DAILY MORNING NOTE | 18 May 2023

SINGAPORE shares had nowhere to go but down on Wednesday (May 17), following Wall Street’s overnight losses and the release of weak export data, which raised the risk of a technical recession for Singapore’s economy in the second quarter of 2023.Singapore shares tumbled 40.2 points or 1.3 per cent to 3,173.84, after US stocks retreated on the back of mixed economic data, weak corporate results and the ongoing debt-ceiling negotiations in Washington. On the local bourse, some 1.3 billion units worth S$1.3 billion were traded. Losers outnumbered gainers, with 341 counters down and 227 up. Key gauges across the region fared mixed: Japan, South Korea, Malaysia and Taiwan posted gains, while falls were recorded in Hong Kong, China and Australia.

WALL Street stocks finished solidly higher Wednesday (May 17), shrugging off a mixed session in overseas markets on hopes for an agreement to avert a US debt default. Although there is still no compromise to lift the nation’s debt ceiling, President Joe Biden said he was “confident” the country would not default, while Republican House Speaker Kevin McCarthy said he was “optimistic about our ability to work together”. Equities halted the recent trading lull, with gains in the S&P 500 topping 1.2% and the Nasdaq 100 hitting the highest since August. Treasuries dropped, with yields on 10-year notes approaching 3.6%.

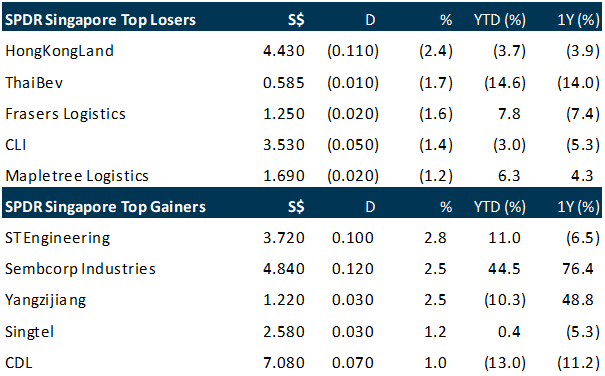

Top gainers & losers

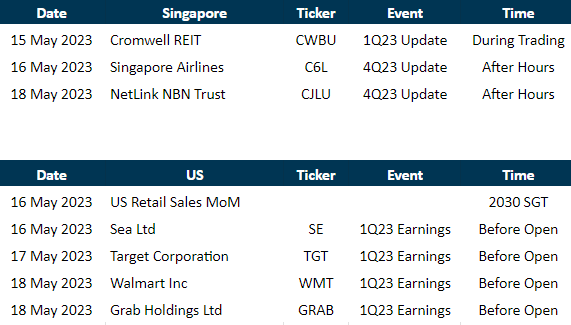

EVENTS THIS WEEK

SG

SINGAPORE’S recovery momentum has been moderating amid the global economic slowdown, but the city-state has “ample fiscal space to deploy if downside risks materialise”, a team from the International Monetary Fund (IMF) has said. IMF economist Lamin Leigh, who led the team in discussions in Singapore from May 8 to May 17, said: “The tighter fiscal stance in the FY2023 budget, combined with targeted support to the most vulnerable, will appropriately help moderate price pressures. Gross domestic product (GDP) is projected to grow by 1 per cent in 2023, reflecting the weakening external demand from the slowdown in growth of the country’s major trading partners as well as slowing domestic demand following the post-reopening recovery, he said.

SINGAPORE Airlines will be rewarding eligible employees with a profit-sharing bonus of 6.65 months following the group’s record earnings, and a maximum total of 1.5 months of ex-gratia bonus in recognition of their hard work and sacrifices during the pandemic. SIA will award an additional 0.5 month of ex-gratia bonus for each of the last three financial years, or a maximum total of 1.5 months, to eligible employees. The group now has some 24,000 employees on its payroll, up 12.3 per cent year on year.

HATTEN Land on Wednesday (May 17) addressed a claim that its subsidiary was under probe by the Malaysian authorities over its Harbour City development in the Malaysian state of Melaka. In February this year, Hatten Land announced that it would terminate an existing agreement it had with Tayrona Capital Group over the proposed divestment of GMSB. The developer said Tayrona Capital Group did not comply with its obligations, including paying a consideration to GMSB.

Scoot announced that none of the Airbus A320neo planes in the Singapore Airlines group with Pratt & Whitney engines are currently grounded over a lack of spares, said on Wednesday (May 17).The engines have been under scrutiny since Go Airlines (India) filed for bankruptcy protection this month, blaming “faulty” Pratt engines for the grounding of about half of its 54 Airbus A320neos.

ST Engineering on Wednesday (May 17) announced that its commercial aerospace business and SF Airlines – a Chinese cargo airline – have incorporated a new joint-venture company in Ezhou, in China’s Hubei province. The company will operate a greenfield airframe facility at the Ezhou Huahu Airport to provide airframe maintenance, repair and overhaul (MRO) services to cargo and passenger airlines operating in Asia, including SF Airlines.

US

GOLD prices held steady in early Asian trade on Wednesday (May 17) after retreating from the key US$2,000-an-ounce mark in the previous session, while investors kept their eyes peeled for an outcome from the US debt-limit negotiations. Traders are currently pricing in an 85 per cent chance of the US central bank holding rates in June, according to the CME FedWatch tool. SPDR Gold Trust GLD, the world’s largest gold-backed exchange-traded fund, said its holdings rose 0.09 per cent to 934.93 tonnes on Tuesday from 934.07 tonnes on Monday. Spot silver was flat at US$23.74 per ounce, while platinum rose 0.4 per cent to US$1,061.43. Palladium fell 0.1 per cent to US$1,499.84.

UBS GROUP expects a financial hit of about US$17 billion from the takeover of Credit Suisse Group, the bank said in a regulatory presentation as it prepares to complete the rescue of its struggling Swiss rival. UBS estimates a negative impact of US$13 billion from fair value adjustments of the combined group’s assets and liabilities. It also sees US$4 billion in potential litigation and regulatory costs stemming from outflows. UBS, however, also estimated it would book a one-off gain stemming from the so-called “negative goodwill” of US$34.8 billion by buying Credit Suisse for a fraction of its book value.

PFIZER sold US$31 billion of debt in the fourth-largest US bond sale ever, according to a person with knowledge of the matter. Pfizer’s mega bond sale comes as the Federal Trade Commission (FTC) sued to block Amgen’s US$27.8 billion deal to buy Horizon Therapeutics on Tuesday, arguing the tie-up would stifle competition for the development of treatments for serious illnesses.

DEUTSCHE Bank is seeking to cut office space by 40 per cent at its key base as a rising number of employees work from home. Germany’s largest lender expects to achieve reductions across Frankfurt and neighbouring Eschborn by the end of 2024, it said in a response to an investor question at its annual general meeting on Wednesday (May 17). Almost two thirds of employees have registered for a hybrid work model introduced three years ago that allows up to three days of home office per week.

Goldman Sachs Group dramatically reduced its exposure to the Adani Group in its ESG portfolios in the weeks following allegations of fraud against the conglomerate by short-seller Hindenburg Research. Goldman funds registered as promoting environmental, social and governance goals under European Union rules sold about 11.7 million shares in Adani companies in February, according to data compiled by Bloomberg. Following the retreat, Goldman Sachs Asset Management’s actively managed ESG fund exposure to Adani was limited to a stake of roughly 400,000 shares in Ambuja Cements, the data show.

SONY Group plans a buyback of up to 2.03 per cent of its shares over the next twelve months, after warning of headwinds ahead from a slump in global consumer spending.It will spend as much as 200 billion yen (S$2 billion) to buy a maximum of 25 million of its shares.

Source: SGX Masnet, Bloomberg, Channel NewsAsia, Reuters, CNBC, WSJ, The Business Times, PSR

RESEARCH REPORTS

BRC Asia – Disappointing 1H23, strong uptick expected in 2H23

Recommendation: BUY (Maintained); Last Done: S$1.64

Target Price: S$1.99; Analyst: Peggy Mak

– 1H23 net profit was below our expectations, at 31% of our FY23e forecasts. Net profit fell 34.1% YoY, due to 1) 15% decline in ASP; and 2) slow construction progress with safety measures implemented at worksites, which caused deliveries to be deferred. Lower order delivery was mitigated by trading volume, which reduced gross margin by 1.3% pt to 7.4%.

– Construction activities have picked up since April. Demand remains strong, underpinned by pent-up demand in residential and infrastructure development. BCA has projected 2023 construction demand at S$27bn-32bn (2022: S$29.8bn) and progress payment to grow by 9-20%. BRC’s orderbook has further grown to S$1.42bn. Rebar prices have stabilized from Feb 2023.

– Maintain BUY with a lower DCF-derived target price of $1.99 (prev. $2.14). We cut our forecasts by 23.2% and 27.7% for FY23e and FY24e to reflect the lower 1H23 earnings. We expect steel prices to stabilize for the rest of the year, though this implies a 20.4% YoY decline in 2H23. Order deliveries should rise as construction activities are ramped up.

Silverlake Axis Ltd – Higher OPEX hurt earnings

Recommendation: Buy (Maintained), Last done: S$0.33, TP: S$0.49, Analyst: Glenn Thum

– 3QFY23 earnings of RM34.2mn were below our estimates. 9MFY23 earnings were at 64% of our FY23e. The 15% YoY dip in earnings came from higher-than-expected OPEX due to the current inflationary environment and a need to increase staff costs.

– Project-related revenue comprising software licensing and software project services fell 27% YoY. Silverlake recently signed their first multi-million 10-year core and channels digital banking MOBIUS deal with a client in Malaysia, total size of more than RM100mn of which RM30-40mn will be booked in the first year.

– We maintain BUY with an unchanged target price of S$0.49. We lower FY23e earnings by 7% as we increase operating expenses estimates for FY23e. Our target price is pegged to 21x P/E FY23e. We expect MOBIUS and the recovery in bank IT spending after two cautious pandemic years to be the key growth drivers for the company.

ComfortDelGro Corp Ltd – Inflationary pressures gradually abating

Recommendation: BUY (Maintained); TP S$1.57, Last close: S$1.16; Analyst Paul Chew

– 1Q23 revenue was within expectations but PATMI disappointed. 1Q23 revenue/PATMI was 22% and 18% of our FY23e forecast.

– The cost recovery from higher indexation of bus fees is underway in UK but the full benefit will be more evident in 2H23. Taxi earnings were hampered by incentives in China to attract taxi drivers, especially in Beijing. Balance sheet continues to strengthen with net cash of S$718mn.

– The recovery in Singapore disappointed. Improvement in rail passenger volumes and prices could not offset the higher electricity and lower bus contracting fee. We are reducing lowered our FY23e PATMI by 8% to S$167.4mn. Recovery in FY23e will stem from increased passenger volumes for both taxis and trains, a reduction in taxi rental rebates in Singapore by 5% points, indexation of UK bus contracts and lower of taxi rebates in China. We maintain BUY with a reduced DCF target price of S$1.57 (prev. S$1.63).

Airbnb Inc – Strong performance overshadowed by soft guidance

Recommendation: BUY (Upgraded); TP: US$143.00

Analyst: Ambrish Shah

– 1Q23 revenue/PATMI was within expectations at 19%/6% of our FY23e forecasts because of seasonality weakness. Revenue growth of 20% YoY was led by a 19% YoY surge in booking volumes. We expect profitability in 2H23e to rebound strongly driven by summer travel demand and higher operating leverage.

– Airbnb expects 2Q23e revenue growth of 12-16% YoY. Booking volumes face pressure from tough comparisons following the Omicron-fueled pent-up demand in 2Q22. Management reiterated its adj. EBITDA margin guidance of about 35% for FY23e.

– We upgrade to BUY from ACCUMULATE recommendation after the recent fall in its stock price. We lower our DCF target price to US$143.00 (prev. US$149.00) with a WACC of 7% and terminal growth of 4%. We lower our FY23e revenue estimates by 2% due to softening travel demand, while increasing our PATMI by 13% to account for higher interest income. We believe Airbnb platform offers better non-urban location listings versus hotels, benefits travelers looking for long-term stays, and is more family and group travel-friendly.

Spotify Technology S.A. – Confidence in user growth

Recommendation : ACCUMULATE (Maintained); TP: US$165.00, Last Close: US$146.32

Analyst: Jonathan Woo

– 1Q23 results were within expectations. 1Q23 revenue at 22% of our FY23e forecasts, with adj. net loss (excl. one-offs) EUR80mn lower than our FY23e forecasts.

– Record 1Q user additions with 26mn, MAU/premium subscribers of 515mn/210mn beat guidance with broad-based outperformance across all regions. 1Q23 operating loss of EUR156mn beat guidance by ~20% on lower marketing spend.

– We maintain ACCUMULATE with a raised DCF target price of US$165.00 (prev. US$128.00) to account for increasing user growth and stronger long-term pricing power. We maintain a WACC of 7.5%, but raise our terminal growth rate to 4% (prev. 3%) due to an acceleration in user additions and higher MAU to Premium conversion rates.

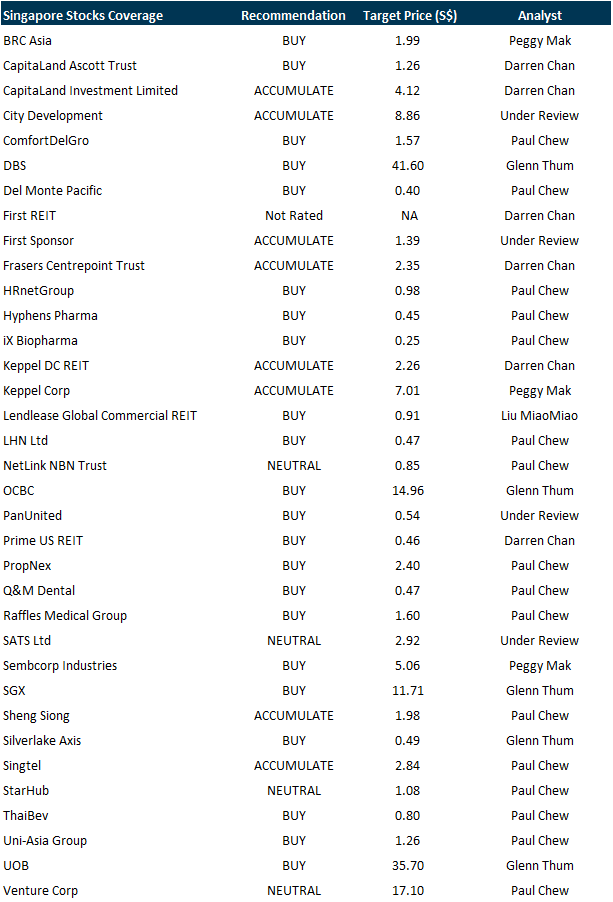

PSR Stocks Coverage

For more information, please visit:

Upcoming Webinars

Guest Presentation by LHN Limited [NEW]

Date: 26 May 2023

Time: 12pm – 1pm

Register: https://bit.ly/44XPNdk

Guest Presentation by Sunview Group Berhad [NEW]

Date: 1 June 2023

Time: 12pm – 1pm

Register: https://bit.ly/3LUwZme

Guest Presentation by United Hampshire US REIT [NEW]

Date: 28 June 2023

Time: 7pm – 8pm

Register: https://bit.ly/3pIRkUl

POEMS Podcast:

Research Videos

Weekly Market Outlook: OCBC, Block Inc., PayPal, Alphabet, META, SG Banking, SG Weekly & More!

Date: 15 May 2023

Click here for more on Market Outlook.

Sign up for our webinars here, and be among the first to receive economy and market updates.

PHILLIP RESEARCH IN 3 MINS

Phillip Research in 3 minutes: #29 Keppel Corporation; Initiation

Click here for more on Phillip in 3 mins.

Join our Singapore Equity Research Community on POEMS Mobile 3 App for the latest research reports, market updates, insights and more

Disclaimer

The information contained in this email and/or its attachment(s) is provided to you for information only and is not intended to or nor will it create/induce the creation of any binding legal relations. The information or opinions provided in this email do not constitute an investment advice, an offer or solicitation to subscribe for, purchase or sell the e investment product(s) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this information. Investments are subject to investment risks including possible loss of the principal amount invested. The value of the product and the income from them may fall as well as rise. You may wish to seek advice from an independent financial adviser before making a commitment to purchase or investing in the investment product(s) mentioned herein. In the event that you choose not to do so, you should consider whether the investment product(s) mentioned herein is suitable for you. PhillipCapital and any of its members will not, in any event, be liable to you for any direct/indirect or any other damages of any kind arising from or in connection with your reliance on any information in and/or materials attached to this email. The information and/or materials provided 揳s is?without warranty of any kind, either express or implied. In particular, no warranty regarding accuracy or fitness for a purpose is given in connection with such information and materials.

Confidentiality Note

This e-mail and its attachment(s) may contain privileged or confidential information, which is intended only for the use of the recipient(s) named above. If you have received this message in error, please notify the sender immediately and delete all copies of it. If you are not the intended recipient, you must not read, use, copy, store, disseminate and/or disclose to any person this email and any of its attachment(s). PhillipCapital and its members will not accept legal responsibility for the contents of this message. Thank you for your cooperation.

Follow our Socials