleet.

- UK continues to deliver the growth with operating profit in 3Q25 rising 48% to S$32.7mn (or up 18% excluding acquisitions)—repricing of London bus routes to higher margins supported growth. CMAC’s contribution was weaker due to fewer travel disruptions.

- We reduce our FY25e forecast by 8% to S$213.7mn as we lower operating margins and raise interest expenses. Our DCF target price is lowered to S$1.62 (prev. S$1.68) and ACCUMULATE recommendation is maintained. London bus repricing, resolution of Australian driver shortages, and new Manchester bus and Stockholm rail contracts will drive earnings growth for Comfort. Growth will be offset by a decline in taxi and bus profitability in Singapore.

SG Bonds – Week 47: SGS Curve Remains Stable

Recommendation: REDUCE; TP S$; Last close: S$; Analyst Phillip Research Team

- UST yields fluctuated within a tight range, with the 10Y around 4.10% and the 30Y near 4.70%, broadly unchanged from last week.

- SGS yields were broadly stable over the week, with the 10Y closing at 1.84% (+4 bp WoW) and the 30-year at 1.98% (+9 bps WoW).

- Globally, the focus will be on US data releases and the FOMC Minutes, which may either validate or challenge the recent pushback from Fed officials against a December cut.

Singapore Banking Monthly – Dividends and provisions are the differentiator

Analyst: Glenn Thum

- October’s 3M-SORA was down 11bps MoM to 1.39%, the lowest since August 2022 and fell by 206bps YoY. Singapore loan growth has continued to climb (Sep25: +6.8%). Loans growth is broad based from tech and data centres, real estate, energy, housing and wealth management. Banks are still guiding low to mid-single digit. CASA ratio to total deposits rose (Sep25: 19.7%), 17% YoY, a tailwind for banks, lowering funding costs.

- 3Q25 bank earnings were within expectations except for UOB. Earnings dipped 31% YoY, from lower NII (-6%) as NIMs fell by 24bps YoY. Fee income growth (+18%) partially offset the lower NII. UOB’s earnings fell 72% YoY from a surge in allowances (+348%). The banks are guiding for NIM compression to ease in 2H25 as deposit rate cuts begin to flow through, and we expect FY25e PATMI to decline YoY, as fee income growth will not offset the NII decline. All three banks have committed to their previously announced capital return plans.

- Maintain NEUTRAL. With the continued decline in interest rates in both Singapore and HK, banks’ NIMs have also decreased, affecting NII and earnings. Deposit rate cuts would benefit funding costs in 2H25 and help ease NIM compression, but we believe earnings will decline in FY25e due to lower NII. The banks’ dividend yield of ~6.1% remains

Singapore Telecommunications Ltd – More divisions start to shine

Recommendation: ACCUMULATE; TP S$5.35; Last close: S$4.8300; Analyst Paul Chew

- 1H26 results were within expectations. Revenue/EBITDA/underlying PATMI were 48%/50%/52% of our FY26e forecast. Underlying net profit rose 14% YoY to S$1.35bn, supported by 12% growth in regional associates and 23% jump in subsidiaries. Interim dividend rose 17% YoY to 8.2 cents.

- Bharti India led the earnings growth with an 81% YoY jump in earnings to S$359mn in 1H26. Other divisions enjoying a pick-up in earnings growth were Thailand (+42% YoY) and NCS (+41% YoY). The weakest segments were Singapore (+0.3%), Indonesia (-17%), and the Philippines (-13%).

- Our ACCUMULATE recommendation and FY26e forecasts are maintained. Our target price is raised to S$5.35 (prev. S$4.86) from higher mark-to-market valuations of associates. The growth profile of the Singtel group has expanded from Bharti to include Thailand, and NCS. Thailand is undergoing mobile price repair (+5%), and NCS orders are picking up momentum (+20%). We expect more monetisation to be underway from the disposal of stakes in Gulf Development (~S$2bn) and Bharti Airtel (~S$4bn). The S$2bn value realisation share buyback has recently started. We expect the next growth driver will be new data centres especially GPU-as-a-Service.

StarHub Limited – Still munching popcorn

Recommendation: NEUTRAL; TP S$1.05; Last close: S$1.1600; Analyst Paul Chew

- Results were below expectations. 9M25 revenue and EBITDA were 72% and 71%, respectively, of our FY25e forecast. Earnings were propped up by S$6mn other income grant. 3Q25 PATMI was down 30% YoY to S$26.2mn following the 9% fall in EBITDA and higher depreciation.

- Mobile competition remains intense, especially at the low-end price plans and increased bundling of roaming packages. We think competition has intensified as unlimited mobile data and voice plans have been launched, targeting the premium user. Competition is also spreading to broadband, with 3Q25 revenue declining 4% YoY.

- We lower FY25e EBITDA forecast by 4% to S$418mn. Our NEUTRAL recommendation is maintained with a lower target price of $1.05 (prev. S$1.08). We assume mobile price competition in Singapore will not abate until the end of 2026. We believe StarHub will attempt to narrow its revenue market share with Simba Telecom as it turns 2nd largest operator and focused on integrating networks and synergies. A potential special dividend opportunity for StarHub will be a 20% (currently 56%) sale of Ensign under a call option.

Valuetronics Holdings Ltd- Operating earnings growing stronger

Recommendation: BUY; TP S$1.96; Last close: S$0.8800; Analyst Paul Chew

- 1H26 results were within expectations. Revenue and PATMI were 46%/53% respectively of our FY26e forecasts. 1H26 PATMI grew 2.7% YoY to HKD93mn. Around 10% points of earnings growth was held down by lower interest income. Operating profit rose around 17% YoY to HKD71mn. Dividends were unchanged at 8 HK cents in 1H26 (4 cents interim, 4 cents special).

- 1H26 earnings grew from the 2%-point expansion in gross margins, led by growth in the industrial and commercial division. New customers in network infrastructure and PC cooling solutions have led the growth. Network infrastructure products are now the largest category. Revenue declined due to the exit of legacy consumer products.

- We raised our FY26e earnings by 3% to HK$181.9mn from higher gross margins, but lowered revenue and interest income. The target price is increased to S$0.96 (prev. S$0.785), or 13x PE FY26e, which remains a discount to industry valuations. Our ACCUMULATE recommendation is maintained. The dividend yield of 5.4% (including a special for the 3rd consecutive year) is backed by net cash of HK$1.1bn (S$185mn), equivalent to 53% of market cap. We expect more new customers in FY27e. Despite tariffs, customer enquiries remain robust, with US customers still looking for an Asian supply chain. We expected customer adoption of TrioAI to be longer than expected.

Venture Corporation Ltd – More time needed to recover

Recommendation: NEUTRAL; TP S$13.00; Last close: S$15.0600; Analyst Paul Chew

- 3Q25 results were within expectations. Both 9M25 revenue and PAT were 76% of our FY25e forecast. Net profit in 3Q25 fell 8.3% YoY to S$55mn. The shorter replacement cycle of the key lifestyle consumer product was a significant drag on revenue.

- Venture’s guidance points to new product wins in network connectivity products for hyperscaler data centres and new product launches in lifestyle consumer. Both categories will only contribute meaningfully likely in 2H26. Tariffs have also made Singapore a more attractive manufacturing destination for the US market.

- We nudge our FY25e PATMI down by 1% on account of lower interest rates and foreign exchange. Our NEUTRAL recommendation is maintained. The target price is raised to S$13.00 (prev. S$11.80) as we roll over our valuations to FY26e as the recovery year. The PE ratio is also increased to 15x, in line with its 5-year average. The dividend yield of 5.5% and the strong net cash balance sheet of S$1.2bn have been the attraction. Operationally, we expect challenging conditions until 2H26 when new products materially ramp up. The stock is trading at a steep valuation of 18x PE FY25e.

Sea Ltd.- All rounded growth continues

Recommendation: BUY; TP US$170.00; Last close: US$; Analyst Helena Wang

- 3Q25 revenue was in line with expectations, while PATMI underperformed mainly because Shopee’s higher logistics, fulfilment, and user-engagement investments. 9M25 revenue/PATMI was at 75%/60% of our FY25 estimates.

- Revenue rose 38% YoY, driven by Shopee’s strong momentum with higher commission and ad take rates, Monee’s rapid loan-book expansion (+70% YoY), and Garena’s best performance since 2021 on the back of successful IP collaborations.

- We raised our FY25/26 revenue by 3%/4% to reflect improved growth in all three segments. We increase FY25/26 selling & marketing expense by 5% to account for the elevated investment. Our DCF target price remains unchanged at US$170, with a terminal growth rate of 4.5% and a WACC of 7.6%. We upgrade our recommendation from NEUTRAL to BUY due to recent share price movement.

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Corporate Insights by Wee Hur Holdings [NEW]

Date & Time: 10 December 25 | 12PM-1PM

Register: poems-20251210-133186

Corporate Insights by Marco Polo Marine [NEW]

Date & Time: 11 December 25 | 12PM-1PM

Register: poems-20251211-133188

POEMS Podcast:

Research Videos

Weekly Market Outlook: MSFT, ABNB, AMD, AAPL, UOB, DBS, OCBC, CLI, SG Weekly & More!

Date: 10 Nov 2025Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials